Liontrust’s multi-asset strategies have led the pack for the past five years.

Liontrust Asset Management beat its multi-asset competitors by having the most balanced and adventurous strategies that consistently outperformed during the past five years, data from FinXL reveals.

Trustnet compared multi-asset funds by measuring their alpha – an indicator of a fund’s performance in excess of its benchmark that is often used by investors as a way to tell whether their funds have been worth their fees.

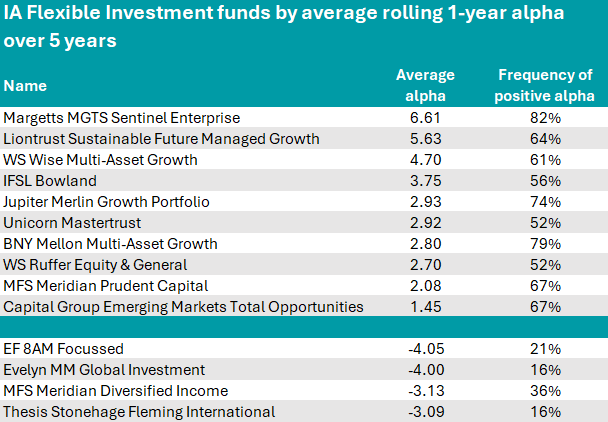

In the study below, we look at the IA Flexible Investment and the IA Mixed Investment 40-85% Shares sectors and highlight the constituents that have the highest 12-month average rolling alpha of the past five years, meaning that they outperformed their benchmarks in most of the 61 year-long periods that begin each month from January 2018 to December 2023.

In the IA Flexible Investment sector, where most funds measure their performance against the peer group average, the top vehicle was Margetts MGTS Sentinel Enterprise. This £105.2m portfolio had an average alpha of 6.61 and is led by FE fundinfo Alpha Manager Gerrit Smit, who is also in charge of the much bigger Stonehage Fleming Global Best Ideas Equity fund.

The Sentinel Enterprise strategy has been a top-decile performer over the past 10 and five years and remained in the second decile over the past three years and 12 months too.

Source: FinXL

A whole point below it, in second position, was the first Liontrust vehicle we encounter, the Sustainable Future Managed Growth fund, whose average alpha was 5.63.

The strategy, alongside the whole Sustainable Future range, is considered by Square Mile analysts “a strong choice” for investors who are looking to grow their capital by investing in companies that are making a positive contribution to the planet and society.

“The managers have demonstrated they are able to deliver robust returns following this tried and tested process but the approach can lead to a return profile that is more volatile than many peers. However, we think over the long term it can deliver superior returns,” they said.

The list also included the Jupiter Merlin Growth Portfolio (2.93) and WS Ruffer Equity & General (2.7).

Jupiter Asset Management featured predominantly amongst the cautious funds that keep delivering the most bang for your buck and its Growth Portfolio’s alpha confirms the group’s strength in managing multi-asset strategies.

The Ruffer fund, managed by FE fundinfo Alpha Manager Alex Grispos, beat its benchmark – the FTSE All Share – by an average of 2.7% in the past five years.

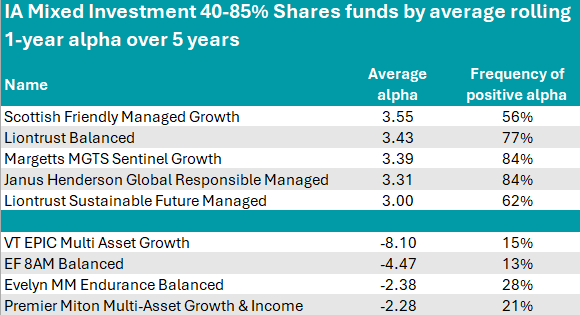

In pole position in the IA Mixed Investment 40-85% Shares sector sits the £163m Scottish Friendly Managed Growth fund, a five FE fundinfo Crown-rated strategy managed by Colin McLean, benchmarked against the FTSE All Share.

With an average alpha of 3.55, it was a top-decile performer in the 196-strong peer group over the past three years and a second-decile performer over five, while dropping to the second-quartile over 10 years and 12 months.

Source: FinXL

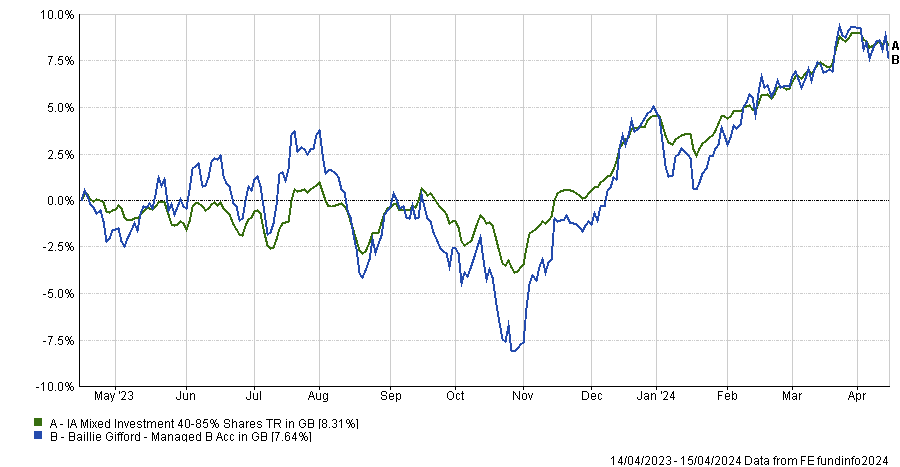

Moving on to funds that use the sector average as their benchmark, in second position was Liontrust Balanced, with an average alpha of 3.43.

The fund and its managers Tom Hosking and Hong Yi Chen joined the Liontrust stable in April 2022 with the acquisition of Majedie Asset Management.

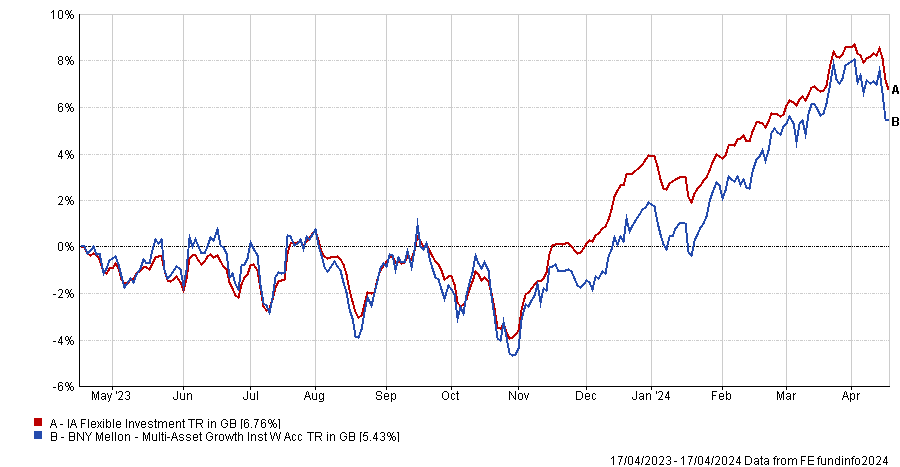

The fund has bested its benchmark in more rolling one-year periods than not, but it hasn’t all been plain sailing. Between the transition to Liontrust and the end of 2023, the fund trailed the sector average but it returned to form this year, as the chart below shows.

Performance of fund against sector since moving to Liontrust

Source: FE Analytics

Another Liontrust fund, Sustainable Future Managed, also had a high average alpha score of 3.

Meanwhile, Janus Henderson Global Responsible Managed had a positive alpha in 51 out of the 61 periods measured and achieved an average alpha of 3.31. This is another strategy that avoids harmful industries and has a focus on sustainability.

It stood out to Square Mile analysts for its style diversification provided by its three sub-portfolios: a UK sleeve with an income focus, which balances out the global, growth-biased sleeve; and a fixed-income sleeve that is usually the smallest component but acts as a volatility dampener through a portfolio of G7 government bonds and global credit.

Finally, at the foot of the table was VT EPIC Multi Asset Growth, which had the worst average alpha of the sector at -8.1.

Sectors previously in this series: UK Equity Income, UK All Companies, Global, Global Equity Income, Sterling bonds, smaller companies, global bonds, cautious funds.

The two longstanding funds will close later this year.

The £20m CT UK Smaller Cap fund and £28m Aviva Investors UK Smaller Companies fund are both to be closed in the coming months. The former will close its doors on 6 June while the latter is to shut on 10 May.

UK small-caps have had a torrid time of late, with investors moving away from riskier assets in favour of defensive holdings such as bonds and cash, which now offer attractive returns thanks to higher interest rates.

This, along with economic uncertainty surrounding inflation and geopolitical tensions around the world, has caused investors to take a more cautious approach.

While some believe better times are ahead, Columbia Threadneedle and Aviva have thrown in the towel on their funds.

CT UK Smaller Cap, managed by Catherine Stanley since 2004 and Patrick Newens since 2019, was originally launched in February 1988 and has been one of the best performers in the IA UK All Companies sector over three years, making an 11.5% loss. Over 10 years the fund has made 78.6%, placing it in the second quartile of the sector.

However, the fund has failed to accumulate significant assets under management (AUM), with its total assets peaking in2021 around £33m.

Conversely, the Aviva Investors UK Smaller Companies fund has struggled over the long term, with a return of 60.5% over 10 years and has fared even worse over three years, down 25.4%.

Trevor Green has managed the fund since 2014 and was joined by co-manager Charlotte Meyrick in 2017. The fund pre-dates both however, having been initially launched in 1998. Assets under management reached £66m in July 2021 but have slipped back to the £28m in the fund at present.

A spokesperson for Aviva Investors said: “To ensure our fund range remains efficient, of high quality and provides the best outcomes for our clients, we regularly assess the value offered by our funds. This assessment process has led us to take the decision that it is in the best interests of investors to close the fund.

“The fund possessed a relatively small AUM and as such we would expect the broader impact of this decision to be very limited. The announcement has already been communicated to clients.”

Investors will have the option to switch into another Aviva Investors fund free of charge or to receive the proceeds of the sale of their investment as cash.

A spokesperson from Columbia Threadneedle Investments said: “We keep our range of funds under regular review and are committed to offering investors the best possible opportunities and value for money.

“Following a recent review, we have decided to close the CT UK Smaller Cap fund. The fund has experienced a fall in assets and became too small to run as efficiently as we would wish. We believe the closure of the fund is in the best interests of investors.”

Please note, a previous version of this article stated the CT UK Smaller Companies fund managed by James Thorne was to close. This was incorrect and the article has been amended accordingly to reflect the closure of the CT UK Smaller Cap fund.

The market is underestimating the tailwinds of US housing companies, according to BNY Mellon’s Paul Flood.

Tech stocks have done particularly well recently but there another industries that have grown exponentially and the market underestimates them.

Within the £2.2bn BNY Mellon Multi-Asset Growth portfolio, US home builders have been among the top performers of the past 12 months, with relative contributions higher than Microsoft’s.

The fund has achieved top-quartile performance over 10, five and three years and is co-managed by FE fundinfo Alpha Manager Bhavin Shah, Simon Nichols and Paul Flood – the same team behind the highly successful and popular £3.4bn Balanced fund.

Below, Flood discusses the underestimated tailwinds for US home builders, the sectors he sees as opportunities and those he avoids, and why he favours UK gilts over US treasuries.

Performance of fund against sector and index over 1yr

Source: FE Analytics

Can you sum up your investment process?

We're investing in companies that have long-term structural thematic support, proven business models and attractive valuations with bias towards growth companies or companies in sectors where we think there's a cyclical opportunity.

It’s a very flexible product as we can invest everywhere and we aim to get the broadest views around the house. We’re willing to take more aggressive stances and to be zero weights in some industries, as we’ve been in the past for bonds, for example.

When did you increase your fixed income allocation?

We've had very little in bonds for a long time, until the past 12 to 18 months, when they have started to become more attractive and got a yield and a return on them. The allocation still remains fairly low, however, at 10%.

Because the growth element of the fund is going to be driven by our equity allocation, we want bonds that work when there's more volatility and down-trending growth in the global economy, which is why the vast majority is in government bonds.

We've got some Australian, New Zealand and US Treasuries as well as UK gilts. We're favouring gilts over US Treasuries, given the risks that we see in the long end of the curve in the US, due to the fiscal expenditure and the continued deficit, which we think is a bit of a risk.

What equity sectors are you more bullish on?

We’re always looking at technology because it has the most growth, and industrials as it benefits from fiscal spending. Within that, we favour industries that are exposed to the long-term dramatic changes that we're seeing across global economies as we look to reduce the impact of global warming – so electrification, renewables, decarbonisation.

And it’s not just wind and solar – we think HVAC [heating, ventilation, and air conditioning] technologies are very interesting, as heating and ventilating our buildings represents 25% of global carbon emissions.

Here, we invest in Trane Technologies, which provides equipment that is 20-40% more efficient than legacy systems, so clients can massively reduce their carbon intensity.

What areas do you not invest in?

We’ve had zero in real estate for a long time, where we have fairly negative views from a thematic standpoint.

More and more trade is done online, which is a headwind to the high street – both on the industrials side of real estate but also offices. Even pre-pandemic, the internet was allowing us to be more flexible and we saw that as a headwind.

What have been the worst calls of the past year?

The area that has struggled the most recently was the electric vehicles supply chain. Battery manufacturer Samsung SDI was the biggest detractor to relative performance at -1%, alongside chemical manufacturer Albemarle.

With those stocks and our position in physical nickel, the EV supply chain cost the fund 2.6% in relative performance versus the IA Flexible sector.

Asian life and health insurers AIA and Prudential also cost the fund 1.5% in relative performance, but we continue to believe they are well placed over the longer term, given the ageing populations.

What has done well instead?

Our top holding is Microsoft, which did extremely well and added 0.55% of relative performance, but it wasn’t our top performer, which was US home builder Toll Brothers. It added 1.1% of relative performance.

So not a growth stock?

Surprisingly, yes. The market massively underestimated the changing business model of house builders in the US. Because they overbuilt in the financial crisis, there's been a huge under-build since then.

Generally speaking, it's not the same industry that caused the last crisis to cause the next, and US housing companies have moved away from having all the land development on their balance sheets. Instead of buying it, they take options on it, which is less balance-sheet intensive.

Interest rates are a massive headwind for moving into existing housing, as people want to avoid re-mortgaging at higher rates, so we’re seeing many more renovations instead. Houses are being built for the post-pandemic workforce that is moving out of California towards Texas, out of cities and into the suburbs.

Another tailwind comes from the fact that the US is the second little piggy, it builds its house out of wood, and so there is a replacement cycle unlike in Europe, where we build our houses out of brick.

What do you do outside of fund management?

Running and cycling help with the stress of the job and give you time to think away from screens.

People who mine the cryptocurrency will receive 3.125 Bitcoins for their effort, down from the 6.24 Bitcoins they currently receive.

Bitcoin, the world’s largest cryptocurrency, could be in line for a sharp rise in price following the latest halving, according to Pieran Maru, investment manager in the Liontrust Global Equities team.

Bitcoin is ‘mined’ by computers, which create new coins. When it first started, each time a successful block of coins was mined in January 2009, the individual responsible for doing so would receive 50 Bitcoins.

However, this has come down significantly thanks to ‘halving’ events, which occur every 210,000 blocks mined. There have been three so far, but the fourth is expected to take place this week.

In the first ‘halving’ event in 2012, the number of Bitcoins given to someone who successfully mined a block dropped from 50 to 25. Once the next halving event occurs in the coming days, people who mine the cryptocurrency will receive 3.125 Bitcoins for their effort, down from the 6.24 Bitcoins they currently receive. This is expected to take the number of new Bitcoins produced per day down from 900 to 450.

“This potentially could lead to an increase in the price of Bitcoin, if the demand remains constant or increases, while the rate of supply slows,” said Maru.

Following the first halving in November 2012, Bitcoin’s price jumped around 9,500% to a peak of $1,160 in one year, while after the 2016 halving the price rose by 3,040% to $19,660 around 18 months later. After the halving in 2020 the price took time to rise but ended up 802% higher to a top of $73,800 almost four years later.

However, not all were convinced. Nigel Green, founder of deVere Group, said: “It is likely to be a major price non-event. Investors, traders and speculators priced in the halving months ago. As a result, a significant portion of the positive economic impact was experienced previously, driving up prices to fresh all-time highs last month.”

Indeed, Bitcoin reached a new all-time high of $75,830 on March 14 2024.

Either way, Maru said it is clear cryptocurrencies are becoming an increasingly significant part of the financial world, despite some likening it to the ‘wild west’, a term given after several scandals.

“From being a niche digital currency to a defined asset class, with approximately one in five Americans owning crypto, the future appears bright. Bitcoin has experienced a surge in retail and institutional activity following the announcement by the US Securities and Exchange Commission (SEC) in January approving the long-awaited Bitcoin ETFs (exchange traded funds). To date, the total fund assets in these ETFs has reached $56.2bn, representing about 4.4% of Bitcoin supply,” said Maru.

Progress is being made on regulatory frameworks for cryptocurrency, he added, including the Markets in Crypto-Assets Regulation (MiCA) in Europe, which came into effect last year.

“Bitcoin, as the pioneer, has inspired the creation of new blockchains that are more scalable and have added utility, such as decentralised apps and smart contracts. Despite this, Bitcoin's dominance continues to hold as the original truly decentralised blockchain,” he said.

Some domestic companies are paying 10% dividends – more than double the amount investors can get from bonds and cash.

Cash has been king for the past 18 months or so as investors have taken advantage of higher interest rates and locked in good returns in cash accounts.

For investors, this has also meant a return to fixed income, which struggled in 2022 but now appears to be on strong footing, as Pictet’s Jon Mawby told Emma Wallis this week.

Yet with interest rates likely to be on their way down this year, investors may start to return to the stock market for their income. While riskier, it presents a good opportunity to gain an income far higher than from cash and bonds.

The 10-year gilt currently offers investors an income of 4.07% per year, while the top easy access savings accounts are higher at 5.2%.

Yet there are some companies far exceeding this. At the top of the tree is cigarette maker British American Tobacco, which currently offers a 9.9% dividend yield, according to data from AJ Bell investment director Russ Mould.

It has dividend cover – how much it receives in earnings versus the amount it pays to shareholders – of 1.4x and has not cut its dividend in more than a decade.

“It can even point to a streak of increases in its annual dividend payment that stretches back to 1998,” Mould noted.

Insurance firm Phoenix Group is another with a 9.9% yield, although dividend cover is lower at 0.3x and it has a habit of lowering its dividend – doing so in both 2016 and 2018.

But there are a plethora of stocks with high income payouts. Asset manager M&G currently yields 9.4%, followed by fellow tobacconist Imperial Brands (8.7%) as well as financial juggernauts Legal and General (8.4%), HSBC (7.6%) and Aviva (7.1%).

However, investors need to keep in mind that investing directly in single stocks is much riskier than diversifying.

Furthermore, companies may be paying sky high yields because their share prices are cheap for a reason. An oft-used rule of thumb states “any dividend yield which exceeds the risk-free rate by a factor of two may turn out to be too good to be true”, Mould said.

“The 10-year gilt yield is a good proxy for the risk-free rate. A dozen years of interest rates at near zero rendered the rule pretty useless but now monetary policy is returning to something akin to ‘normal’ it may regain some of its former relevance.”

Taking British American Tobacco as an example, despite its long track record of upping dividends, the firm continues to face ongoing regulatory pressure.

“Investors should never take anything for granted. There have been 138 dividend cuts across the current crop of FTSE 100 members in the past decade and even if 74 of those came in the Covid-blighted years of 2019 and 2020 there were still nine in 2023,” said Mould.

Still, for those unwilling to take the risk on individual stocks, the FTSE 100’s forecast dividend yield of 3.8% for 2024 (and 4.1% for 2025) makes it an interesting option at a time when interest rates are expected to come down.

“Financial markets continue to price in three interest rate cuts of one-quarter of a percentage point apiece from the Bank of England by the end of 2024. That would take the base rate down to 4.5% and potentially weigh on UK government bond yields, to further raise the profile of the UK equity market’s income potential, at least if inflation stays relatively benign,” said Mould.

There are myriad factors to consider when investing for income, but now could be a chance for investors to put some of their cash into equities. Although it may be riskier, the prospect of capital gains and a strong starting yield mean they are a good option for the long term.

And as I wrote last week, those willing to explore further down the market capitalisation away from the FTSE 100 may be in line for even better yields in the future.

Bestinvest’s Jason Hollands picks four funds with a complementary approach to Fundsmith for investors who want to diversify manager and stock-specific risk.

With £25bn in assets, Fundsmith Equity is one the most popular and widely-held funds amongst UK retail investors but the once-mighty giant has waned in recent years, so much so that the fund was included in Bestinvest’s Spot the Dog list for the first time in the latest report.

Despite this, its long-term track record remains impressive. Between 2014 and 2021, Fundsmith Equity outperformed the IA Global sector in every calendar year. It then fell behind its peer group average in 2022 and 2023, although it has come roaring back this year so far, returning 7.3% year to date as of 17 April, versus 4.7% for the average global fund.

Given the concentrated nature of its 28-stock portfolio, with 9% apiece in Microsoft and Novo Nordisk, investors may wish to pair Fundsmith with other global equity strategies owning a different batch of stocks.

For investors who hold Fundsmith but want to add complementary strategies alongside it, Jason Hollands, managing director at Bestinvest, recommended four contenders, below.

Brown Advisory Global Leaders

Mick Dillon and Bertie Thomson, who run the $2.9bn Brown Advisory Global Leaders fund, oversee a portfolio of 30-40 stocks. Their fund has a 9% allocation to Microsoft in common with Fundsmith Equity and both strategies hold Visa but beyond that, their top 10 positions do not overlap.

Brown Advisory Global Leaders’ high conviction holdings include General Electric, the London Stock Exchange Group, Taiwan Semiconductor Manufacturing Co. and Safran, the French aerospace and defence group.

“This fund is not wildly dissimilar from Fundsmith in approach with a focus on high quality cash-generating businesses delivering positive and sustainable returns on capital. The fund has low portfolio turnover too,” Hollands said.

Despite that, this is the least correlated to Fundsmith out of all of Hollands’ suggestions, with a 0.75 correlation over the past five years. The three funds below have a 0.83-0.86 correlation to Fundsmith.

Long-term performance has been broadly in line with Fundsmith Equity, but Brown Advisory Global Leaders has pulled ahead in the past year, as the chart below shows.

Brown Advisory Global Leaders vs Fundsmith Equity and sector over 10yrs

Source: FE Analytics

GuardCap Global Equity

The $3.4bn GuardCap Global Equity fund is managed by Michael Boyd, Giles Warren, Bojana Bidovec and Orlaith O’Connor.

“Boyd and Warren have worked together for more than 25 years and have developed a highly collaborative and successful approach focused on investing in a concentrated portfolio of circa 20-25 high quality, large companies that they believe can deliver sustainable earnings growth and can be bought at attractive valuations,” Hollands explained.

Performance of fund vs sector and benchmark over 10yrs

Source: FE Analytics

The only overlap with Fundsmith in GuardCap's top 10 is Novo Nordisk. GuardCap's other significant holdings include French-Italian eyewear group Essilor Luxottica, derivatives marketplace CME Group, Alphabet and Mastercard.

Fiera Atlas Global Companies

Since inception, the $1bn Fiera Atlas Global Companies fund has trounced its sector, benchmark and the mighty Fundsmith, as the chart below shows.

Performance of fund since inception vs sector, benchmark and Fundsmith

Source: FE Analytics

The fund invests in 25-35 “exceptional growth companies with strong wealth creation credentials”, Hollands said.

Managers Simon Steele and Neil Mitchell look for companies with “competitive advantages, runways for growth and a track record of making wise capital allocation decisions, which are backed up by repeatable and diversified cash flows that can compound over time,” he explained.

The fund is benchmark unconstrained and “differs considerably from the index and many other global funds which invariably own the ‘usual’ names,” he continued.

It shares Fundsmith’s conviction in Visa and IDEXX Laboratories, which provides a range of products for veterinarians. Other large positions are in luxury products group LVMH, technological research and consulting firm Gartner, electronic design and semiconductor specialist Synopsys and animal health company Zoetis.

Evenlode Global Income

“This fund certainly brings something different to the table, as targeting companies that can grow their dividends is part of the brief,” Hollands said.

Evenlode Global Income’s managers Ben Peters and Chris Elliott look for “companies with low capital expenditure requirements, which means they can fund their own growth and pay those sustainable dividends,” he explained.

“Low leverage is another tick in the fund’s box. Peters also looks at qualitative factors, including companies with hard to replicate business models and intangible assets such as a strong brand name. The final portfolio is concentrated, currently holding 28 stocks with the intention being to hold them for the long term.”

Evenlode Global Income is comfortably ahead of the IA Global Equity Income sector over 10 years but it has not kept pace with Fundsmith, reflecting the differences in the two strategies’ mandates, with the former delivering steady income and the latter focusing on growth.

Performance of fund vs sector and Fundsmith over 10yrs

Source: FE Analytics

Microsoft is the only overlap with Fundsmith’s top 10; it is the second-largest position in Evenlode Global Income, worth 4.3% of the fund.

Other high conviction holdings include Unilever, consultancy Accenture, professional data and software provider Walters Kluwer and healthcare technology company Medtronic.

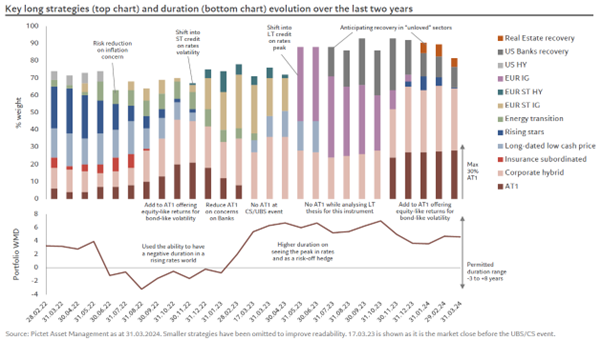

Pictet Asset Management expects strategic credit portfolios to deliver high returns due to the elevated yields on offer.

‘It was the best of times, it was the worst of times.’ The opening lines of ‘A Tale of Two Cities’ by Charles Dickens is an apt description of the fixed income markets for the past couple of years, although the bad times in 2022 and early 2023 preceded the good.

For bonds, it currently looks like the best of times. Yields across the board are attractive and the income is back in fixed income – even though spreads are below long-term averages.

The high starting yields mean that strategic bond portfolios should be capable of delivering returns in the mid-to-high teens, said Jon Mawby, co-head of total and absolute return credit at Pictet Asset Management.

“That sort of return would be expected over an 18-24 month horizon if rates stay elevated. It would be possible over 12 months only if yields fall (e.g. due to a rate cutting cycle) and then bonds could benefit from significant capital gains,” he explained.

Further rate hikes would be detrimental for fixed income but returns should still be flat to slightly positive because yields are so high that they provide an element of protection, he continued.

“You’re being paid for the risk. If you’ve got the ability to be nimble, dynamic and strategic with no cognitive bias, it’s actually a great environment for the asset class.”

Maximum confusion amongst investors and central bankers

Yet despite the potential for high returns, many investors remain uncertain and are sheltering in cash and money market funds. Mawby described the current environment as one of “maximum confusion” because the dynamics of a normal economic cycle have been disrupted by massive fiscal stimulus after the pandemic.

Government spending cushioned consumers and businesses from feeling the full impact of rate hikes, throwing the “long and variable lag playbook” out of the window, he said. “These lags are going to be longer and they’ll probably be more variable. That is really what’s causing maximum confusion among central banks and the market.”

Mawby thinks the US Federal Reserve needs to cut rates soon or risk losing its window of opportunity because it would be politically unviable to introduce the first cut just before the November presidential election, lest the Fed be accused of trying to bail out the Democrats. “You know what the politics are going to be. I’d hate to be a central banker,” he confessed.

Mawby thinks the Fed needs to see “a shaft of light” to have the impetus to change course and believes that the yield curve needs to steepen, especially at the front end, before substantial cuts are implemented.

All that said, macroeconomic signals are divided with a cost-of-living crisis on one hand and better than expected economic data on the other. “I’m probably more confused than I’ve ever been about whether people are greedy or fearful,” Mawby said.

On the greedy side, equity market valuations look stretched, but on the fearful side, there is lingering distrust of fixed income following ‘the worst of times’ in 2022.

Investors in fixed income want three things, Mawby said: income; capital protection during times of stress; and diversification from risk assets. Fixed income failed to deliver on these criteria in 2022 and instead “super-charged risk”, which is why there is “maximum fear” surrounding bonds. That explains some savers’ preference for cash.

Where to invest in the bond market

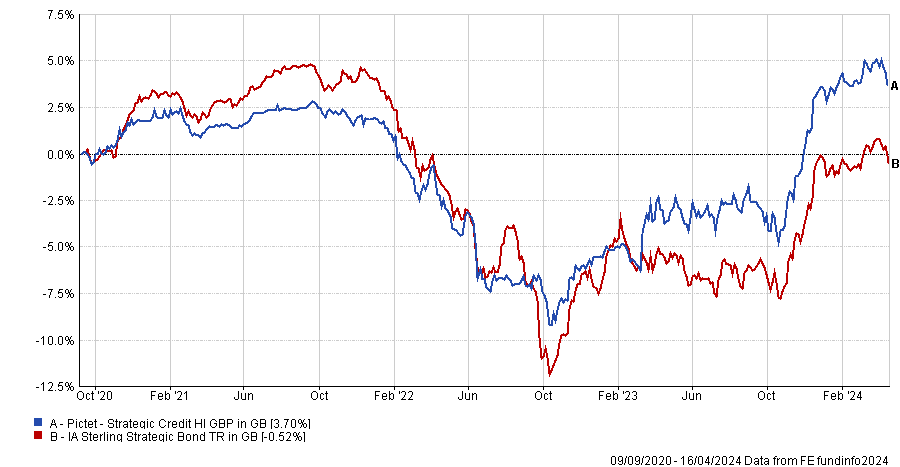

Fortune favours the brave and Mawby is looking for contrarian, undervalued opportunities for his Pictet Strategic Credit fund, which has an FE fundinfo Crown Rating of five (indicating that it is within the top 10% of funds in its sector for alpha, volatility and consistent outperformance).

Performance of Pictet Strategic Credit vs sector since inception

Source: FE Analytics

At the end of last year, he began building a position in additional tier 1 debt (AT1s), which were offering equity-like returns for bond-like volatility due to the elevated coupons on offer. “Everyone hated AT1s”, Mawby said, because investors were still spooked after Credit Suisse’s AT1 bondholders were wiped out as part of the forced merger with UBS in March 2023.

Although Mawby believes that AT1 instruments were designed to absorb losses, the Credit Suisse situation was unique; AT1s would not be written down to zero in the same way elsewhere in Europe or in the US, he said.

With the US regional banking crisis over, the outlook for the banking sector now appears more certain and AT1s look attractively-valued. They account for almost 30% of the Pictet Strategic Credit fund and he expects them to outperform as the yield curve steepens.

The Pictet Strategic Credit fund’s AT1 exposure

Another high conviction allocation is to short call hybrids with calls in 2024 to 2027 and yields from 4% to 6.5-7%.

“The carry or income is among the highest in the credit space thanks to the inverted yield curves and additional spread on offer in these subordinated bonds,” Mawby explained. “The issuers we hold are typically well-known or ‘national champion’ investment-grade-rated companies, where we are comfortable to harvest the additional carry through their subordinated debt.”

The macro environment is largely favourable for emerging market debt and the asset class offers an immense opportunity to invest across different regions, countries, industries, currencies and ratings.

While fund flows into emerging market debt have struggled due to global headwinds, investment performance has been quite resilient. Last year, emerging market hard currency indices and local currency indices delivered low double-digit returns.

This was amid an aggressive Federal Reserve hiking cycle, heightened US Treasury yield volatility, a disappointing post-Covid China reopening, looming geopolitical risks and two major wars.

The resilience of the asset class has been impressive, attributable to improving institutional strengths, a lengthening history of prudent macroeconomic policies and the hard-fought credibility of central banks, in particular in their disciplined response to inflation.

Companies operating in these emerging countries have benefitted from this structural framework, enabling them to successfully access the international capital markets while at the same time developing and strengthening their local funding sources.

If US rate volatility eases, we could see fund flows turn positive as investors rotate back into the asset class given the attractive yield and spread pick-up relative to developed market credits.

In addition, the technicals for the asset class remain supportive thanks to a significant reduction in new external bond issuance over the past few years, combined with a prominent level of tenders, buybacks and calls. This has led to a shrinking emerging market debt stock.

Globally, it appears likely that we will see a disinflation cycle continuing through 2024. Developed market central banks, including the US Federal Reserve, have removed their hiking bias and are expected to begin easing monetary policy from restrictive levels this year.

Many emerging market central banks, which had hiked rates earlier and more aggressively than their developed market counterparts, have already begun to ease. On balance, investors could expect more accommodative monetary policy to support economic growth and favour the growth differential between emerging and developed markets.

China, the world’s second largest economy, should continue to grow around 5% for 2024. If needed, Beijing appears ready to increase support to prevent a sharp domestic growth slowdown. Policy support is likely to include liquidity measures, proactive fiscal policy and monetary support.

A key trend that investors should be monitoring is market implications for the US election in November this year. Whoever wins, the next administration is expected to continue supporting US domestic growth. Geopolitical risks need to be carefully monitored as they are the most likely potential source of economic headwinds.

The dollar is anticipated to be somewhat rangebound over the near term, which is beneficial to the emerging market carry trade and dampens volatility in emerging market foreign exchange.

Over the medium term, broad dollar weakness is likely as the Fed begins a cutting cycle and global growth rebounds with support from China, while a deteriorating fiscal outlook in the US may deter dollar dominance.

A global recession, the US election cycle and an escalation of geopolitical conflicts are some of the key risks to emerging markets to monitor this year. However, even if these risks materialise, active managers can weather the storm through credit selection within chosen countries, regions and sectors.

Emerging market economies are certainly vulnerable to a global recession. However, within a shallow growth deceleration, the higher quality credits with high carry may benefit, as emerging market credit spreads may widen less than the compression in Treasury yields.

Emerging market debt faces a potential headwind of heightened political uncertainty related to US foreign policy. There could potentially be an increase of volatility leading up to the US presidential election as candidates campaign on a return to protectionist policies. However, in the recent past, divisive campaign rhetoric toward foreign countries has been more a starting point for bilateral negotiations.

Additionally, some countries stand to benefit from these policy shifts, in particular from near-shoring and friend-shoring as the US and EU move supply chains away from China.

While geopolitical risks are hard to quantify and trade, certain regions are better able to weather these risks. Latin America remains more insulated from conflicts within the Middle East, Europe and Asia. Indeed, commodity-linked economies, which tend to be low-cost producers, may benefit from higher commodity prices.

The asset class is a secular improving story that offers an immense opportunity to invest across different regions, countries, industries, currencies and ratings.

Opportunities lie within the emerging countries which have institutional strengths, supportive growth outlooks and increasing linkages to developed markets, such as those within Latin America, with favourable outlooks in both Mexico and Brazil. Latin America remains more insulated from geopolitical risks and stands to benefit from a near-shoring trend that is already beginning to boost foreign investment, particularly in the case of Mexico.

Emerging market corporates have evolved into an asset class of their own, with a market capitalisation that far exceeds that of emerging market sovereigns and the US high-yield bond market.

The fundamentals for emerging market corporates have remained quite resilient despite the macro uncertainties, thanks to overall conservative financial policies. Moreover, emerging market corporates offer an attractive spread pick-up relative to emerging market sovereigns and comparably rated developed market credits.

Within emerging market corporates, we tend to favour the sectors that are strategic, i.e. those sectors deemed necessary for the smooth functioning of their domicile countries. These sectors include banking, utilities, natural resources and transportation.

All said, the macro environment is largely favourable for emerging market debt with opportunities to invest in countries that have a strong domestic story and in corporate credits, which have strong to improving credit fundamentals and a dedicated local investor base.

Su Fei Koo is a portfolio manager at DoubleLine. The views expressed above should not be taken as investment advice.

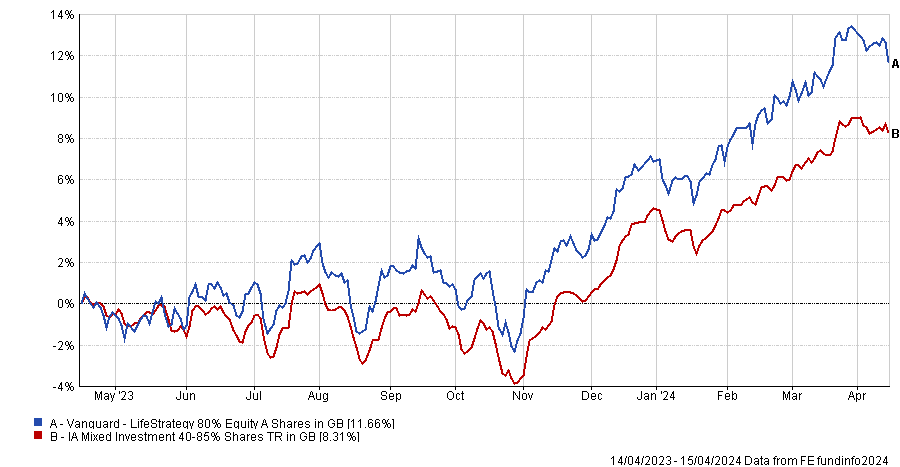

Savers abandon Vanguard LifeStrategy 40% Equity yet flock to Vanguard LifeStrategy 80% Equity.

Investors withdrew more than £250m apiece from defensive funds such as Ruffer Total Return, Vanguard LifeStrategy 40% Equity, Troy Trojan and Baillie Gifford Managed during the first quarter of 2024 in favour of more equity-heavy portfolios.

At the other end of the spectrum, the most popular multi-asset fund by far was Vanguard LifeStrategy 80% Equity, which netted £378m during the first quarter, data from FE Analytics revealed.

It grew its assets from £10bn to £11bn during the quarter, with investment performance adding almost twice as much as inflows. The fund has benefitted in recent months from its relatively high equity allocation versus its sector during a bull market, as the chart below shows.

Performance of fund vs sector over 1yr

Source: FE Analytics

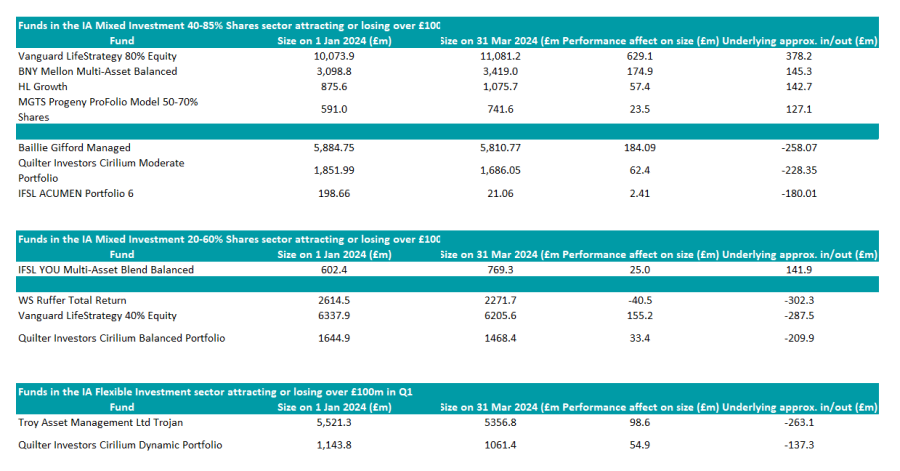

In this series, Trustnet scrutinised fund flows data for the IA Flexible Investment sector and the three IA Mixed Investment sectors to uncover which funds gained or lost more than £100m. No funds in the IA Mixed Investment 0-35% Shares sector had such large flows but a list of the most and least popular funds in the other sectors is below.

Multi-asset funds attracting or losing more than £100m in Q1 2024

Source: FE Analytics

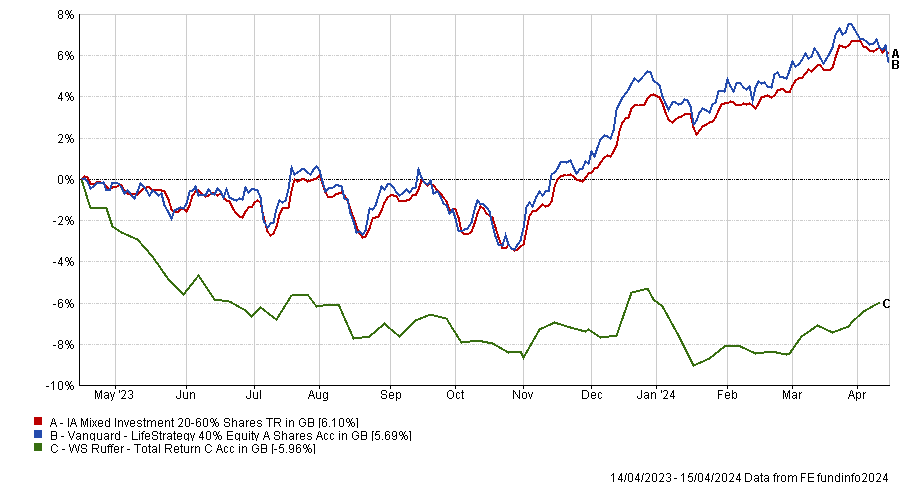

Several large funds run by well-known managers suffered outflows this year. Investors pulled £302m out of the £2.3bn Ruffer Total Return fund, which lost an additional £40m through poor performance, making it the only strategy with negative returns on the list above.

Ruffer has been betting on the yen’s recovery and has a bearish view of equity markets. Its derivative positions, which are focused on credit default swaps and on protecting against equity market downside risk, have “dragged” on performance, Ruffer said in its March 2024 factsheet.

Vanguard LifeStrategy 40% Equity was hit by similar outflows of £287.5m, despite its performance sitting around the sector average.

Performance of funds vs sector over 1yr

Source: FE Analytics

Investors also pulled £263m from Troy Asset Management’s £5.4bn Trojan fund, which is known for its conservative stance and emphasis on capital preservation.

The fund only has 28% in equities, which have rallied strongly in the past five months or so, leaving the Trojan fund far behind its average peer in the IA Flexible Investment sector, as the chart below shows.

Performance of fund vs sector over 1yr

Source: FE Analytics

The Trojan fund has a large bond allocation with 36% in US Treasury inflation-protected securities, 13% in short-dated gilts, 8% in short-dated US Treasuries and 3% in index-linked gilts.

Besides bonds, its largest holdings are iShares Physical Gold and Invesco Physical Gold, which together account for 11.7% of the portfolio. In March 2024, the gold price surged to new highs in all major currencies as geopolitical risk remained elevated, bolstering the Trojan fund, which has held gold for many years for diversification and portfolio insurance.

Meanwhile, Baillie Gifford Managed had the fourth-largest outflows amongst all multi-asset funds. A core growth portfolio with an emphasis on bottom-up stock picking, the fund’s top 10 holdings include Amazon, Nvidia, Meta, Taiwan Semiconductor Corp. and ASML.

Performance of fund vs sector over 1yr

Source: FE Analytics

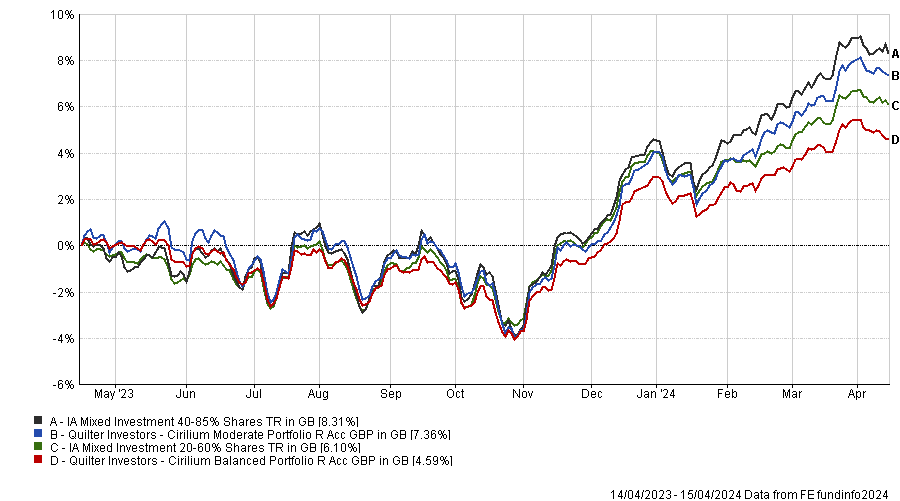

Three of Quilter Investors’ multi-manager Cirilium portfolios – the moderate, balanced and dynamic iterations – lost more than £100m each in outflows.

The £1bn Cirilium Dynamic Portfolio outperformed the IA Flexible Investment sector over the year to 15 April 2024, returning 9.6% versus 8.6% for the sector average, but its larger moderate and balanced stablemates trailed their respective sectors.

Performance of fund vs sector over 1yr

Source: FE Analytics

The Cirilium range is in relatively new hands, having been led since December 2022 by Ian Jensen-Humphreys and Sacha Chorley, who replaced Paul Craig and Hinesh Patel.

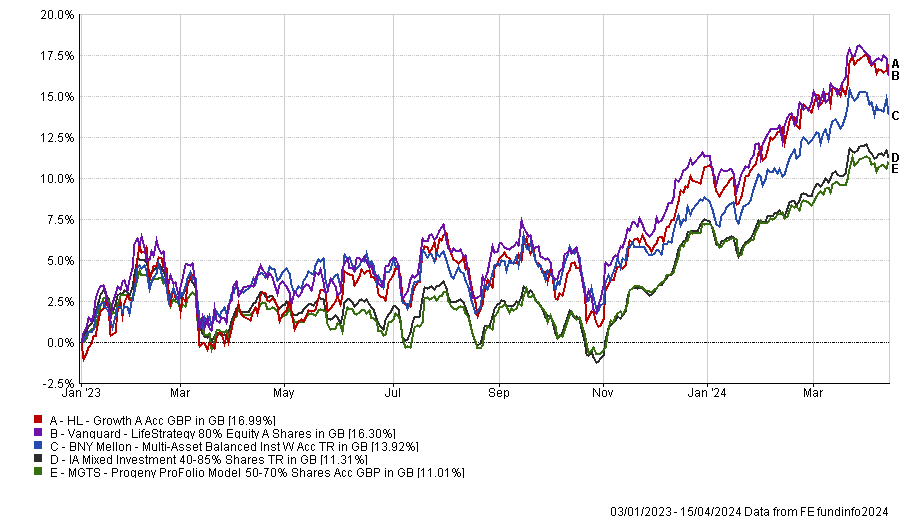

Four funds in the IA Mixed Investment 40-85% Shares sector received more than £100m in inflows apiece. In addition to the popular Vanguard LifeStrategy 80% Equity fund, investors also backed BNY Mellon Multi-Asset Balanced, Hargreaves Lansdown’s HL Growth fund and MGTS Progeny ProFolio Model 50-70% Shares.

The £1bn HL Growth fund is the strongest performer in this group with top-quartile returns, as the chart below shows.

Launched in December 2021, HL Growth allocates to a range of passive strategies, most of which are run by Legal & General Investment Management. Its largest holding is a 33% allocation to the L&G Future World ESG Developed Index fund and it also has 14.5% in L&G Future World ESG North American Index and 13% in L&G Future World ESG Emerging Markets Index.

Performance of funds vs sector over 1yr

Source: FE Analytics

BNY Mellon Multi-Asset Balanced is managed by FE fundinfo Alpha Manager Bevin Shah alongside Paul Flood and Simon Nichols. It has top-quartile performance over three and five years and a FE fundinfo Crown Rating of five (the highest score based on alpha, volatility and consistent outperformance). Its largest holdings are Microsoft, RELX and Shell.

ISFL YOU Multi-Asset Blend Balanced was another winner, taking in £142m from investors during the first quarter. The £769m fund has achieved top-quartile performance over three years and second-quartile returns over the 12 months ending 15 April 2024. It was established in 2019 and is part of YOU Asset Management’s range of model portfolios and funds.

Fidelity India Focus, Morant Wright Japan and Jupiter Merian Asia Pacific have outperformed year in, year out.

The ability to consistently beat a benchmark is what makes a great active manager.

In the Investment Association Asia sectors, no funds managed to outperform the most common benchmark in their peer groups every single year for the past decade, although some funds achieved that feat in eight of the past 10 years. For Japan, seven years of outperformance was the high water mark.

To help investors select the funds that justify their fees, Trustnet highlights below which IA China, IA India, IA Japan and IA Asia Pacific Excluding Japan strategies can claim the title of the most consistent funds of the decade.

We used FE Analytics data and only considered funds with 10-year track records.

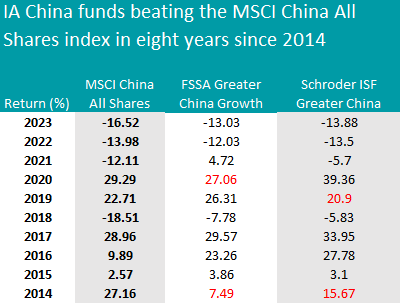

We begin with the IA China sector, where only two funds managed to consistently beat the most common benchmark of the peer group, the MSCI China All Shares index, since 2014 – FSSA Greater China Growth and Schroder ISF Greater China. Both have outperformed in eight years out of the past 10.

The former is a £428.5m benchmark-agnostic, multi-cap strategy co-managed by FE fundinfo Alpha Manager Martin Lau and Helen Chen, who has been working on the fund since 2019.

Square Mile analysts said that Lau and Chen focus on quality businesses, selected with a “rigorous bottom-up research process, where company and country visits help build their collective knowledge and assessment of a business's growth sustainability, franchise, financial strength and management.

“Overall, we see this fund as a very strong and wholly viable option for long-term investors who wish to access the greater China region in a more conservative manner, where the emphasis is on identifying high quality growth companies,” the analysts said.

In the past decade it underperformed the reference index in 2020 and 2014 only, as the table below shows.

Source: Trustnet, MSCI (for the 2014 index performance). The red highlights represent underperformance against the reference index.

The $2.2bn Schroder ISF Greater China portfolio managed by Louisa Lo achieved a similar performance – the two funds are in fact 95% correlated to each other and have a similar split between Asia Pacific equities and Asia Pacific emerging equities (14% and 84% approximately).

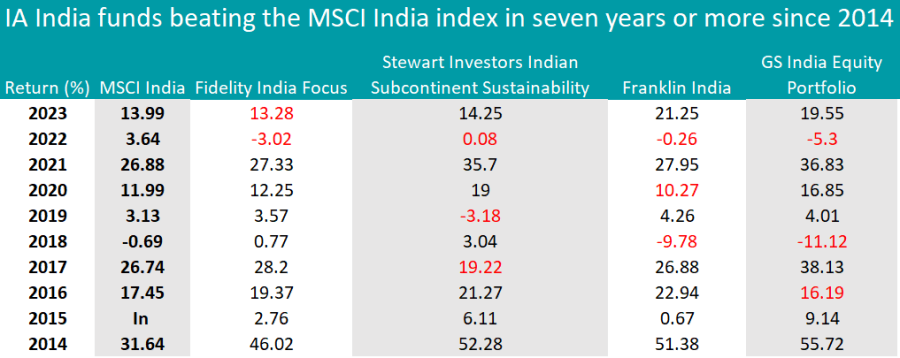

In the IA India sector, managers struggled to beat the most common benchmark, the MSCI India, during the past 10 years.

The only fund to achieve this feat in eight years out of 10 was the $2.5bn Fidelity India Focus fund managed by Amit Goel, who invests in sustainable businesses that are market leaders in sectors that benefit from India’s growth opportunities.

His current overweights compared to the MSCI India Capped 8% Index are financials (6.2 percentage points on top of the index’s 25%) and consumer discretionary (6.2 percentage points on top of the index’s 12.9%), while the main underweights are energy (where the fund remained 6.6 percentage points below the index at 4.1%) and utilities (which the fund doesn’t own but make up 4.6% of the index).

Source: Trustnet. The red highlights represent underperformance against the reference index.

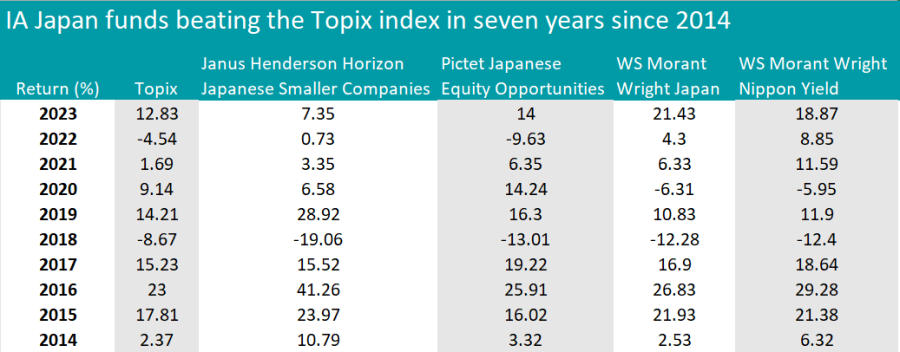

In the IA Japan sector, the Topix index proved to be a high hurdle to beat, with no more than four strategies outperforming it in seven years of the past decade – two of which are from the same provider, Morant Wright.

WS Morant Wright Japan and WS Morant Wright Nippon Yield are two similar strategies (98% correlated to each other), both with a FE fundinfo Crown Rating of five.

The management team is unconstrained from any benchmark and can choose companies across the market-cap spectrum.

The Nippon Yield fund’s value-style approach has become a large headwind in recent years, as Square Mile analysts noted. However, “while this has meant the fund has struggled, it has continued to present superior returns over its stylistic biases,” they said.

“There are risks involved with this strategy and the approach appears simplistic, but we believe this fund is a strong value option with a disciplined approach and focused team.

“The fund would suit investors who want to diversify their Japanese equity exposure but also those that are willing to accept volatility versus the benchmark over shorter periods.”

Source: Trustnet. The red highlights represent underperformance against the reference index.

Another strategy of note was the Janus Henderson Horizon Japanese Smaller Companies fund, managed by FE fundinfo Alpha Manager Yunyoung Lee, who has been in charge since 2005.

The portfolio now includes 53 holdings, 28% of which are in the industrial sector. At 14.8%, technology is a slight overweight for the fund against its benchmark, the Russell/Nomura Small Cap index, which has 12% in the sector. The biggest underweight is consumer discretionary (11.9% versus 20.8% in the index).

The only other fund in the table was Pictet Japanese Equity Opportunities, an Article 8 strategy investing in undervalued companies. Its top holdings include Toyota (4.9%), Mitsubishi (3.81%) and Sony (3.3%).

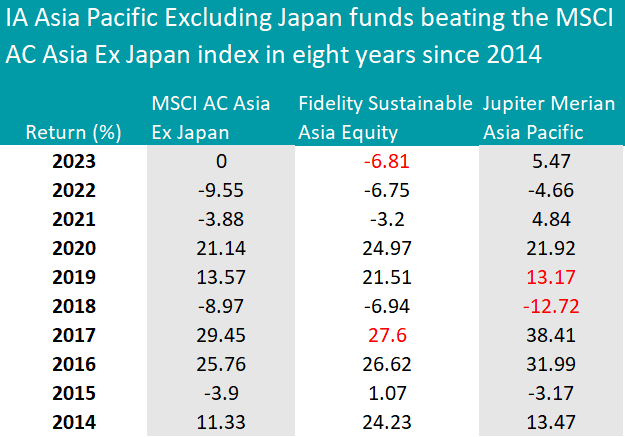

Finally, the standout vehicles in the IA Asia Pacific Excluding Japan sector were Fidelity Sustainable Asia Equity and Jupiter Merian Asia Pacific, both of which outperformed the MSCI AC Asia Pacific ex Japan index in eight years since 2014.

Source: Trustnet. The red highlights represent underperformance against the reference index.

Fidelity Sustainable Asia Equity is an £80m fund managed by Dhananjay Phadnis, who employs a quality-growth approach to select companies with sustainable returns that are mispriced or unrecognised by the market.

Jupiter Merian Asia Pacific, led by Ian Heslop, was described by Rayner Spencer Mills Research analysts as a highly-diversified long-only benchmark-aware portfolio that has consistently outperformed since the current management team took over in December 2011.

“The team has developed a systematic model over time which is now used in seven equity strategies at Jupiter and each of these strategies has delivered top quartile performance since launch with the first strategy dating back to 2005,” they said.

“This tried and tested process gives investors a strong option for investing in Asian equity markets.”

This article is part of an ongoing series on consistency. Previous instalments covered the following asset sectors: Emerging Markets, IA Global, Europe, IA UK Equity, IA UK Equity Income, UK Small Caps, UK bonds, cautious funds, balanced funds, adventurous funds, technology, healthcare and financials.

Jupiter Asset Management has the most Hall of Fame members, with five of its fund managers holding an Alpha Manager rating for at least seven years.

Six active managers have joined FE fundinfo’s Alpha Manager ‘Hall of Fame’ for the first time today, meaning they have earned an Alpha Manager rating for seven consecutive years or more.

The six new entrants are: David Walton, who runs IFSL Marlborough European Special Situations; Claudia Calich of M&G Emerging Markets Bond; Yunyoung Lee at the helm of Janus Henderson Horizon Japanese Smaller Companies; Aziz Hamzaogullari of TM Natixis Loomis Sayles US Equity Leaders; Kristian Heugh, who runs Morgan Stanley Investment Management’s MS INVF Global Opportunity fund, among others; and Polina Kurdyavko, who manages several emerging market debt funds for RBC BlueBay Asset Management.

The Hall of Fame includes 46 managers, seven of whom have been members consistently ever since they joined the group: Richard Woolnough from M&G Investments, John Chatfeild-Roberts and Daniel Nickols from Jupiter Asset Management, David Dudding from Columbia Threadneedle Investments, Martin Lau from FSSA Investment Managers, Mark Slater from Slater Investments and Leigh Himsworth from Fidelity International.

Jupiter has the most managers – five – in the Hall of Fame, followed by Fidelity with four, and three managers each from Schroders, Morgan Stanley and Janus Henderson.

Charles Younes, deputy chief investment officer, FE fundinfo, said: “Those in the Hall of Fame have risen above the market volatility of recent decades, delivering above-average returns during unprecedented circumstances such as multiple economic crashes, a global pandemic and a host of geopolitical conflicts.”

FE fundinfo’s Alpha Manager ratings recognise the top 10% of managers running funds for UK retail investors, based on investment performance during their entire careers. The ratings assess managers’ risk-adjusted alpha, consistency of outperformance versus their benchmark and outperformance in both up and down markets. Managers with longer track records of outperformance are accorded extra weighting in the rankings to recognise the benefits of experience.

Experts explain the differences between the two trusts, share their preferences and suggest strategies to complement them.

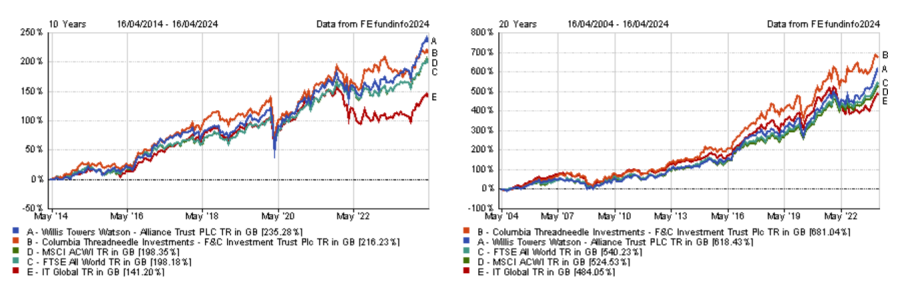

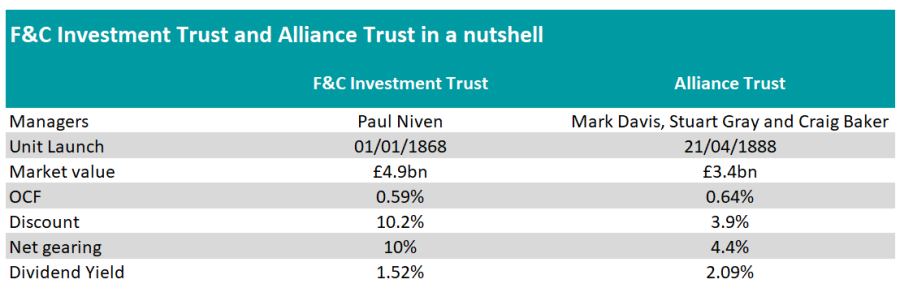

F&C Investment Trust and Alliance Trust are among the largest investment trusts in the IT Global sector and have a long history dating back to the 19th century, making them popular choices as one-stop-shops for core exposure to global equities.

Investors might have a hard time choosing between the two, as they seem very similar at first glance. Both take a multi-manager approach, are well diversified and are aligned with global benchmarks from a country and sector perspective.

Historical performance may not help investors distinguish between the trusts, either. Alliance has had the upper hand over the past decade, but F&C has performed better over 20 years.

Performance of trusts over 10yrs and 20yrs vs sector and benchmarks

Source: FE Analytics

Trustnet asked experts to explain the differences between the two portfolios, to share which one they favour and to suggest other trusts to complement them.

How do Alliance Trust and F&C differ from each other?

Although both funds use a multi-manager structure, there are nuances. F&C invests in funds run by 13 managers, resulting in a portfolio comprising approximately 400 stocks, whereas Alliance Trust uses segregated mandates to get access to its 10 managers’ top 20 holdings.

Aidan Moyle, investment analyst at Hargreaves Lansdown, said: “This gives Alliance a higher conviction approach in their managers’ best ideas and results in a portfolio of 200 stocks from 10 managers. The use of segregated mandates also gives them access to managers that aren’t available to UK retail clients.”

Nicholas Todd, investment trust research analyst at Kepler Partners, countered that using funds makes it easier for F&C’s manager Paul Niven to adjust the portfolio tactically, depending on his outlook.

As a result, F&C has a greater style bias at times, which may impact short-term performance based on whether Niven makes the right call or not.

For instance, the trust significantly underperformed its benchmark over the past 12 months. Niven positioned the portfolio towards value stocks at the beginning of 2023 and missed the ‘Magnificent Seven’ rally as a result, although he shifted to a more balanced exposure during the year.

Performance of trusts over 1yr vs sector and benchmarks

Source: FE Analytics

Another difference is F&C’s exposure to unquoted investments, which has been a “valuable source of alpha” for four out of the last five financial years and offered “good diversification”, according to Todd.

Dan Coatsworth, investment analyst at AJ Bell, pointed out that private companies are less liquid, which may explain why F&C trades on a deeper discount of 10.2% versus 3.9% for Alliance Trust.

Both trusts are ‘dividend heroes’; Alliance Trust has raised its dividend for 57 consecutive years, while F&C has done so for 53 successive years. Yet, Alliance Trust has a bigger dividend yield at 2.05% versus 1.48% for F&C.

Coatsworth said: “Alliance Trust made a strategic decision in 2021 to boost its dividend payments and make the investment trust more attractive to a bigger pool of investors.

“This level of yield is still small versus what’s on offer from equity income-specific trusts but the combination of income and growth is why certain investors want to own the shares.”

Which trust do experts favour?

James Carthew, head of research at QuotedData, said Alliance Trust changed its strategy seven years ago, which was a turning point. The board appointed Willis Towers Watson to run the trust in 2017 and became more aggressive about tackling the discount. Around £1bn worth of shares have been bought back since then.

“Even though Alliance Trust’s new investment strategy is only seven years old, the trust’s returns have already made up the underperformance earlier in the decade. Its 10-year returns have now pulled ahead of F&C’s (12.6% per annum on average to F&C’s 12.0%),” Carthew said.

“It feels to me as though the gap will only get wider. If I had to choose between the two, Alliance Trust is the obvious favourite.”

Mick Gilligan, head of managed portfolio services at Killik & Co, prefers F&C due to its wider discount.

Meanwhile, Moyle believes F&C may be better positioned if central banks cut interest rates due to its 10% allocation to unlisted equities.

“If rates were to start falling, there could be a change in sentiment and investors could start moving more risk-on and increasing exposure to private companies,” he said.

Source: FE Analytics

How to complement them?

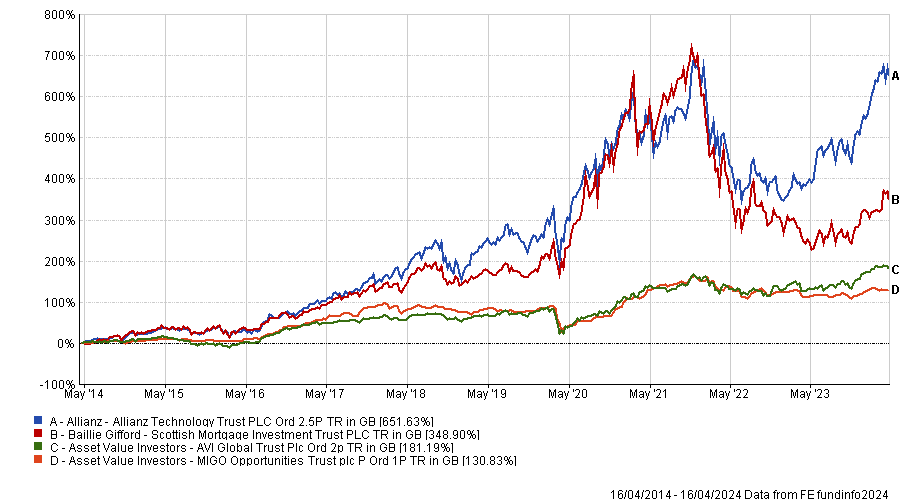

As both trusts are highly correlated to global equity benchmarks, Todd suggested complementing them with specialist exposures, such as Allianz Technology Trust.

He said: “It focuses on the tech sector, specifically at the lower end of the market cap spectrum, targeting the ‘picks and shovels’ companies which portfolio manager Mike Seidenburg believes have longer pathways for growth.

“However, there is an allocation to the Magnificent Seven which investors should be aware of as it may limit the diversification benefits. That said, it trades on a discount of 11.6%, which in a notoriously expensive sector looks attractive.”

Performance of trusts over 10yrs vs sector and benchmarks

Source: FE Analytics

Alternatively, Todd would consider Scottish Mortgage, AVI Global Trust or MIGO Opportunities.

“The high allocation to private markets in Scottish Mortgage would likely provide a diversifying source of returns and, despite its high volatility, a small allocation of an investor’s risk bucket may be warranted,” he explained.

“Similarly, something like AVI Global Trust or even MIGO Opportunities would offer a good source of diversification and at this juncture look attractive ways to benefit from an easing macro environment given their focus on discounted opportunities.”

As F&C and Alliance Trust are large-cap core portfolio, Todd also suggested adding The Global Smaller Companies Trust, which offers a balanced and core exposure to small-caps.

Performance of trusts over 10yrs vs sector and benchmarks

Source: FE Analytics

He said: “There is an 18% allocation to collective investment vehicles to utilise the expertise of managers in Asian and emerging markets, and a 25% allocation to UK smaller-cap equities which have been particularly hard hit.

“The focus is on quality and identifying growth at a reasonable price, which means the managers avoid more speculative areas of the market.

“The trust offers a yield of 1.5% which is rare to see across smaller companies’ strategies and may provide a source of diversification away from typically large-cap focused global equity strategies. A discount of -12.3% may provide an added licker to returns over the long term.”

Any investment trust with a market capitalisation below £200m might be considered sub-scale, although some large investors may even prefer £1bn.

Size is becoming an increasingly important factor in the investment trust market. A larger war chest has always had its advantages because it implies – but not always means – that a closed-ended fund benefits from a stronger liquidity profile, a broader shareholder register, easier access to borrowing facilities, more firepower in terms of discount control and better capital allocation policies.

Moreover, bigger funds can spread their fixed costs over a wider asset base and therefore reduce cost ratios, while scale gives them headroom for share buybacks.

However, another factor contributing to the preference for bigger market capitalisations is the consolidation of wealth management firms. As they are now managing larger sums of money, it can be challenging for them to buy and sell smaller investment trusts.

Elliott Hardy, an investment trust analyst at Winterflood, said: “Wealth managers and institutional investors are better able to invest in larger investment trusts across multiple portfolios/strategies without becoming too large a part of the share register, while funds that see their market caps grow sufficiently to enable inclusion in FTSE indices can benefit from further improved liquidity and passive inflows as a result.”

What is considered sub-scale?

A market cap of £200m is commonly considered to be the bare minimum for an investment trust.

In fact, Winterflood’s latest industry survey revealed that only 62% of investors would consider a closed-ended fund below £200m, whereas a decade ago almost all respondents (99%) were prepared to look at smaller trusts. Meanwhile, 8% of investors now require a size of £400m or more.

Those figures echo the preferences of discretionary investment management firm Quilter Cheviot, which considers anything below £200m as sub-scale and tends to prefer a market cap of at least £250m.

While also seeing £250m as its threshold, Killik & Co indicated that others may even require a size of £500m, if not £1bn.

Few closed-ended funds can pretend to match the latter requirements. Data from Peel Hunt shows that out of circa 300 investment trusts, approximately 50 of them boast a size of £1bn or larger, while 200 have a market capitalisation below £500m and 120 under £200m.

Anthony Leatham, investment companies research analyst at Peel Hunt, said liquidity can be an issue. “The average daily traded value of the trusts above £1bn market cap is c.£6.5m (including 3i Group). For the remaining trusts, the average drops to £670,000 per day.

“This can have a big influence on what is considered sub-scale as it is not just an investment decision but also a risk-management decision.”

Why size can be a misleading indicator

While size has become crucial for many investors, it can be deceptive. For example, size alone does not say enough about the composition of the shareholder register.

Hardy said: “Take for instance a fund with a market capitalisation of £500m but a shareholder register of only five large institutional investors, each with 20% ownership.

“Those incumbent investors may find it difficult to exit the fund without significantly moving its share price – relative to investors within a £250m fund with a diverse shareholder register across institutional and retail investors, each with different investment horizons and motivations for buying and selling at certain times.”

Moreover, a larger size can be a problem for investment trusts focusing on the lower end of the market capitalisation scale.

Leatham said: “In a previous role, I looked at the deterioration of alpha generation from a very large open-ended equity fund and, after detailed analysis, we found the reason – the strategy generated the majority of its historic outperformance from investing in small-caps and, as the fund size expanded rapidly, the ability for the fund to participate in the smaller end of the market reduced and the proportion of the small-cap exposure also reduced.

“Investment trusts are unlikely to experience the same level of growing pains but there is a risk that very large, multi-billion-pound vehicles can become unwieldy and struggle to deploy capital into smaller, less liquid investment opportunities.”

Some investment trusts are aware of this potential issue and try to come up with solutions to avoid building too large positions in their underlying companies. For instance, River & Mercantile UK Micro Cap returns capital to shareholders when its net asset value exceeds £100m.

Where investors can benefit from a smaller market capitalisation

A small market capitalisation is a double-edged sword and can be an advantage for fund managers who may be better positioned to uncover hidden gems.

Leatham said: “If we look at our datasheet and focus on performance by the smaller trusts (<£200m market cap), the top performing 40 trusts have delivered an average share price total return of 22% over the last 12 months, outperforming the FTSE All-Share return of c.7% over the same period.”

An example he provided is Ashoka India Equity, which launched in July 2018 with a market cap below £50m, but a “clear and differentiated” investment approach and “robust structuring” in terms of fees and discount control.

Fast forward to today, the trust has delivered approximately 22% annualised share price total return compared to 13% for the MSCI India index and boasts a market cap of £378m.

Leatham added: “Investors with a strict size-based exclusion criteria risk missing out on some exceptional investment opportunities.”

Performance of investment trust since launch vs sector and index

Source: FE Analytics

Based on the success of Ashoka India Equity, Mick Gilligan, head of managed portfolio services at Killik & Co, sees good prospects in its stablemate Ashoka WhiteOak Emerging Markets, which follows the same investment process but applied to the whole emerging markets universe.

The trust was launched last year and currently has a market cap of £35m.

Gilligan also likes the previously mentioned £51m River & Mercantile UK Micro Cap to fish into the smaller echelons of the UK stock market.

Performance of investment trust since launch vs sector

Source: FE Analytics

Finally, smaller investment trusts tend to trade on wider discounts as larger institutional players may be reluctant or unable to invest in those trusts effectively.

As a result, investors may be able to take advantage of such price dislocations or benefit from corporate activity.

Leatham said: “We have seen a notable pick-up in M&A activity recently, particularly combinations with larger or better-rated peers – often including a full or partial cash exit opportunity and often involving a common management entity.

“If size continues to be of importance to investors, then we expect to see further consolidation across the investment trust universe.”

Recent mergers in the investment trust space have included the combination of JPMorgan UK Smaller Companies and JPMorgan Mid Cap, the acquisition of abrdn China by Fidelity China Special Situations and the absorption of Atlantis Japan Growth Fund and abrdn Japan Investment Trust by Nippon Active Value Fund.

Investors should not overlook the domestic market.

The UK market currently offers an unprecedented buying opportunity given valuations are unjustifiably low. This view is well supported by the recent flurry of UK targeted M&A at extremely attractive premiums.

Alongside compelling valuations, there are also signs that the Bank of England will ease its monetary policy as inflation comes under control. We think this backdrop, which gradually moves us on from the more turbulent macro conditions of recent years, should bolster the UK’s appeal to investors.

Investors should therefore not overlook the market standing at these historically low levels, or the many successful British listed companies available at bargain prices that can be tapped into.

Aerospace and defence demand

Whilst most people might associate Rolls Royce with luxury vehicles, the stock is actually a powerful player in the aerospace market. It has become the world’s leading engine supplier in business aviation, powering some of the largest, fastest, and longest-range business jets available.

Today more than 3,300 of these aircraft are in service worldwide, helping companies to improve business efficiency, productivity and enabling economic growth.

Rolls Royce’s new management team has been instrumental in turning the business around, improving both cashflow and profit margins. The firm has also benefitted from increased demand for flight travel in a post-Covid era, with ageing fleets that need ongoing service and maintenance.

Within the sphere of defence spending, which has become a heightened priority in most Western countries, BAE Systems, which provides some of the world’s most advanced, technology-led defence, aerospace and security solutions, is currently experiencing a significant order book as companies seek to address potentially decades' worth of defence underspend.

Consumer manufacturers – hobby miniatures

Games Workshop is the global leader in tabletop miniature gaming with a long-standing reputation for producing 30 million high quality miniatures per year for its iconic Warhammer worlds.

The company is differentiated by its scale, expertise, and control of every aspect of its brands and products from concept and design to manufacture and distribution. As one might expect, the figurines command a very loyal fanbase who tend to purchase new releases as soon as they appear.

Another boost for Games Workshop is set to come from its exclusive deal with Amazon, signed last year, to transform its Warhammer 40k game into a film and television series.

In its half-yearly report, released in January, the gaming firm said revenue reached £247m in the 26 weeks to 26 November 2023, up from £226m in the previous year. We believe the business has good pricing and volume growth which, coupled with unending revenue streams, presents a compelling investment opportunity.

IT solutions in the value-added reseller sphere

Bytes, a recent addition to the portfolio, is a value-added reseller of IT services and Microsoft’s top partner in the UK. As Microsoft has gone from strength to strength, so too has Bytes.

The company goes beyond simply reselling products to small- and medium-sized businesses, by seeking to educate on various tech trends and help clients find suitable technology solutions for their businesses.

It has had huge success selling into the public sector, winning big name contracts with the likes of the NHS. Recent artificial intelligence (AI) developments, such as Co Pilot, present a significant growth opportunity as the tool represents a serious productivity opportunity but requires instruction to use it. Bytes will therefore be able to sell it into their customer base at scale.

Callum Abbot is portfolio manager of JPMorgan Claverhouse. The views expressed above should not be taken as investment advice.

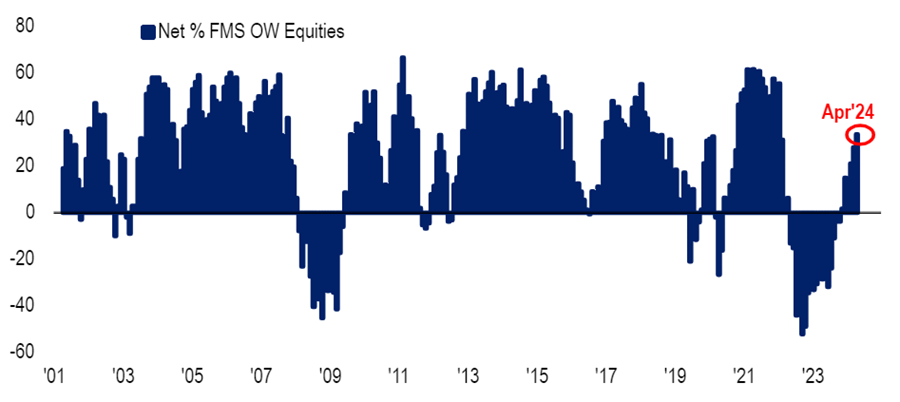

The Bank of America Global Fund Manager Survey reports a significant surge in optimism this month.

Fund managers around the world have become increasingly bullish this month, according to closely watched positioning and sentiment research, with many expecting an economic revival and increased profits.

The findings of the April edition of the Bank of America Global Fund Manager Survey, which polled 224 asset allocators running a combined $638bn, were the “most bullish” since January 2022.

The survey’s broadest measure of fund manager sentiment, which looks at cash levels, equity allocations and economic growth expectations, jumped to 5.8 this month from 4.6.

Percentile rank of fund manager growth expectations, cash level and equity allocation

Source: Bank of America Global Fund Manager Survey, Apr 2024

Fund managers have turned bullish on macroeconomics for the first time since December 2021, with a net 11% expecting a stronger economy over the next 12 months. This is a massive turnaround from last month, when a net 12% of respondents thought the economy would weaken.

Some 78% of managers believe a global recession is unlikely within the next 12 months, which is the highest level since February 2022.

Bank of America analysts added: “While global growth expectations are picking up rapidly (to the highest since September 21), they are still playing ‘catch up’ with equity prices.”

Exactly how this growth will look is more polarising, however.

While ‘stagflation’ (or below-trend growth, above-trend inflation) is still the consensus view at 60%, it has come down from the 92% peak in September 2022.

Expectations for an ‘economic boom’ of above-trend growth and above-trend inflation have jumped to 24%, surging from 12% last month and 5% in January.

Just 9% expect ‘stagnation’ (below-trend growth, below-trend inflation) and only 6% expect ‘goldilocks’ (above-trend growth, below-trend inflation).

Meanwhile, a net 20% of asset allocators think profits will improve over the coming 12 months, which is the highest in three years.

Net % of fund managers overweight equities

Source: Bank of America Global Fund Manager Survey, Apr 2024

Amid this bullish macroeconomic sentiment, fund managers have taken their equity allocation to a 34% overweight, up 6 percentage points on last month and going to the largest overweight since January 2022.

In April, investors are rotating into materials, commodities, energy and industrials while reducing allocations to bonds, cash, staples and emerging markets, the survey found.

Fund managers’ bond allocation has dropped 20 percentage points since the March survey, which is the biggest monthly fall since July 2003. With a net 14% underweight, investors are now the most underweight bonds since November 2022.

The cash allocation fell 14 percentage points month-on-month to a net 9% underweight, which is the biggest underweight since January 2002.

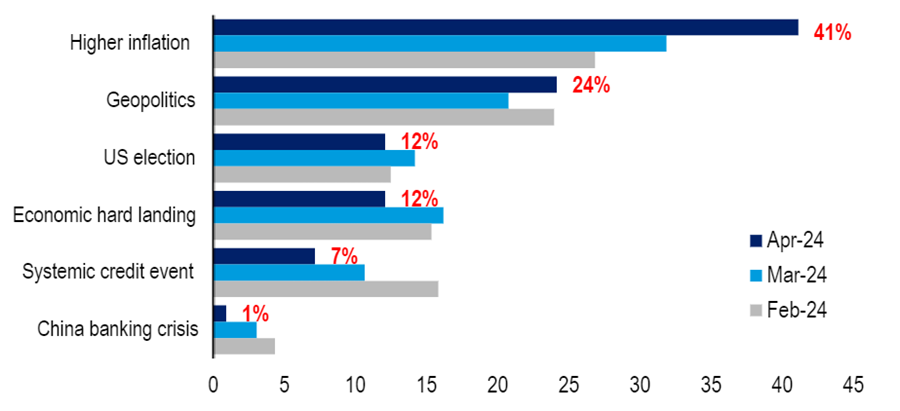

What fund managers consider to be the biggest tail risks

Source: Bank of America Global Fund Manager Survey, Apr 2024

Despite the overall bullish sentiment, there are still some worries keeping managers awake at night.

Some 41% of respondents said higher inflation is currently seen as the largest tail risk, which is higher than the reading last month. Inflation is proving sticker than thought in the US.

Geopolitics is the second tail risk at 24%, reflecting ongoing conflicts in eastern Europe and the Middle East. However, worries around the US election and a hard landing appear to be easing.

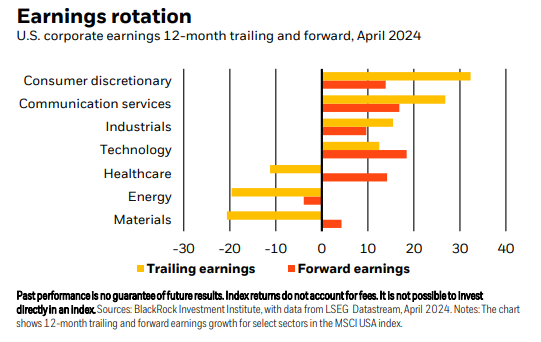

BlackRock expects US earnings growth to broaden out beyond tech and is looking for selective sector opportunities in industrials, commodities, healthcare and energy.

BlackRock went overweight US stocks on a tactical horizon of six to 12 months earlier this year and is sticking to its position despite the market hitting all-time highs.

The asset management giant, which is the largest in the world, is confident that artificial intelligence (AI) advances will continue to bolster returns in the technology sector but believes that gains will broaden out into other sectors such as industrials, commodities, healthcare and energy.

A sector rotation is underway. Although the consumer goods and tech sectors have driven earnings growth for the past 12 months, going forward, consumers are starting to show signs of fatigue as their pandemic savings run dry, while demand is improving in other sectors, the firm said.

Carrie King, chief investment officer of US and developed markets, fundamental equities at BlackRock, said: “Earnings for energy and commodity producers are picking up after a rough two years. We think higher commodity prices can persist and boost both, with the FTSE/CoreCommodity CRB index up 14% this year and near a decade high.

“Prices of metals key to the low-carbon transition, such as copper, have rebounded and could rise further. We see AI advances stoking the buildout of data centres, resulting in major commodity demand. Companies bringing production closer to home can boost industrials.”

Nonetheless, there are risks on the horizon, including tensions in the Middle East and the potential for inflation and interest rates to stay higher for longer. Against that backdrop, BlackRock views energy stocks as a potential portfolio buffer against geopolitical risk.

“The March acceleration in core services inflation, excluding housing, suggests overall core inflation could rise again sooner than we had expected. The tensions in the Middle East look contained for now but we see risks of further escalation. We could face elevated oil and commodity prices for longer, reinforcing the new regime of higher inflation – and our long-held view that we are in a higher-for-longer interest rate environment,” King warned.

“The question for stocks: will economic and earnings growth stay strong enough to offset that inflation and policy rate outlook?”

So far, solid job gains have supported US economic growth, helping companies to maintain profit margins. “We think market sentiment can stay upbeat if falling goods prices keep dragging down inflation – allowing the Federal Reserve to deliver one or two rate cuts,” King said.

“Nonetheless, after such strong recent performance, the onus will be on US companies to meet already-high expectations this earnings season.”

Analysts are forecasting 2024 earnings growth of 11%, which is well above the 7% historical average, according to data from LSEG.

Felix Wintle, manager of the VT Tyndall North American fund, agrees with BlackRock that stock market leadership is spreading to other sectors. Since the market rally began at the start of November, “mid-caps are working, small-caps are working, there’s been a broadening out of participation,” he said. “We’re actually really bullish.”

This is in stark contrast to last year when “everyone wanted to play defence” but “your traditional defensive sectors were a no go” because utilities, real estate investment trusts and pharmaceuticals were all hit hard by successive rate hikes.

“People just piled into Apple and Microsoft [thinking] ‘I know these stocks aren’t going to blow me up’,” Wintle said. In his 20-year investment career, he doesn’t remember a market being that narrow.

To find the next stock market leaders, Wintle is leaning into the themes of US federal spending on infrastructure, reshoring the semiconductor industry and building out data centres – trends that BlackRock is also monitoring closely.

The VT Tyndall North American fund’s biggest winner this year is Super Micro Computer; it provides the hardware to retrofit and upgrade servers to make them compatible with AI, which uses more computer power than traditional data centres can handle. Since Wintle bought the stock in January it has risen 300% so he is trimming the position.