The opportunity in the UK is so great these mangers put on gearing for the first time since 2011.

People keep talking about when the UK market is going to turn, but very few realise it probably already has. There have been signs particularly in the small-cap arena, as the asset class has silently climbed up the 2024 performance table and leapfrogged to the very top earlier this month.

Jonathan Brown and Robin West, managers of the £146m Invesco Perpetual UK Smaller Companies trust, have been patiently watching this trend since the autumn of last year, when they started to crank up the gearing on the trust from 0%, where it has been since 2011, all the way to the current 5%.

Their decision to take up more debt and increase the exposure to the market was based on a combination of favourable conditions measured through multiple lenses, including valuations, momentum and earnings momentum, economic outlook and geopolitics.

“Valuations had looked attractive for a long time and we felt inflation was about to peak. Then, we started to see the beginnings of takeover activity, so we put on 1% to 2% and waited to see how the market would fare,” West said.

“Our confidence has increased since then and we’re now geared between 5% and 6%.”

The pickup in market momentum over the past quarter has been a reason for the increase in optimism, but the most convincing parameter for the managers was valuations.

“We looked at the valuations of smaller companies in the past 30 years. When they traded on similarly low multiples as they do today, the average return was 19% over the next 12 months and 36% over the next two years,” West continued.

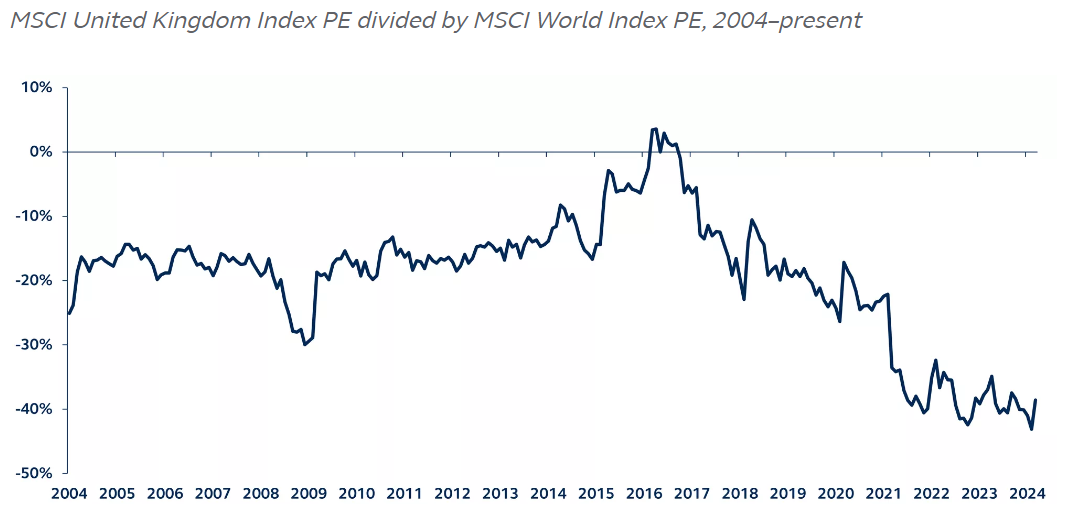

On top of that, the UK is one of the biggest underweights globally and is “definitely on sale” at the moment, with the MSCI UK index more than 30% cheaper than the MSCI World index, as the chart below illustrates.

UK price/earnings relative to the world

Source: Factset, MSCI, Principal Asset Management. Data as of December 31, 2023.

This value is not only clear to the managers but also to private equity and corporates, which have been snapping up bargain after bargain in the UK. It is also apparent to other investors too, they noted.

“At the end of March 2024 for the first time in the past two years, the institutional trading system at Merrill Lynch went from showing the UK as a net sell to having net buyers,” West said.

“That's a reason why we think the discount that the UK is trading at will close, and that was one of the key factors behind our decision to introduce gearing.”

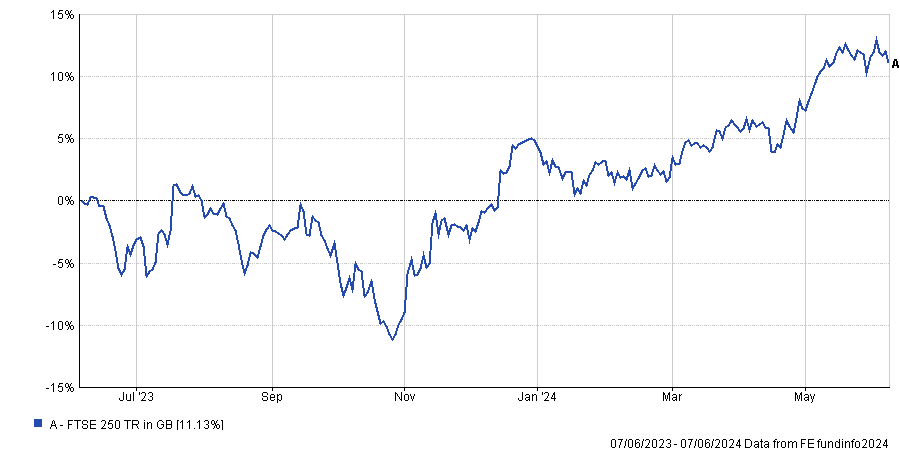

To those that aren’t convinced the market has already turned, Brown suggested looking at the performance of the FTSE 250 index.

Performance of index over 1yr

Source: FE Analytics

It bottomed at the end of October last year, but has recovered over 25% since then.

“It's not a question of when the market is going to turn, it's already turned thanks to better sentiment about inflation and interest rates, the cheapness of the UK and takeover bids, whose cash gets reinvested back into the market as well,” he said.

“With the economic situation further improving and the future interest rate cuts, we can see a push even further. That's not well understood by investors. After a period of being in the doldrums, the market has had a very strong six or seven months, and for where valuations are, it's got a very long way to run still.”

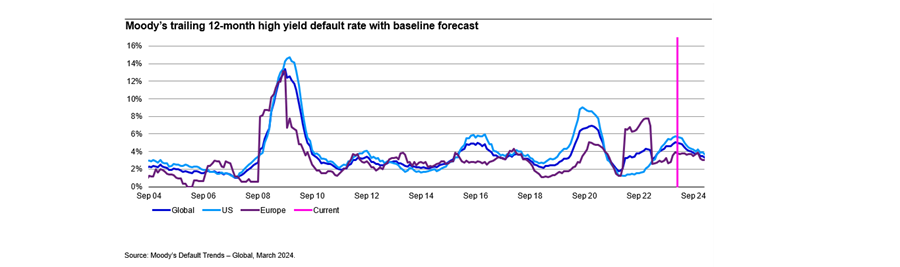

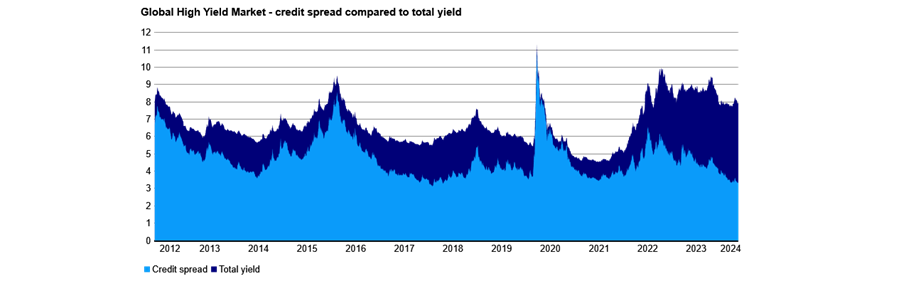

A company having to pay more to its creditors is not necessarily a bad thing, especially if you’re the creditor.

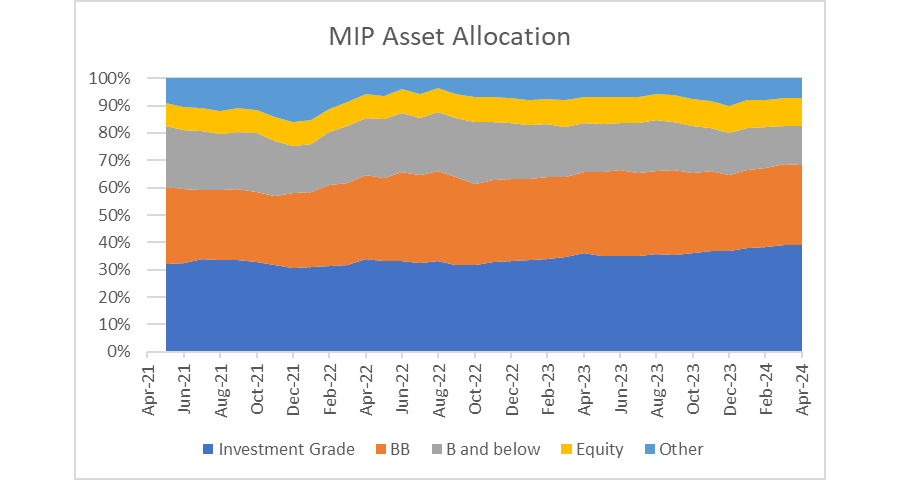

Our fund’s exposure to bonds rated B and below has rarely been lower. This part of the market is a natural hunting ground for us, given its explicit mandate to deliver high income. Yields remain higher here than in BB and above. So, why steer away from it?

There are two sides to this. One is the presence of attractive alternatives, both in outright yields and on a risk-to-reward basis. With the rise in interest rates, yields on higher quality bonds, in BB and investment grade, have been good. There is no need to chase income.

The flip-side of this positive is a concern that the yields offered on assets in the lower part of the credit quality spectrum do not justify the risks.

Source: Invesco

Competing forces - growth versus re-financing risk

As shown in the chart above, our exposure to lower quality bonds has continued to fall in the past couple of quarters, despite this market segment being bolstered by improved growth data and rising hope of a soft economic landing. High yield bonds have outperformed investment grade.

Source: Invesco

Growth is good for high yield. High yield companies tend to be more indebted and so have higher debt-servicing costs relative to their earnings. This means they are more sensitive to changes in earnings. As an asset class, high yield is more correlated with equities than more rate-sensitive investment grade and government bonds.

With earnings holding up well across the corporate sector, commonly followed metrics for high yield, such as the ratio of debt to EBITDA and interest coverage, are looking healthy. Default rates and default expectations have also remained within the normal range.

Source: Invesco

My reason for concern about lower-quality credit is not that I see an immediate risk of an earnings recession. It is to do with re-financing risk.

For several years before 2022, ultra-low interest rates enabled bond issuers to finance very cheaply, with historically low coupons.

Source: Invesco

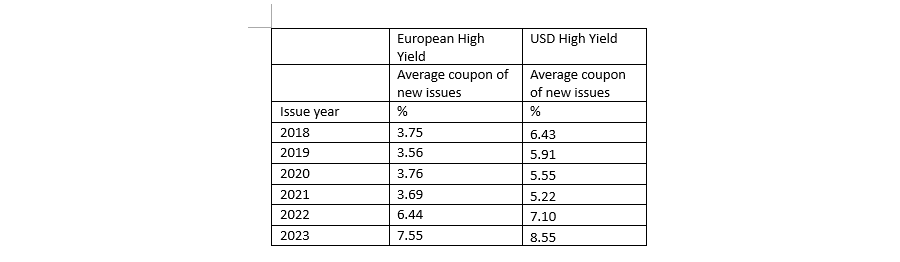

This changed in 2022. Higher interest rates meant the high yield bond market had to adjust to remain competitive. The price of these low coupon bonds fell below par and the coupons on new bonds began to rise.

New bonds have to offer a yield that is competitive with the secondary market. At current market yields, that means coupons on new bonds, issued at par, will have to be substantially higher.

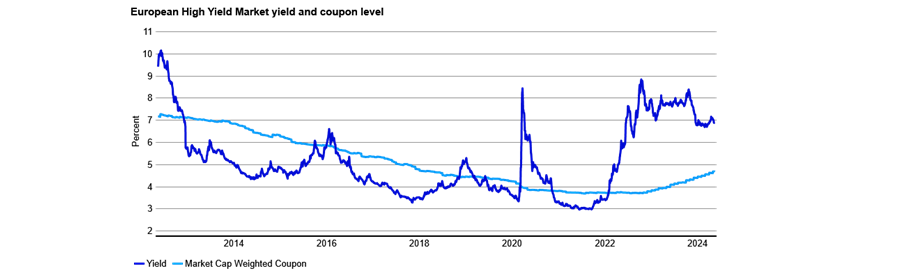

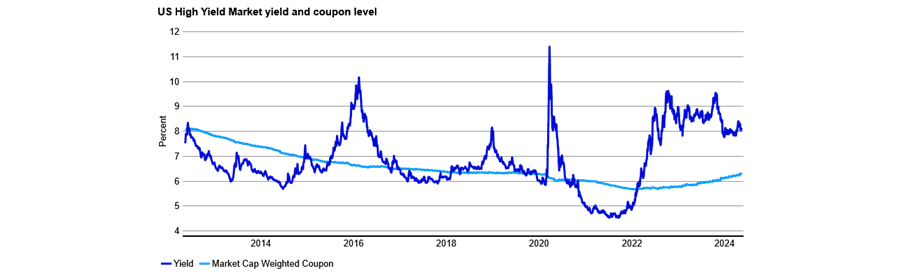

The charts below compare the weighted average coupon of high yield bonds with the market yield. In both the European and the dollar markets, coupons are substantially below the yield. Unless the yield drops, issuers will have to pay more coupon to close this gap.

Source: Invesco

Source: Invesco

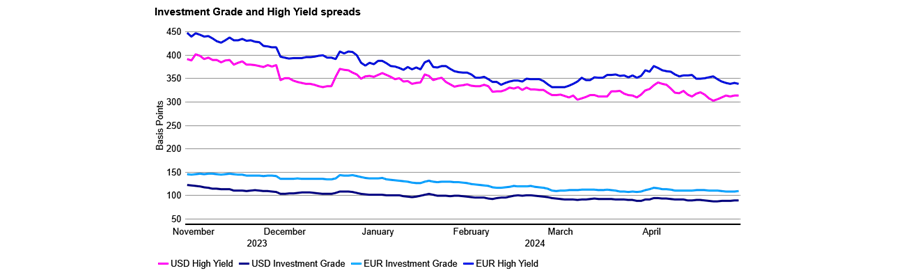

Spreads are not unusually high. In fact, they are well below average. As the chart below reminds us, the dominant driver of today’s higher yields are interest rates.

Source: Invesco

While interest rates remain high, high yield issuers face a re-financing challenge. According to Bank of America research, 25% of the US high yield market will be free cash flow negative if they have to carry out the next two years of re-financing at current rate expectations. In other words, these companies’ balance sheets don’t work unless the Federal Reserve cuts more than is currently priced.

Taking a step back, this environment is a little counterintuitive. Better growth conditions pose a threat to the high yield market. Higher earnings will increase the ability of corporates to service their existing debt, but if interest rate expectations stay high (in part because of better growth), then many will struggle with re-financing.

What this means for my portfolio

Monthly Income Plus is built on fundamental credit research and bond selection. I am wary of the re-financing risk faced by high yield and I have reduced exposure to that part of the market. But that doesn't mean I will avoid it altogether.

These risks may offer opportunities at the individual company level. High yield companies, as a whole, will have to pay more interest. Some companies will struggle in this environment.

I will be aiming to avoid them through careful credit assessment. But others will be able to manage. That a company has to pay more to its creditors is not necessarily a bad thing, especially if you’re the creditor.

We have already seen good companies coming to the market and paying coupons several percentage points higher than when they borrowed a few years ago. We’ve been happy to invest and to take those coupons.

Rhys Davies, manager of Invesco's Monthly Income Plus fund. The views expressed above should not be taken as investment advice.

The world’s largest asset manager looks at the election landscape for the remainder of the year.

More than half of the world’s population will head to the polls in 2024 with the US and UK among numerous countries with potential political upheaval in the remainder of the year.

It is a tricky period for politicians, according to Jean Boivin, head of the BlackRock Investment Institute, who said voters are “expressing frustration” with the ongoing rising cost of living around the world. Yet a change in government may not be the catch-all solution, he warned.

“We see many incumbent leaders or challengers constrained in any response, notably due to high public debt somewhat tying their hands,” he said.

Taking the US as an example, Boivin noted both incumbent president Joe Biden and former president Donald Trump – who will do battle once again in the upcoming election – swelled fiscal deficits to stimulate growth during the Covid pandemic, leaving them somewhat hamstrung.

“No matter who wins, deficits are set to remain historically large. Neither is charting a path to a sustained reduction in deficits,” he said.

In fact, both presidents could increase inflation through their measures. Trump has proposed a 10% levy across-the-board tariff for imports and a 60% tariff on Chinese goods, while Biden is expected to keep his current protectionist policies, like higher tariffs for some sectors, industrial policies favouring domestic production and the use of export controls.

Meanwhile, changes to immigration would have implications for inflation as the US faces a shrinking working-age population, said Boivin.

“On energy policy, the Inflation Reduction Act (IRA) and its low-carbon transition investment incentives are in focus. If Republicans control Congress, they may revise or repeal parts of the IRA to fund tax cuts.”

It is for this reason he believes the Federal Reserve will need to keep rates high for longer, as increased deficits should lead to persistent inflation.

“We think that, and markets needing to absorb large bond issuance, will spur investors to demand more term premium, or compensation for the risk of holding long-term US bonds,” he said.

However, the firm is bullish on the US equity market, maintaining its overweight position, although Boivin added that he will “eye the key policy areas of the presidential election”.

“US stocks notched fresh highs last week and are up nearly 13% this year,” said Boivin, although all eyes are currently on whether the Federal Reserve will cut rates in the near future.

“We expect key data – like last week’s US payrolls and this week’s US CPI – to drive Fed decision-making. Even with easing likely on the horizon for the Fed and already underway elsewhere, this is not your typical rate-cutting cycle, in our view.

“The red-hot US payroll data reinforces what an unusual environment this is for the start of a global easing cycle. We don’t see central banks cutting far and fast.”

Away from the US, the Indian election threw up a moderate surprise. Although prime minister Narendra Modi secured a third term, he had to enlist help through a coalition after failing to win a majority.

“That could slow some reforms – but it doesn’t change the long-term benefits from the confluence of mega forces, like a young population and digitalising economy,” said Boivin.

In Europe, despite the resurgence of right-wing parties in recent years centrist parties are still expected to keep control of the European Parliament, although he questioned whether certain governing parties could struggle, such as French president Emmanuel Macron who called a snap election in France after his party suffered a big loss.

In the UK meanwhile, a decisive victory for one party could “create the political breathing space to address the UK’s structural issues, such as weak productivity growth”, said Boivin.

“Beyond potential policy changes, a July election could allow the Bank of England to start cutting rates once it’s over – a reason why we like UK bonds. On a strategic horizon of five years and longer, we like government bonds in the euro area and UK on expectations for lower interest rates.”

This reader has several pension pots from former employers and is wondering how to amalgamate them.

Making a career switch is a brave thing to do, especially if taking the plunge and becoming self-employed. There are a litany of things to think about but your pension is probably not one of the first things that comes to mind.

After an office-based career spanning two decades, Louise decided to change direction in her forties and retrain as a yoga teacher, but having made the switch she is now wondering how best to save for her retirement given her relatively-new self-employed status.

She is already ahead of the curve in planning for her future, given that only 20% of self-employed people are saving into a pension plan, according to Hargreaves Lansdown. Furthermore, Louise is fortunate enough to have a final salary pension fund, having previously worked in the public sector, as well as a defined contribution pension fund from her previous full-time private sector job.

She now supplements her teaching income with short-term corporate contracts and these part-time jobs come with pension payments. This has left Louise with several different pension pots and she is considering how best to amalgamate and manage them.

How much should Louise save into her pension?

Lena Patel, a director and chartered financial planner at ISJ Independent Financial Planning, suggested that Louise start by considering what income she needs in retirement, what kind of lifestyle she wishes to lead, and when she intends to retire.

She might prefer to have a phased retirement, continuing to work part-time to supplement her income, Patel added.

Rob Morgan, chief investment analyst at Charles Stanley, suggested one way of doing this is to use an online pensions calculator to help decide how much to save and to see how increasing or decreasing contributions would impact the overall pot.

The calculator will work out what level of retirement income Louise has already accumulated in her existing pension funds and state pension, and how much more she needs to save to meet her goals, he explained.

To give some context around what sort of annual income Louise might need in retirement, the Pensions and Lifetimes Savings Association (PLSA) states that a single person would need £14,400 for a minimum standard of living and £31,300 annually for a moderate lifestyle, including owning a car and having a fortnight’s holiday abroad each year. The full state pension of £11,500 for 2024-25 goes some way towards this.

As a recently qualified yoga teacher, Louise is still building up her business, so can only afford to put a small amount aside each month to save for her retirement, but she anticipates that her monthly contributions will grow over time.

With that in mind, Patel recommended considering other savings vehicles such as ISAs to give Louise the flexibility to access her savings in case of an emergency. ISAs do not have the same tax benefits as pension funds but that is less meaningful for very small amounts and liquidity might be more important, she noted.

Morgan countered that the tax relief on contributions makes pensions an attractive way to save. “For basic-rate taxpayers, the government adds 20% to whatever you contribute. If you’re a higher-rate taxpayer, you can claim up to an additional 20% through a tax return,” he said.

“In addition, you’ll benefit from tax free returns while the pension fund invested, only paying tax when you take money out. Currently the first 25% is tax free up to a certain limit.”

What’s the best way to consolidate various pension pots?

Experts recommended that Louise consolidate her defined contribution pension pots from various employers into one place to make it easier to manage them and ensure nothing gets lost. They agreed that she should keep her final salary pension untouched, however.

Morgan said: “The transfer starts with an application process to the provider you want to transfer to, and they do the legwork for you from there.”

Helen Morrissey, head of retirement analysis at Hargreaves Lansdown, advised that “before consolidating, it is important to make sure you aren’t losing any important benefits such as guaranteed annuity rates or landing yourself with high exit penalties”.

The next question is where to pool Louise’s retirement savings. Patel said the simplest solution might involve moving everything into one of the workplace pension schemes that Louise already has, although she should check that the risk profile and investment strategy of the scheme are suitable. Morgan said she might consider consolidating into the best value plan.

Another option would be opening a self-invested personal pension (SIPP). SIPPs give people control over how their retirement savings are invested, but they may only suit people who want to proactively take investment decisions and who have the time and inclination to do their own research.

Louise does not have any prior investment experience and she is looking for some guidance. Therefore, a ready-made fund solution, either within a SIPP or another type of personal pension, might be more suitable, Morgan said.

Morrissey added: “In terms of choosing where you are going to consolidate your pension then it’s important to consider factors such as cost, investment choice, service and support. SIPP/pension providers will offer fund options aimed at those who are unsure about where to invest.

“Ongoing support is hugely important in terms of helping people build confidence in managing their pensions. Some providers will offer webinars, articles, research and even access to financial advice if required.”

How should the pension portfolio be invested?

Patel recommended a high allocation to equities to maximise returns, given that Louise has at least a decade to ride out stock market volatility. She is in her mid-to-late forties and would not be able to access her pension until the age of 57.

Morgan concurred: “My suggestion here is not to be too risk averse. Maximising exposure to equity markets should build wealth better than other lower risk areas, albeit at the expense of greater shorter-term ups and downs. Given the long time horizon until retirement age and continued regular contributions, it’s worth embracing that."

Morgan also suggested delegating asset allocation decisions to a multi-asset fund that covers all the major markets and regularly rebalances.

If you would like your financial situation reviewed by experts, please get in contact with the Trustnet team. You can reach us by emailing editorial@fefundinfo.com.

The Fidelity China Special Situations manager explains the country’s regulatory and macroeconomic outlook.

The ongoing battle for technological innovation between the US heavyweights and their Chinese counterparts is something that will go on for decades, according to Fidelity China Special Situations manager Dale Nicholls.

There have been myriad concerns over the trade war between America and China, causing the manager to work with Fidelity International’s legal and regulatory team to understand potential policies that could come into place.

“In general, we believe that China would be keen to have better relations with the US, and the greater dialogue between presidents Xi Jing Ping and Joe Biden is encouraging,” he said in the trust’s full-year financial results.

“There is no denying, however, that strategic competition between the two countries is going to be a factor that will be with us for decades.”

Mike Balfour, chairman of Fidelity China Special Situations, added this was the major risk to the board’s “cautiously positive outlook” on the country.

“US relations with China have stabilised somewhat, although increasing tariffs and trade restrictions remain a concern. There is a significant risk that relations could worsen and the US may implement measures such as raising tariffs on imports from China to 60%, which would significantly harm Chinese exporters, depress global trade and exacerbate US inflation trends,” he said.

This increase to 60% has been mooted by former president Donal Trump, who is contending to be re-elected later this year, although Nicholls noted that sticky inflation could make this a difficult policy to achieve.

Even if there are further trade sanctions on the way, the country has been “dealing with US tariffs for years” and companies are “well aware of the prospect that they might be higher in the future”.

Despite the potential trade tariff headwind, both the manager and the chairman were “cautiously optimistic” on the outlook for the world’s second largest economy.

For example, Balfour highlighted a strong March reading of the purchasing managers index (PMI) – a measure of the economic health of the manufacturing sector. It moved into positive territory for the first time in six months and was the highest it has been in a year.

Nicholls added consumer confidence could be picking up, having been weak for some time, with deposit growth – the amount people are putting away into savings – slowing, suggesting they are spending more.

“Bank deposits saw huge growth during Covid and household balance sheets are very strong, so there is spending power available, but people need confidence to unlock it,” he said.

Although China’s economy is forecast to slow from its current growth rate of around 5%, Nicholls added that it is expected to remain one of the fastest growing major economies in the world.

“Its gradual shift towards consumption-driven growth, fuelled by an expanding middle class, rising incomes and technological innovation, provides a solid backdrop for companies to thrive,” he said.

At a market level, he noted valuations are at “particularly low levels” and there should be “many opportunities for investors to participate profitably in the recovery”.

These views came in the trust’s full-year report in which it made a total loss of 16.3% for the financial year ended 31 March 2024. This was slightly ahead of the MSCI China Index’s 18.8% fall.

Consumer discretionary stocks were a big relative winner, with four of the firm’s top 10 best performers coming from the sector, including Hisense Home Appliances Group.

“While the ‘white collar’ area of the consumer market has had a tougher time, the lower end has been much more resilient, supported by government stimulus in the case of home appliances,” said Nicholls.

Industrials such as logistics firm Sinotrans also helped the portfolio to beat the benchmark over the past 12 months.

Energy stocks, which make up 2% of the trust, were the biggest gainers in absolute terms, while laggards came from financials and materials, where the trust is overweight, as well as its 3% holdings in the property sector.

He also commented on the trust’s gearing position, which peaked at 25.5% in August last year. “Gearing will naturally be higher when that opportunity set is plentiful and vice versa. Given the significant swings in sentiment towards the China market, we tend to see better risk-reward prospects when sentiment is weak and valuations are lower,” said Nicholls.

Currently it stands at 20.8%, which he noted was “a notable increase since late 2021” and reflects the “compellingly attractive valuations of the Chinese market”.

It was a detractor to performance last year, however, contributing a loss of 3.75 percentage points over the 12 months to March 2024.

Interest rate hikes and China’s downturn have bitten into returns during the past few years.

Edinburgh-based Baillie Gifford has had a torrid time of late, with just one portfolio among its 46 funds and investment trusts making a top-quartile return in their respective sectors over the past three years.

The Schiehallion Fund was the only one to achieve the feat, despite making a 47.5% loss; most trusts in the IT Growth Capital sector plummeted even further.

Only two further portfolios beat their sectors, with the open-ended Baillie Gifford Responsible Global Equity Income fund and Baillie Gifford China Growth Trust making above-average returns in the IA Global Equity Income and IT China/Greater China sectors respectively. The latter, however, only has three constituents.

As a result, managers at the firm have admitted that mistakes were made over the past three years. Below they highlight key areas that have impacted performance.

Inflation and interest rates

One of the biggest impacts on Baillie Gifford’s growth-oriented suite of funds has been interest rates, which have rocketed in recent years to combat significantly higher than expected inflation.

Chris Davies, co-manager of the Baillie Gifford European Growth Trust, said this was a particularly big factor in Europe where inflation numbers hit double digits in some countries.

“If you go back to 2022, we went into that year with a portfolio that was probably set up to do much better in an environment where rates remained low. That was something we have been open about and was a mistake. We could have been more front-footed about that,” he said.

“There was some endemic inflation in the system anyway coming out of the pandemic but when Russia invaded Ukraine suddenly it just took off and, with that, interest rates moved up quickly, as did discount rates.”

Performance of trust vs sector over 3yrs

Source: FE Analytics

The trust’s overweight to mid- and small-caps, which today make up around 40% of the portfolio, got “whacked” and “hammered” during 2022, he admitted.

Lawrence Burns, deputy manager of the Scottish Mortgage Investment Trust, said if he had “more of an inkling” on the interest rate headwinds the trust faced, he would have made moves “at the margin” to limit losses, but the portfolio would still look broadly similar to today.

“We are investors in long-term growth companies. They are always going to come under pressure if there is a material rise in interest rates. But as we went through that period, we were quite clear that what we thought mattered in the long run was (more than interest rates) does the business work and succeed,” he said.

Burns admitted there were some factors the team could have looked at more, such as companies with greater capital requirements or more debt, noting they could have been “more attuned” and “a bit more alert” that the macro environment was changing.

Performance of trust vs sector over 3yrs

Source: FE Analytics

China

Another area that hampered Scottish Mortgage’s returns was China, with the market taking a battering over the past few years on the back on geopolitical concerns. The MSCI China index, for example, is down 34.8% over the past three years.

“If we’d incorporated some of the geopolitical tensions and the change in the domestic regulatory environment that was largely kicked off around the ANT attempted IPO, we probably would have [implemented] a higher bar for Chinese holdings sooner,” said Burns.

Since then, the trust has reduced its Chinese equity exposure to 10% from 25%, although the deputy manager noted that he is still “very happy to own companies in China”.

Stock selection

For Baillie Gifford Positive Change, two factors (as well as those mentioned above) have hit returns. The first is an underweight to the Magnificent Seven.

Rosie Rankin, investment specialist on the fund, said: “What has been particularly unhelpful for the relative performance of Positive Change over the past six to 12 months has been the incredible performance we have seen from a very concentrated number of stocks – the Magnificent Seven – to which we have a very low exposure indeed.”

Performance of fund vs sector over 3yrs

Source: FE Analytics

Another is the “execution risk”, she added, with some companies failing to match the ambition of their management teams.

Instead, the managers have “learned lessons” from the past few years particularly around risk and the “financial resilience” of stocks within the portfolio.

“We have a broad range of companies from steady growth compounding stocks like Deere with a long track record but then new innovative companies too. We want that balance,” she said.

Future headwinds

Lastly, Burns said he and lead manager Tom Slater have been looking ahead for potential headwinds and highlighted artificial intelligence (AI) as one area where investors can expect to see some volatility.

“There will be future headwinds. It will not be plain sailing for us for the next 20 years. At some point there may be an air pocket in AI demand. There has been a huge investment in AI hardware but whether that matches with demand as people work out how to use them at scale [remains to be seen],” the Scottish Mortgage manager said.

“Others include geopolitical tensions and what that means around the world. We have considered new potential holdings [and asked] what do we want in a more volatile world? Ultimately we are trying to own and back companies that are best placed to navigate that future.”

This US equity manager debunks a myth about investing in technology and resources.

When James Watt invented the steam engine, people marvelled at its efficiency, but as they used the new technology, they started to fear they would run out of coal.

British economist Stanley Jevons kept a cool head and predicted in his 1865 book, ‘The Question on Coal’, that increased efficiency would drive greater use of the technology and that far more deposits of coal would be found. History proved him right.

Economists call this the Jevons paradox, which happens when better efficiency leads to increased demand and a higher rate of resource use, contrary to mainstream expectations.

Applying this paradox to today’s markets can give investors an edge in recognising areas that are set to flourish, according to Cole Smead, manager of Smead US Value UCITS.

“There's the myth in our cultures that technology will cause us to do more by depriving ourselves. Technology makes us more efficient, but the Jevons paradox continues to play out,” he said.

“I hear time and time again people saying that technology will make our use of energy so much more efficient and therefore we're going to use less energy. The Jevons paradox says that's impossible, and it's also never happened historically.”

An example is gasoline demand, which has never been bigger in the United States, and the same goes for the number of miles driven.

Similarly, people thought the LED light bulb would save energy but instead, we quadrupled the number of light bulbs in our houses and energy demand continued to go up.

“It's a perfect picture of the Jevons paradox. You did not see a decline in consumption like people would have thought,” he observed.

How the Jevons paradox translates to investing

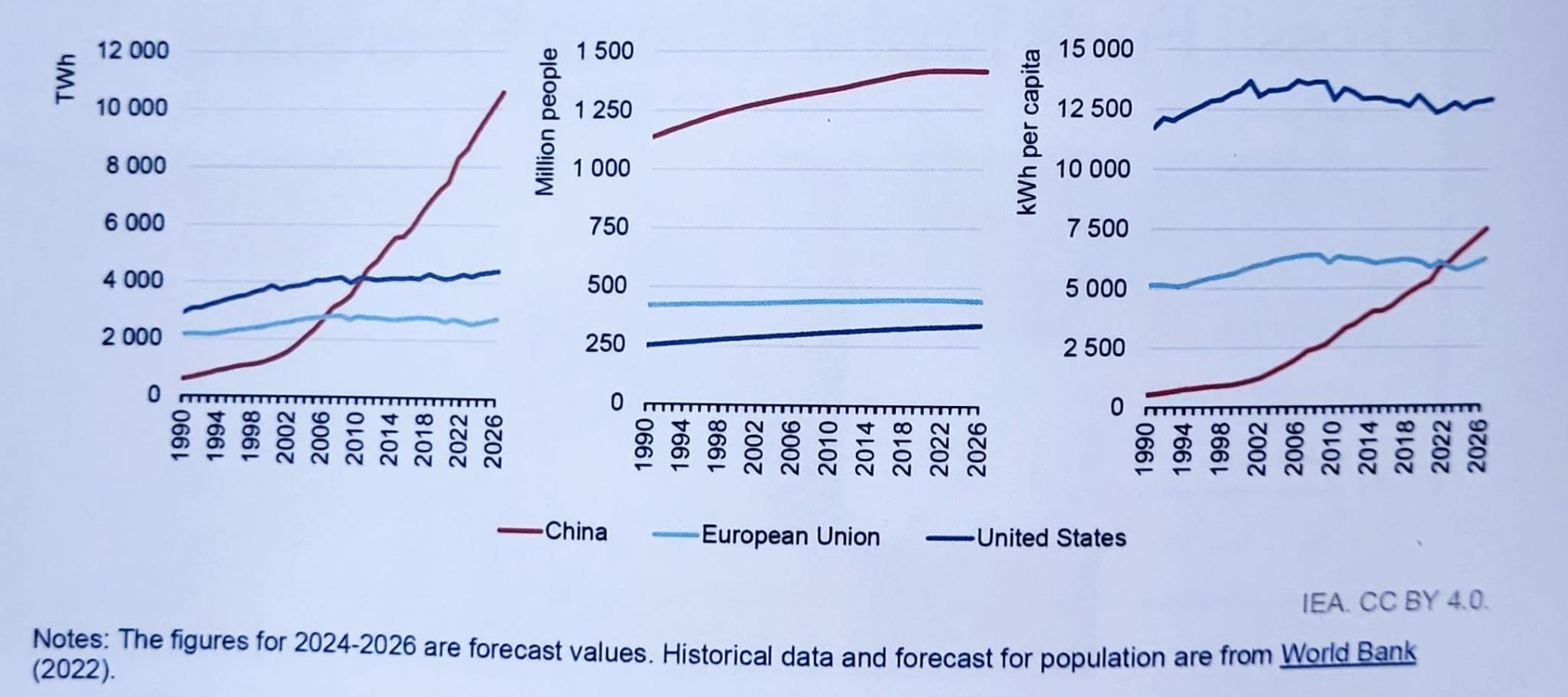

There is one area where demand is accelerating but supply is being cut, making it a great investment opportunity, according to Smead. That area is electricity production – in particular through fossil fuels.

Total electricity demand (left), population (centre) and electricity consumption per capita (right)

Source: Smead Capital Management, International Energy Agency

“Technology causes us to do way greater things and become more efficient. But more efficient doesn’t mean that demand is going down, in fact the curve of electricity use is ever growing,” the manager said.

“And while natural gas has sucked up a bigger share of the total growth, we have slowly been moving away from coal, but move is not relevant whatsoever.”

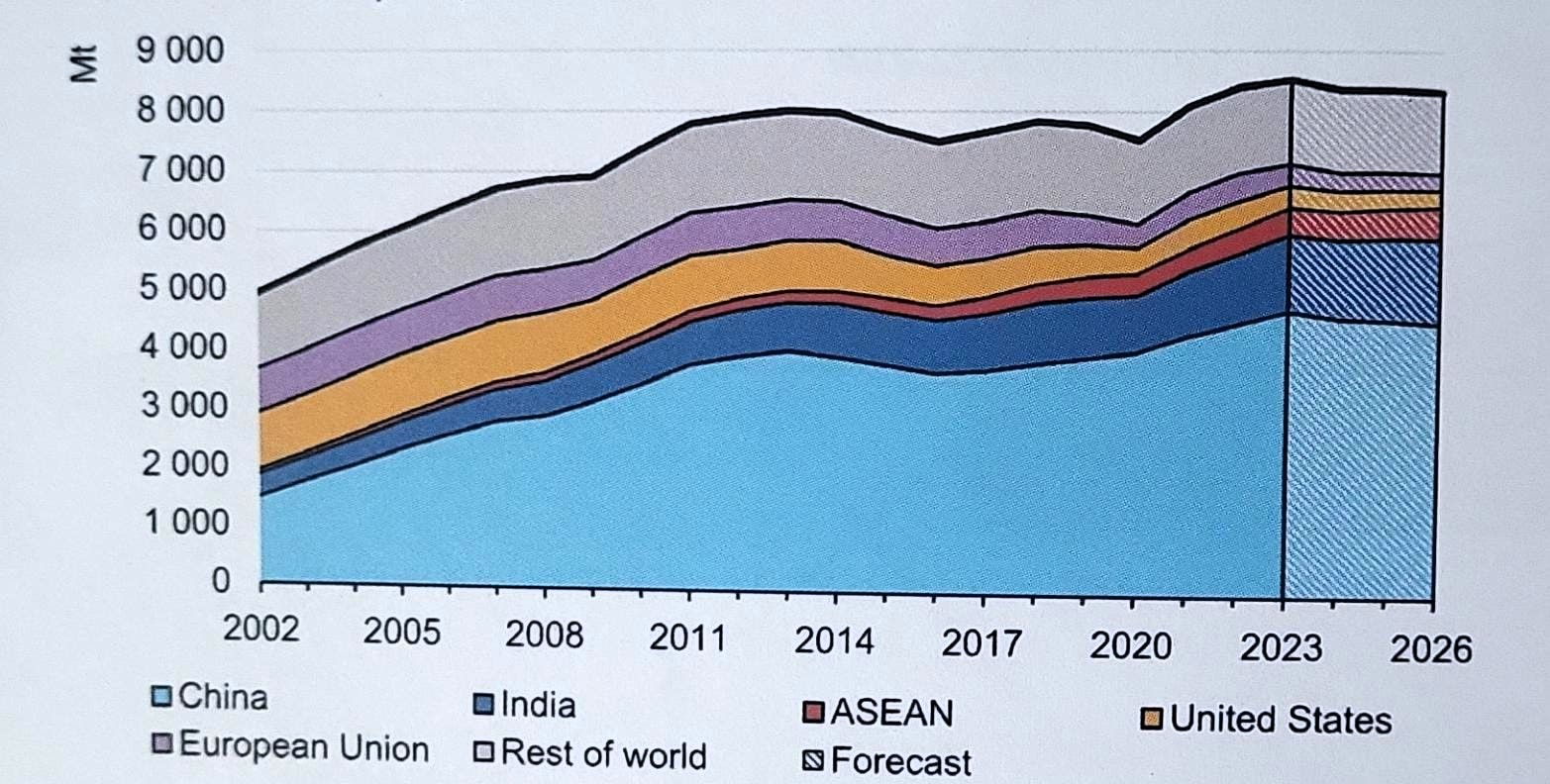

To illustrate this point, he showed the chart below.

Global coal consumption, 2002-2026

Source: Smead Capital Management, International Energy Agency

“About 13 years ago, the International Energy Agency predicted the world was at peak coal usage. So far, it’s 13 years off and growing. These organisations are wicked smart, but they can be very wrong,” he said.

“If you ever get into a world where supply is dwindling and demand picks up, you can make some fabulous money.”

The manager highlighted three stocks that he believes are poised to benefit from this supply/demand discrepancy.

The first is South African coal exporter Thungela – admittedly a cyclical business that has had periods of underperformance, but it comes with “a nice little buffer”, as 60% of the stock is in net cash.

This means firstly that the company would need to burn a lot of cash before investors make a loss, and secondly, that it can buy back its own shares. The impact of buybacks on return on equity (ROE) is “one of the most underappreciated ideas in the stock market”, Smead added.

If half of Thungela’s cash was used to finance share repurchases, its adjusted ROE could grow by 30%, he calculated.

Finally, the market is overlooking pure play Canadian oil sands producer Meg Energy and US oil company Ovintinv, Smead said. Jevson’s paradox is at play again, with capital expenditure on oil declining in the western world, shrinking supply for industry, butat the same time, demand is increasing.

REITs have historically been fertile ground for active managers.

Index investing reached a milestone in early 2024, with assets in passive investment vehicles surpassing those in actively managed strategies for the first time. On the surface, the appeal of index investing is compelling: passive exchange-traded funds (ETFs) offer lower costs.

And, in the case of broad-based equity and bond categories, active managers frequently fail to consistently outperform their benchmarks. But cheaper is not always better, and not all markets are alike.

Real estate is one area of the equity market that lends itself to active management. REIT managers who commit time and resources to understanding current property fundamentals, shifting market trends and factors that may affect listed equity performance can potentially spot pricing inefficiencies and rapidly implement plans to generate excess returns.

We believe this advantage is reflected in the performance of the largest active REIT mutual funds relative to passive investment vehicles, despite active funds typically having greater expense ratios.

The modern REIT market offers a diverse opportunity set

When investors think of commercial real estate, they may envision office buildings, malls, shopping centres and apartments.

REIT ownership of these kinds of assets exists, of course. However, REITs have become increasingly specialized in new property types since 2000, shifting the REIT market’s composition away from traditional sectors.

For well-resourced managers, these new sectors provide a broad selection of REIT-owned assets for constructing portfolios, many of which have secular growth drivers.

These include data centres, where companies rent by the kilowatt to connect cloud servers; cell towers that lease space to wireless carriers for 5G networks; high-tech distribution hubs that facilitate next-day shipping on e-commerce orders; climate-controlled food storage facilities; biotech research labs; and senior living centres, just to name a few.

Capitalising on distinct sector characteristics

REIT sectors and companies tend to respond to market conditions very differently depending on factors such as lease durations, types of tenants, economic drivers and supply cycles. These differences have historically resulted in wide dispersion of sector returns in any given period.

More economically sensitive sectors with short lease terms, such as hotels and self-storage, can adjust rents relatively quickly to capture accelerating demand in a cyclical upswing.

By contrast, longer-lease sectors such as net lease and health care have more defensive cash flows that may be more resilient during economic downturns. In 2023, returns between the best and worst sectors were separated by 38 percentage points. In other years, the dispersion has been considerably greater.

We have observed that the difference in returns at the security level within each sector is often similar to the variance at the sector level. We believe this dispersion highlights the opportunities active managers have to enhance returns through both sector and stock selection.

Navigating secular growth opportunities and challenges

As economic cycles progress, property types are likely to have different fundamentals. For instance, the pandemic upended retail, hotels and offices, but benefited technology-related REITs amid acceleration in e-commerce and working from home.

And many sectors and cities continue to feel the lasting effects of the pandemic as flexible work-from-home policies have changed how and where people want to work and live, creating an uncertain outlook for offices.

Consequently, high-quality offices may continue to see healthy demand, while lower-quality assets may experience soft demand for years to come – a distinction not likely to be reflected in passive portfolios.

Active managers can also add value by capitalising on regional differences and trends. Many US residents are moving from dense, high-cost northern and coastal cities to lower-cost markets in the sunbelt.

In global portfolios, REIT managers may assess geographic regions to understand local property supply and demand fundamentals, economic trends, monetary policy and other factors that may affect the operating performance of different real estate companies, as well as the markets valuation relative to other regions.

Anticipating secular trends such as these is a key component of active management since they can present opportunities for active managers to capitalize on diverging fundamentals. For example, the divergence in industrial and office properties.

By contrast, passive portfolios are, by design, not able to allocate assets to capitalise on potential secular growth opportunities, nor can they sidestep sectors that may be facing long-term headwinds. Of course, there is no guarantee that active management can successfully navigate these trends.

REIT managers may also invest based on relative value, seeking to allocate portfolio assets based on merit rather than market capitalization, as is often the approach for many passive index funds.

Investing outside the benchmark – participating in special opportunities such as recapitalizations, private placements, initial public offerings (IPOs) or pre-IPO investments – is another way for active managers to add value.

These activities are not within the scope of passive index-tracking strategies – a notable disadvantage in recent years due to the inability of passive vehicles to get out of the way of the secular declines in retail and offices.

Jason Yablon is head of listed real estate at Cohen & Steers. The views expressed above should not be taken as investment advice.

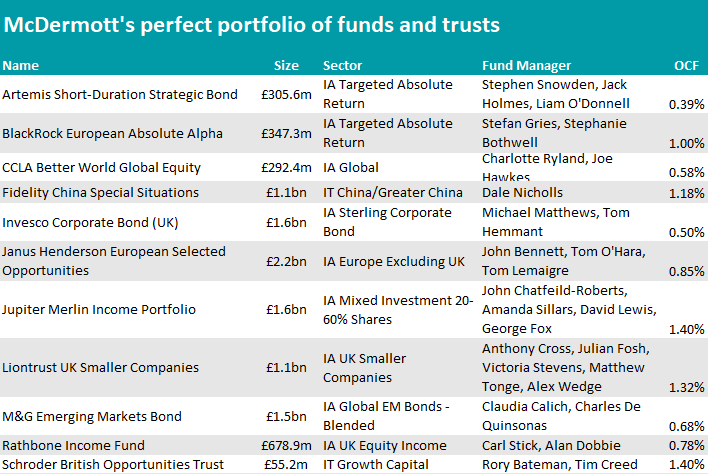

A perfect portfolio of funds and stocks to come out on top this summer.

In both football and investing, picking the best players doesn’t always make for the optimal team; the secret to success is how players’ skills complement each other.

Ahead of the UEFA Euro 2024 football championship, which kicks off on Friday, fund selectors have put themselves in the shoes of football managers to come up with a winning portfolio that strikes the right balance between defensive and offensive plays and has the best chances of coming out on top.

Defenders

Starting with the goalie, it’s all about capital preservation. The Artemis Short-Duration Strategic Bond fund should be able to pull the best saves, according to FundCalibre managing director Darius McDermott.

The fund adapts to changing market conditions by adjusting its allocation to government bonds, investment-grade and high-yield. The focus on bonds with five years or less to maturity “should make it less volatile than the wider bond market”, said McDermott, who also appreciated manager Stephen Snowden’s use of derivatives and futures to reduce risk and manage duration.

The fund has produced a positive return in four of the past five calendar years and also offers an “attractive” distribution yield of 5.21%.

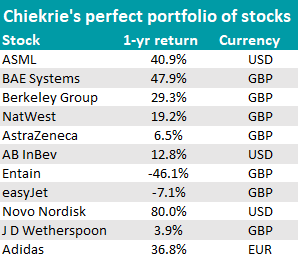

Moving to stocks, Hargreaves Lansdown equity analyst Aarin Chiekrie said that “like the best goalkeeper in the world, it’s hard to see any opponent getting past” ASML, as the Dutch semiconductor company “has a monopoly on the most advanced type of lithography machines used to make the chips that power your phones, computers and even cars”.

As defenders, McDermott chose his back four with some bite.

First up is BlackRock European Absolute Alpha, a long/short pan-European equity fund with a focus on capital preservation and low levels of volatility, but which also managed to almost double the return of the average IA Targeted Absolute Return peer over the past five years, as the table below shows.

Performance of fund against sector over 5yrs

Source: FE Analytics

It is flanked by two bond funds, M&G Emerging Markets Bond and Invesco Corporate Bond, and aided by the Jupiter Merlin Income Portfolio, a “stalwart in the multi-asset sector” designed to provide “an immediate and growing income” as well as the potential for capital growth.

Chiekrie called four players to the pitch: defence company BAE Systems, which is “almost guaranteed to give you a solid performance”; building company Berkeley Group, which “sits on solid ground, despite the current shaky housing market”; NatWest, which convinced him for its new chief executive officer, strong balance sheet and a prospective 5.6% dividend yield; and AstraZeneca, which is seeking to debut 20 new medicines to help fuel growth by 2030.

Midfielders

Midfield is where matches are won and lost, according to McDermott, who turned to Rathbone Income, Janus Henderson European Selected Opportunities and CCLA Better World Global Equity for “goals, flair and bravery”.

The Rathbone strategy has “one of the best – if not the best – track records among open-ended funds for paying dividends,” he said.

“Manager Carl Stick is somewhat of a contrarian investor, so the fund may lag behind while his peers catch up with the news,” but all of its 30 to 50 holdings are chosen for their high quality and visibility of earnings.

The Janus Henderson portfolio is a jack-of-all-trades, mixing mega and large blue-chip holdings with some mid-caps to achieve additional sources of alpha.

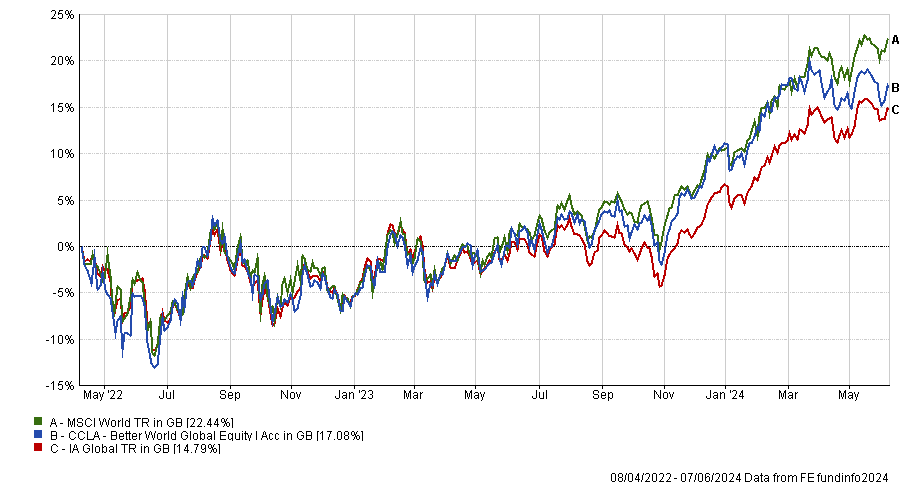

Rising star CCLA Better World Global Equity was launched in 2022 but has proved “very successful since then”, as the chart below illustrates.

Performance of fund against sector and index since launch

Source: FE Analytics

Over in the stocks tournament, Chiekrie put his faith in Belgian drinks company AB InBev, which owns fan-favourite beers such as Budweiser, Corona and Stella Artois.

“Like a midfield maestro dictating the tempo of the game and spraying passes out to all teammates, the group’s diverse portfolio of drinks brands means it has something for everyone this summer,” he said.

The analyst also chose UK-listed Entain, which owns betting houses such as Ladbrokes and Coral.

“It’s been under plenty of pressure from regulators and overall performance has been underwhelming recently, but still, you wouldn’t bet against them turning their form around and making a positive contribution.”

Finally, easyJet looks well-placed with a portfolio of slots at some of Europe’s most valuable airports. It is trading at a cheap valuation despite increased passenger numbers, so there’s scope for this airline to become a fan favourite in the near future, Chiekrie said.

Attackers

For high-octane performance, McDermott has been warming up Fidelity China Special Situations.

Having fallen over 40% since February 2021, the re-rating of China’s equity market has been “indiscriminate”, which has created “plenty of valuation opportunities”.

“With a bias towards smaller and medium-sized companies, this trust is not for the faint-hearted, but manager Dale Nicholls has consistently outperformed his peers and the trust is on an attractive 10% discount,” he said.

For his final two choices, McDermott stuck with recovery plays, this time in the UK.

Liontrust UK Smaller Companies and Schroder British Opportunities Trust should benefit from the recovery of smaller companies, which, coupled with attractive valuations and an increasing number of mergers and acquisitions, could be a compelling opportunity from here.

Source: FE Analytics

“Backed by a market-leading team, the Liontrust fund has a very clearly-defined investment process based on intangible strengths. Every stock in the portfolio must have intellectual property, a strong distribution network or recurring revenues,” the fund selector said.

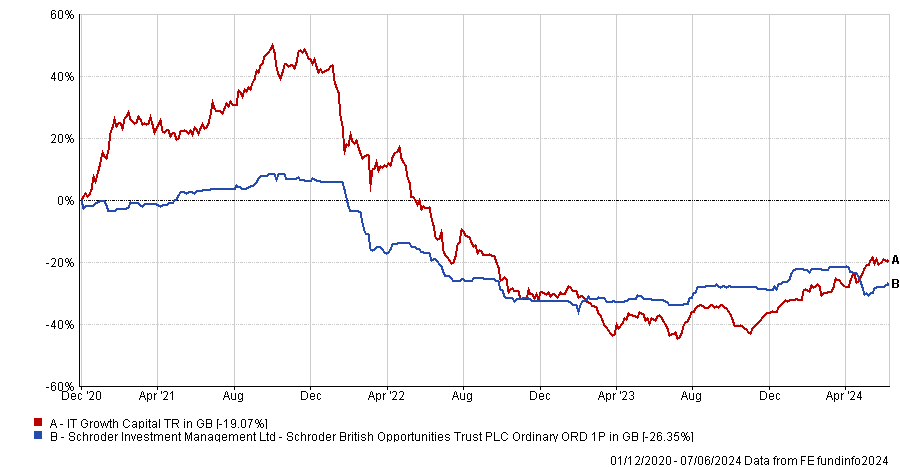

Investing in both public and private businesses, Schroder British Opportunities targets ‘high growth’ and ‘mispriced-growth’ companies.

“Although performance has held up well relative to its peers sentiment has been hit hard, with the trust at a near 35% discount.”

Performance of trust against sector over 5yrs

Source: FE Analytics

Completing the stock squad are strikers J D Wetherspoon and Adidas.

According to Chiekrie, Wetherspoons’ low-value proposition means that “it's well-placed to block out the noise of an unsettled economy and just focus on its own game”, having already scored a like-for-like sales rise of 5.2% last quarter.

On the way home from the match, fans are more likely to pick up an original shirt from Adidas, after host country Germany announced fines of up to £4,000 for supporters caught wearing fake shirts.

“After a challenging 2023, which saw revenue and profits wide of the post, Adidas could be poised to score impressive growth this year,” the analyst concluded.

Source: Google Finance

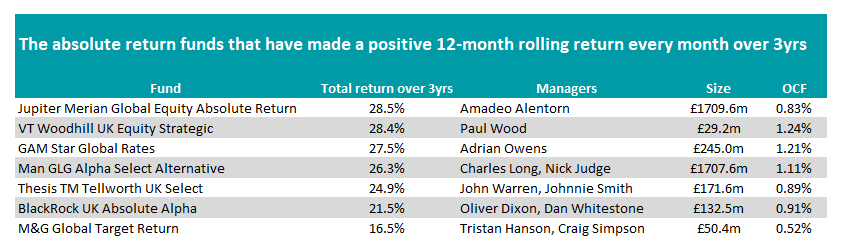

Trustnet looks at the IA Targeted Absolute Return sector to see which funds have achieved positive returns for investors.

Targeted absolute return funds aim to give investors the smoothest ride possible, making a positive return while mitigating volatility. But in the past three years just seven of the 78 funds in the IA Targeted Absolute Return sector have consistently achieved positive gains, according to data from Trustnet.

We looked at the 12-month track record for these funds in each of the past 24 months – the same metric used by the trade body Investment Association to compare the funds’ performance.

Source: FE Analytics

Two behemoths of the sector appeared in the list. First is the £1.7bn Jupiter Merian Global Equity Absolute Return fund managed by Amadeo Alentorn.

A market neutral long/short portfolio, the managers invest in 466 global companies using the team’s systemic equities approach, which tilts the portfolio between different investment styles depending on the trends within the market.

This is coupled with 318 short positions, which are used to mitigate the volatility of market and gives the managers more ways to generate returns. It has been the best performer of the group, returning 28.5% over the past three years, as the below chart shows, and has the second-lowest fees with an ongoing charges figure (OCF) of 0.83%.

Performance of fund vs benchmark over 3yrs

Source: FE Analytics

The other giant of the sector on the list is the £1.7bn Man GLG Alpha Select Alternative fund managed by Charles Long. It invests primarily in UK stocks but, like the Jupiter fund, takes advantage of short positions to add alpha.

With an OCF of 1.11%, the portfolio is more expensive than its Jupiter rival and performance has lagged slightly, with the fund returning 26.3% over the past three years.

The second best performing fund on the list over the period was VT Woodhill UK Equity Strategic managed by Paul Wood, which made 28.4%, just 10 basis points below the Jupiter fund.

With £29.2m in assets under management it is by far the smallest in the group and has the highest fees, with an ongoing charges figure of 1.24%.

It is a UK equity fund, with top holdings including Shell (7.5%), AstraZeneca (7.1%) and HSBC (5.8%). Wood dampens volatility by hedging the portfolio, including being able to “fully hedge” the fund, protecting investors from downside risk. The fund has been hedged in 75% of its days since inception, according to the fund’s factsheet.

GAM Star Global Rates, run by FE fundinfo Alpha Manager Adrian Owens, was in third position with a total return of 27.5%. Unlike the strategies above, it focuses on investing in the currency and fixed income markets with no allocation to equities.

Conversely, TM Tellworth UK Select, run by Alpha Manager John Warren and Johnnie Smith, as well as BlackRock UK Absolute Alpha, headed by Oliver Dixon and Dan Whitestone, also made the list. Both are long/short strategies focusing on the UK stock market.

Analysts at RSMR recommended both funds. On the former, they said: “The fund has been managed in a pragmatic, risk aware manner, allowing returns with no market correlation since moving to Tellworth. The accurate monitoring of potential factor risks has been important to this outcome and the team has generated alpha through stock selection.”

On BlackRock UK Absolute Alpha, they noted: “The fund is run by a specialist long/short hedge fund manager who has developed a strong record in this specialist space. His flexible approach to beta (market exposure), varying net long and net short positions has also added value.

“The manager’s experience, together with the strength of the BlackRock research platform, suggest this fund should be capable of delivering positive returns in most market conditions.”

M&G Global Target Return – run by Tristan Hanson and Craig Simpson – made the lowest return of the group but still achieved the feat of making consistently positive returns on rolling 12-month periods.

Trustnet looks at funds within the Sterling bond sectors that have been run by the same manager since at least 2004.

The fixed income space has proven to be a difficult area for long-serving managers to excel in recent years.

Indeed, only two ‘veteran’ managers – those who have been at the helm since 2004 or earlier – have made top-quartile returns over the past three years across the IA Sterling Strategic Bond, IA Sterling Corporate Bond and IA Sterling High Yield sectors, according to data from Trustnet.

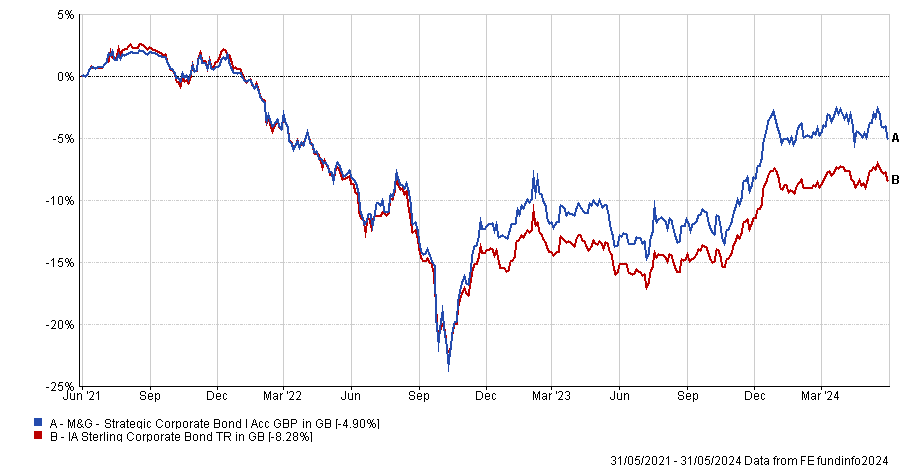

One of those two experienced managers who have stood the test of time is FE fundinfo Richard Woolnough, who has been at helm of M&G Strategic Corporate Bond since February 2004.

The fund – which Woolnough has been co-managing with Ben Lord since 2021 – has fallen 4.9% over the past three years (to the end of May). Nonetheless, it still ranks 23rd out of 90 in the IA Sterling Corporate Bond sector over that period.

Performance of fund over 3yrs (to last month end) vs sector

Source: FE Analytics

Long-term performance has also been commendable, as the fund sits in the sector’s top quartile over 10 and five years.

Although the M&G Strategic Corporate Bond fund belongs to the IA Sterling Corporate Bond sector, its mandate allows Woolnough and Lord to invest up to 20% in government bonds. Additionally, high-yield bonds should not account for more than 20% of the portfolio.

Analysts at FE Investments said: “The investment process begins by agreeing on a view of the global economic environment and how this will affect inflation and interest rates, particularly in the UK. This helps the managers define the appropriate risk level to employ in the fund and identify sectors and asset classes offering most value.

“Credit analysts at M&G study issuing companies across the UK, Europe and the US in order to identify pockets of value, and the portfolio managers combine these recommendations with their macroeconomic views to finalise portfolio positioning.”

They also noted that, historically, the fund has outperformed peers when credit markets rallied, as was the case in 2017 or the second half of 2020, but lagged during sell-offs, such as in 2018 and March 2020.

The other top-performing fixed income fund manager is Eric Holt of Royal London Sterling Extra Yield Bond in the IA Sterling Strategic Bond sector.

Holt has run the five-crown rated fund since April 2003 and was joined by Rachid Semaoune in 2019. Together, they aim to achieve a gross redemption yield of 1.25 times the gross redemption yield of the FTSE Actuaries British Government 15 Year index.

Performance of fund over 3yrs (to last month end) vs sector and benchmark

Chart

Source: FE Analytics

According to the fund’s latest factsheet, unrated bonds and bonds rated BB or below account for 32% and 42.6% of the portfolio, respectively. This suggests a higher exposure to issuers with poorer credit quality, but also higher compensation due to the associated default risk.

In terms of maturity, half of the bonds in the fund are due to mature within 0 to five years, while 31.6% of the securities have a maturity of more than 15 years.

Over the past three years (to the end of May), the strategic bond fund has returned 12.4%, ranking fourth out of 80 in its sector.

Longer term performance has been even stronger, as Royal London Sterling Extra Yield has been the top-performing fund in the IA Sterling Strategic Bond sector, roughly 16 percentage points ahead of runner-up AXA Framlington Managed Income.

Finally, no veteran manager met our requirements in the IA Sterling High Yield sector.

The Rathbone Global Opportunities fund manager explains why the gap between the strongest companies and the rest of the market will widen.

When FE fundinfo Alpha Manager James Thomson took over the Rathbone Global Opportunities fund in 2003, he wanted a simple but repeatable process that would enable him to scale up the fund over time.

This approach has proved successful, as the fund has returned 1,106.8% under Thomson’s 20-year tenure, ranking second out of 94 funds in the IA Global sector since November 2003.

The fund has amassed £3.9bn of assets and continues to be popular with investors. It was one of the top 10 funds for SIPPs on the Fidelity Personal Investing platform in May and was the tenth most-viewed fund on Trustnet during the three months to 20 May 2024.

Performance of fund under Thomson’s tenure and over 10yrs vs sector

Source: FE Analytics

Yet, Thomson believes that equity markets will generally be less rewarding going forward. However, he still sees glimmers of hope, for instance in artificial intelligence.

Below, he explains why the strong will get stronger, why the US is the ultimate growth market and why he avoids Japan and emerging markets.

Could you explain your investment process?

We want as many voices in the room as possible when we're generating investment ideas. We will use our internal analysts, but also a global network of external brokers and analysts. That's how we create a 360˚ view of the investment case. That feeds into our secret sauce analysis, which is a screen of qualities that we look for and qualities that we actively avoid.

The next step is to meet company management and try to understand the drivers of growth, the risks and the strategy and how they change over time. We want an ongoing relationship to understand where promises are being kept and where strategies are being changed and adapted.

Then we think about valuation, timing and suitability. Valuation has to be reasonable given the growth prospects. In terms of timing, we don't want an investment case that takes many years to come to fruition, we want a company that's firing on all cylinders now.

We also want to be able to manage risk effectively. That means having a defensive bucket of weatherproof equities. These are companies that have a more resilient defensive growth profile that's less linked to the economic cycle. That provides a buffer for the rest of the portfolio.

What differentiates you from your peers?

I think there are fewer than 100 UK-domiciled global equity funds that have been in existence for the past 20 years and I believe I am one of the few managers who have been in place for that time period.

Another thing that differentiates us is our willingness to admit that there are areas where we don't have skills and expertise. For example, we avoid investing in emerging markets or Japan. They are important parts of the equity market, but I don't have the skills nor the expertise to do it credibly. I think clients would be better off going to a dedicated emerging markets or a dedicated Japanese equity fund manager.

What have been your best-performing stocks over the past 12 months?

There's been a lot of market concentration around the Magnificent Seven, but I'm pleased that we've had a much broader contribution to our performance over the past 12 months. We own Nvidia and Amazon, but I would also point to businesses such as Costco, Boston Scientific and Amphenol.

Performance of stocks (in sterling) over 1yr

Source: FE Analytics

Outside the US, some of our best performers have been companies like Schneider Electric, which is a play on electrification, digitisation and upgrading electric networks, as well as Partners Group, which is a private equity business that has bounced back very strongly from the malaise in 2022 as rates were rising.

Next, the clothing and apparel retailer, has been a significant outperformer in a pretty soggy UK equity market.

Performance of stock over 1yr

Source: FE Analytics

And the worst-performing stocks?

It’s been primarily defensive, consumer-staple companies such as McDonald's, Coca-Cola, Mondelez and Heineken. It is not a surprise since the market has been looking for cyclicality, recovery in earnings potential and beneficiaries from falling inflation.

Performance of stocks (in Pounds Sterling) over 1yr

Source: FE Analytics

I would also highlight some of our China-exposed businesses such as LVMH, which has really struggled, particularly in its spirits division, and cognac company Remy Cointreau, which we have sold.

What is your view on equity markets hitting all-time highs?

I hope that's a precursor to earnings moving higher to reflect that. Valuation is often a poor predictor of future performance and expensive doesn't necessarily mean overvalued. Often, valuation is reflective of the quality of the earnings you are getting.

The US market is admittedly expensive, but you're paying for resilience, repeatability, adaptability and higher growth. So you're paying a premium in the US because you're getting premium growth credentials. The US really is the home of the growth investor.

What are the main investment themes in your fund?

I would put AI right at the top of my list of investment themes. The computer is no longer just instruction-driven, it is now intention understanding. It’s still early but we are already seeing applications. AI is used for drug discovery and development. Shopify told me that 30% of its coding is being done by generative AI. Video games are going to be produced in record time thanks to AI.

We're all probably going to have some sort of personal digital assistant that helps us with mundane tasks through generative AI.

One of my analysts thinks that AI is going to drive half of incremental GDP over the next decade and will represent 20% of global GDP by 2032. If that's correct, then this is the start of a new industrial revolution.

We have a broader theme called ‘the strong getting stronger’, which is about the increasing concentration of dominance, particularly in technology.

There’s going to be $275bn worth of capital expenditure within technology over the next year, but $200bn is being done by four companies alone.

It’s probably the most important theme we are running. In a world of slower and more inconsistent growth, we think the strong will get stronger.

In 2022, we changed about 20% of the portfolio and repurposed it into the stronger players. We sold some of the earlier stage companies with more expensive financing and an unpredictable demand picture.

We feel they will struggle to outperform in the current market, which is probably leading us toward a two-speed economy.

What do you do outside of fund management?

I have two daughters, so I help my kids to be as well-rounded, stimulated, happy and successful as possible.

I enjoy sitting on the sidelines of sporting events and I like playing tennis. The golf clubs seem to be attracting quite a lot of cobwebs and dust, but hopefully they will come out of the basement when the girls are a bit older.

Trustnet editor Jonathan Jones explores the impact rate cuts will have on markets.

This week, the European Central Bank took the lead on monetary policy by becoming the first of the big three central banks to cut interest rates.

It was the first time in five years the ECB has cut rates, with the Bank of England (BoFE) expected to join its peer from the continent in the coming months.

The big question is what the Federal Reserve will do. After all, experts have warned that the BofE and ECB can’t go too much further without the Fed doing the same, or risk currency fluctuations that would be prohibitive to their inflation targets.

Next week, the US central bank will meet for the fourth time this year, but there aren’t many signs it is gearing up for a rate cut.

Most expect the result to be the same as the previous three meetings: no change in the headline Fed Funds interest rate of 5.50%.

The CME Fedwatch service has a 2% chance of a Fed surprise drop of interest rates, which feels pretty conclusive.

Russ Mould, AJ Bell investment director, said: “As such, the wait for the first, elusive reduction in headline borrowing costs continues, especially as financial markets began 2024 expecting six rate cuts from the Fed, down to 4% by the end of the year, with the first of those coming in March.”

This has been scaled right back, with markets now predicting just two cuts in 2024 down to 5%, with the first one coming in September. Yet, even this is far from given.

“The Fed has to acknowledge that unemployment is low at 3.9% and inflation, as measured by the consumer price index, is 3.4%, still some way above its 2% target,” Mould said.

“The Atlanta Fed’s Sticky-Price CPI index is up 4.4% year-on-year, to suggest the central bank has more work to do, especially as producer prices and the Fed’s own preferred measure, the Personal Consumption Expenditure index, are showing fresh signs of heating up, rather than cooling down.”

As such, most predict the Fed is a few months away from starting its rate cutting cycle – as is the Bank of England, which could hold off to move in lockstep with its US counterpart.

For investors, it means the discount rate applied to growth stocks will remain higher for a little while longer, but there is still a general trends lower.

In the coming months, the likes of the big tech names should start to face an easier time of it from a macroeconomic perspective – as if they needed the help.

Cash rates will start to drop, although rates are not expected to plummet, which should mean they remain relatively attractive, while bonds too could thrive as yields start to drop.

In all, it could be a strong period for investors, who will have a litany of options to choose from to make money. At least that’s the theory.

In practice, these things are never straightforward and other shocks could derail any sort of stabilisation from the macro picture. Solid research and decision making will remain key, even if it seems as though the future looks bright.

Experts stick with the multi-boutique house despite some of its funds underperforming.

Having a consistent investment process is key in asset management, and a good manager will stick to their approach even when it is out of favour.

This has been happening to some of Liontrust Asset Management’s funds recently, particularly in UK small- and mid-caps, but experts agreed that the group’s overall offering remains strong.

Liontrust can be described as a “multi-boutique” whose teams have their own distinct processes and franchises, and its business model is based in part on strategic growth through acquisitions.

One thing the firm has got right with this model is retaining key talent, said FundCalibre managing director Darius McDermott.

Historically, Liontrust’s flagship has been the Economic Advantage team, which manages a range of UK equity funds, including Special Situations, UK Growth, UK Smaller Companies and UK Micro Cap.

The long-term track record of these funds is strong, with the UK Smaller Companies fund being the top performer in the 40-strong IA UK Smaller Companies sector over the past 10 years.

Over five years, UK Growth and Special Situations have fallen into the second and third quartile, respectively; Special Situations stayed in the third quartile over the past one and three years.

Historically, small and mid-cap stocks contributed strongly to the Economic Advantage funds, but weak investor sentiment towards these areas has impacted their performance in the past few years.

A Liontrust spokesperson said that the team remains “passionate believers” in the long-term compounding potential of the entrepreneurial, high-quality smaller companies in which they invest – and so did McDermott.

He emphasised the “excellent” long-term track record under FE fundinfo Alpha Managers Anthony Cross and Julian Fosh, who have returned more than 100% to investors over the past decade. McDermott said this is “concrete proof that the process of targeting companies which must have intellectual property, a strong distribution network or recurring revenues holds up well over the long-term.”

Jason Hollands, managing director at Bestinvest, agreed: “I’ve long been a fan of the overall approach, which has delivered very consistent performance. Liontrust UK Growth is also a Bestinvest top pick for the UK market.”

A prime example of Liontrust’s multi-boutique and inorganic growth strategy is the 2017 acquisition of Alliance Trust Investments, now the Liontrust Sustainable Investment team, which manages the Sustainable Future range of strategies.

For this range, 2022 was the most challenging year since inception in 2001. Only the Corporate Bond and the Monthly Income Bond funds managed to buck the downward trend, while the European Growth fund has been anchored to the bottom quartile of performance and Global Growth steadily fell from the second to the third, then the fourth quartile – as shown in the table below.

Source: FE Analytics

According to a Liontrust spokesperson, this was due to a series of headwinds, including an abrupt change to the macroeconomic backdrop, higher bond yields and weakness among the growth-focused and quality stocks in which the team invests.

Nonetheless, stocks in the Sustainable Future funds “delivered growth despite the low growth economy”, he said, which is “testament to the structural nature of the themes the team invests in, which the managers believe have strengthened, such as energy security, innovation in healthcare and environmental efficiency”.

For Hollands, the Liontrust Sustainable Future Growth fund’s underperformance “isn’t a surprise” and is “not problematic either”. Most environmental, social and governance (ESG) funds have underperformed, given they missed out on the rally in energy and commodities, he explained.

Hollands still regards the Sustainable Investment team as a jewel in Liontrust’s crown.

The Sustainable Future multi-asset offerings have also faced challenges, said McDermott, but are backed by “one of the most experienced and well-resourced teams in the game”.

“We retain confidence in their ability to deliver long-term growth, especially considering the continued relevance of the themes the team invests in – energy security, healthcare innovation and environmental efficiency,” he concluded.

Some funds attached to other investment hubs within Liontrust have also underperformed, including the Global Smaller Companies and US Opportunities funds, as shown below.

Source: FE Analytics

The US Opportunities fund is managed by Hong Yi Chen, who joined Liontrust when it acquired Majedie Asset Management in 2022. The fund has just been moved into the new Liontrust Global Equities team headed by Mark Hawtin. Its investment process has evolved to focus on companies with the potential to exploit change and with catalysts to unlock value.

But the area where Hollands was most sceptical was emerging markets.

Liontrust’s China strategy came 30th out of 36 funds by 10-year performance and has been relegated to the third quartile over the past one, three and five years; the Latin America strategy was the bottom fund in the nine-strong sector over five years.

But Hollands was more concerned about Liontrust Emerging Markets, which came to the group in October 2019 via the acquisition of Neptune Investment Management.

“It is a tiny fund at £9m and appeared in Bestinvest’s last Spot the Dog report as a serial underperformer. At such a small size and with its recent track record, I doubt it is viable,” he said.

Liontrust said most of the underperformance derived from its overweight positions in large-cap technology shares during 2021 and early 2022, which were costly due to a downturn in the semiconductor industry.

Additionally, Brazil dragged on performance as the team’s expectations of recovery initially proved too optimistic – although during the past year, Brazil’s recovery has been a positive contributor to performance.

Asset managers previously covered in this series are Jupiter Asset Management and Schroders.

After election-related volatility settles, consumption stocks are expected to benefit from new populist policies while infrastructure spending could slow down.

India’s election results have surprised everyone, unleashing a week of volatile swings in one of the world’s most expensive and most-watched stock markets.

Indian equities hit an all-time high on Monday 3 June in anticipation of Narendra Modi’s Bharatiya Janata Party (BJP) achieving a majority. The stock market then plummeted as results from the early vote count rolled in. A coalition government now appears the most likely outcome.

Peeyush Mittal, who manages Matthews Asia’s India strategy, expects “volatility to continue as the next government takes shape”.

The new coalition government is likely to introduce more populist policies to drive consumption but will probably hit pause on infrastructure spending, which had been a priority for Modi, Mittal said. As a result, he expects sectoral leadership in the stock market to change in favour of consumption stocks, away from capex-led themes.

“We think capital goods and infrastructure-related sectors spanning industrials and materials will face headwinds in the near term and associated stocks will likely be negatively impacted. There are grey areas, such as power and defence, which should be less affected as these are less sensitive to partisan issues,” he said.

“But it will be consumption-related sectors like consumer staples, traditionally strong areas like pharmaceuticals, and other areas that may be more favourably looked upon by an evolving coalition that could fare the best in the coming weeks.”

Mittal pointed out that consumption growth has been weak in India despite strong GDP expansion during the past two years, which he said indicates there are not enough employment opportunities for lower income groups.

“Post-Covid, the economic recovery in India has been K-shaped, with some sectors and socio-economic groups bouncing back while others have struggled and experienced a loss of savings, particularly citizens on lower incomes and those in rural areas,” he said.

He thinks consumption growth needs to improve for GDP growth to be sustainable.

Mittal also warned that small and mid-cap stocks are likely to experience prolonged volatility given their elevated valuations.

Amol Gogate, manager of Carmignac Portfolio Emerging Discovery, was more bullish about India’s prospects, even though managing a coalition could slow down the government’s pace of execution.

“While the election results are certainly a dampener for the markets and sentiment in the short term, they also showcase that India is a true democracy. And with Modi at the helm, it seems likely the next phase of economic development will proceed and the long-term investment case for India, for now, remains solid,” he said.

Investment into India’s bond markets is set to spike as a result of India’s inclusion in JP Morgan’s emerging markets government bond index this month and Bloomberg’s emerging market local currency index in September 2024. These events could bring in up to $40bn of foreign investment, which Gogate thinks will have a ‘halo’ effect on Indian equity markets as international investors become more familiar with the country.

“This capital boost, combined with Modi’s pro-business stance and a well-managed domestic financial system means Indian markets are poised to continue their upward march. However, with valuations already high, and a less certain political landscape, volatility may increase, so selectivity is becoming more important,” he explained.

His outlook for the stock market differs from Mittal’s. “In our view, small and mid-cap firms will benefit from a likely capex upcycle, as well as the financial services, high-end manufacturing and real estate sectors. The most disruptive businesses, with the highest potential for rapid growth will emerge on top thanks to a highly supportive ecosystem for budding companies,” Gogate said.

John Pattullo, co-head of global bonds at Janus Henderson, plans to retire in March 2025, leaving Jenna Barnard as sole head of the team.

Janus Henderson Investors’ co-head of global bonds, John Pattullo will retire in March 2025 after 27 years with the firm.

Jenna Barnard will assume sole leadership of the global bond team and retain portfolio manager responsibilities for the funds she runs alongside Pattullo, with whom she has worked for 20 years.

They both co-manage the £2.3bn Janus Henderson Strategic Bond fund and the £1bn Janus Henderson Fixed Interest Monthly Income fund, among others.

Nicholas Ware, who has been a fixed income portfolio manager at Janus Henderson since 2012, will become a named portfolio manager on all Janus Henderson’s strategic bond and developed world bond funds as part of the firm’s succession planning.

Analysts at RSMR said the Strategic Bond fund is a core option for conservative investors, with an emphasis on quality, capital preservation and consistent returns. Performance has trailed the sector average over five years, as the chart below shows, but RSMR’s analysts said this fund tends to perform better in risk-off markets.

Performance of fund versus sector over 5yrs

Source: FE Analytics

Barnard and Pattullo employ a thematic macro framework, looking at the structural drivers of economies such as excessive debt, inequality, globalisation, demographics and technology. “This approach results in more of a holistic view of what the managers term the ‘climate’ of investing and provides a framework which excludes a lot of the short term market noise,” RSMR explained.

Barnard and Pattullo describe their philosophy as “sensible income”, with the goal of delivering consistent returns via an understandable investment approach.

“The ‘sensible’ theme results in a large proportion of the investment universe being screened out,” RSMR analysts said.

“As you might expect, the screen removes highly cyclical and operationally and financially leveraged issuers and it also excludes industries and companies that fail to consistently generate value. The team is essentially looking to invest in quality credits and avoid unstable, risky sectors and companies.”

The recent rally may be a taste of things to come for the UK’s smallest companies.

The role of AIM stocks in tax mitigation is well-established; however, in recent years, with AIM impacted by broad disillusionment with the UK stock market, it has been harder to make the investment case. This has resulted in the valuations of many AIM companies hitting all-time lows, but there are several catalysts now evident that should help improve the performance of the index.

The UK’s smallest companies have been widely unloved. They have been on the front line of negative sentiment towards UK stocks and seen as more vulnerable to weakness in the domestic economy. They have been on the wrong end of a general flight to safety among investors. Rising interest rates have also been a headwind, with the valuations of smaller growth companies regarded as more sensitive to higher borrowing costs. However, markets tend to overshoot, and we see real value emerging today.

Operationally, many of the AIM businesses in which we invest have proved sound. They have continued to deliver strong growth despite a more difficult economic environment and have proved resilient in the face of higher interest rates. The combination of weaker share prices and stronger earnings has left many companies looking attractively valued, relative to their larger capitalisation peers.

A contributing factor has been a widespread misunderstanding of the relative risk of AIM companies. While there is certainly higher risk associated with speculative companies within the index, there are also plenty of well-established companies with strong business models, low debt and clear visibility on earnings.

An example of the latter is James Halstead, which manufactures and supplies flooring for commercial and domestic use. Its end markets include defensive sectors such as health and education, reducing exposure to the broader economic environment. It has cash on its balance sheet and the Halstead family still has a significant share of the ownership.

Valuations