Is it finally time for UK equities to shine?

Uninspiring, underperforming and deeply unpopular. Just a few of the adjectives that spring to mind given the divergence in the fortunes of UK equities and their US peers over the past couple of years.

April ushered in the 35th consecutive month of net outflows from UK equity funds and, putting this into context, UK investors poured more money into North American equity funds in the four months ending March 2024 than in the previous nine years combined, according to Trustnet.

It feels as if we’ve banging the drum of UK equities for an age but is light starting to appear at the end of the tunnel? Quite possibly, if the recent performance of the FTSE 100 is anything to go by: the leading UK large-cap index hit a record high earlier this month.

So what’s behind this sudden reversal in fortunes? One of the key catalysts has been an improving macroeconomic environment. The UK has bounced out of one of the shortest recessions on record with better-than-expected GDP growth in the most recent quarter, while April saw output rise to its highest level in almost two years.

That said, Britons are nothing if not a self-deprecating bunch and gloomy business and consumer confidence had become increasingly divorced from improving fundamentals.

However, both measures ticked up in March and, although the Base rate is frozen for now, Bank of England governor Andrew Bailey recently announced that rate cuts were “likely” with inflation predicted to fall close to its 2% target in coming months. All this paints a more positive macroeconomic picture.

Turning to the stock market specifics, valuations remain attractive relative to global peers. The MSCI UK index is trading on a forward price-to earnings (P/E) ratio of 12x, compared to 21x for the MSCI US index (according to Yardeni, as at 15/05/2024).

The rationale is usually attributed to US stocks offering superior earnings growth (and this is undoubtedly the case in some instances) but this valuation gap looks stretched given forecast earnings growth for the FTSE 100.

The FTSE 100 may be (rather harshly) labelled the ‘Jurassic Park’ of stock markets due to the dominance of ‘old economy’ sectors such as mining, pharmaceuticals and financial services. But that overlooks the strong secular growth drivers of mega-trends including the soaring demand for commodities in the move to net-zero and the increasing reliance of an ageing demographic on the pharmaceutical industry, amongst others.

And, in actual fact, some of those ‘dinosaurs’ have delivered superior returns to their glitzier US counterparts. And let’s not forget that the FTSE 100 boasts more than its fair share of leading multinationals too, with more than 75% of revenue generated outside the UK.

Despite the recent bounce, valuations also remain well below long-term averages, particularly further down the market-cap spectrum. A good litmus test of valuations is the level of M&A activity, and bargain hunters have continued to hoover up UK companies.

Last year saw the acquisition of 10% of the UK small-cap index, with overseas buyers accounting for almost half of these transactions. This year has seen interest move up the market-cap spectrum, with bids for FTSE 100 mining giant Anglo American and packaging company DS Smith.

M&A activity has also proved a tailwind for active fund managers, particularly those with more concentrated portfolios, such as Rockwood Strategic. Manager Richard Staveley holds a portfolio of around 20 companies with a focus on sub-£150m companies to exploit pricing inefficiencies from a lack of research coverage.

As a result, acquisition premiums can provide a significant boost to returns and Staveley believes that 80% of the trust’s holdings will ultimately be acquired by a trade or private equity buyer.

Recent bids for portfolio companies include OnTheMarket, The City Pub Group, Finsbury Foods and Crestchic. These acquisitions have contributed to Rockwood comfortably topping the AIC Smaller Companies sector with a five-year net asset value total return of 88%, compared to a sector average of 29% (as at 14/05/2024).

A recent addition to the portfolio was Funding Circle, a leading UK and US lending platform to small businesses. Rockwood acquired a 3% stake in January, when the market cap was £110m and substantially below book value (with the company holding £170m in unrestricted cash, plus a further £110m in restricted cash and loans at that point).

The management team has announced a focus on the UK business going forward, together with a share buyback program, resulting in a year-to-date share price increase of 106% (as at 15/05/2024). Funding Circle’s market cap is now approaching £290m, demonstrating the value of stock-picking skills in an under-researched market.

Looking ahead, it may be too soon to say UK equities are finally out of the woods given the backdrop of uncertainty, but the pendulum certainly looks to be swinging back in their favour. Improving investor sentiment could prove the final catalyst to spark a sustained recovery and maybe, just maybe, month 36 of fund flows will mark a change in fortunes of UK equities.

Jo Groves is an investment specialist at Kepler Partners. The views expressed above should not be taken as investment advice.

Newly named Hall of Fame Alpha Manager David Walton explains why European smaller companies are a better investment than UK and global ones.

There is a lot of anticipation for smaller companies to recover after some painful years. However, investors should be aware that many large funds have commercial reasons to avoid the sector altogether, leaving returns on the table.

That’s where David Walton, manager of the IFSL Marlborough European Special Situations fund, who this year entered the FE fundinfo Alpha Manager Hall of Fame, steps in.

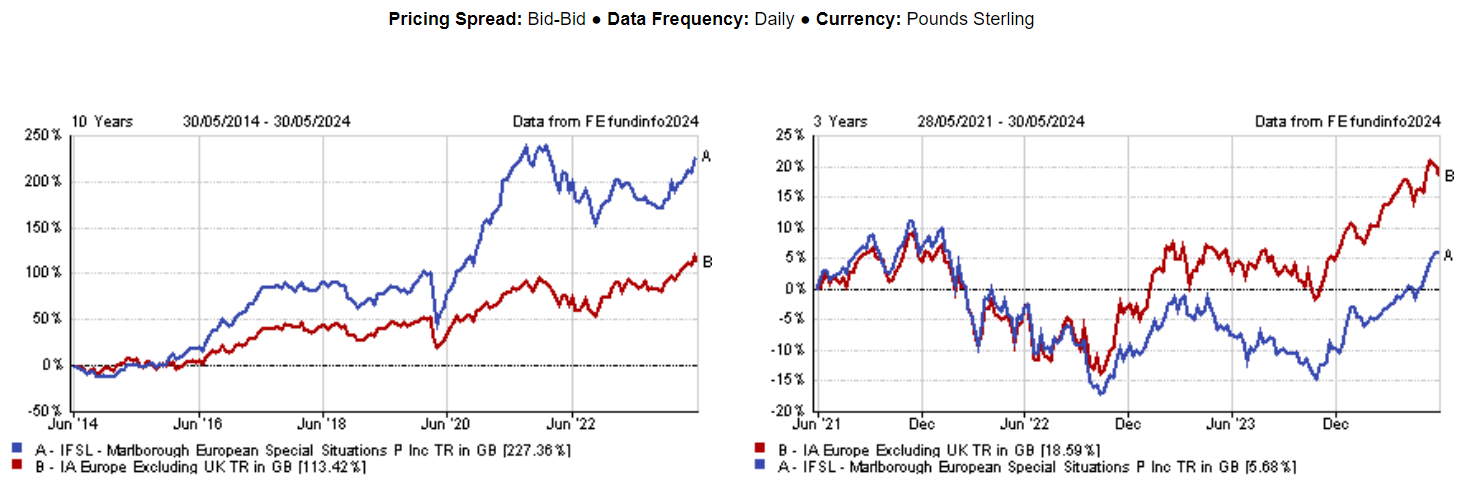

With £270.3m of assets under management, the fund is the right size to take advantage of many overlooked opportunities and has been the first performer over the past 10 years against the then 99-strong IA Europe Excluding UK sector, maintaining a first-quartile ranking over five years too.

Below, he explains why big funds are creating an investment “anomaly”, why European smaller companies are a better investment than UK and global ones, and why investing when the sky is cloudy leads to better outcomes than when it’s clear.

Can you summarise your investment process?

We invest in companies that are growing their profits at an above-average rate, have a good management team and whose shares are attractively valued, trading at price that’s not reflecting the company’s future growth potential.

We're not looking for loss-making or marginally profitable companies with a relatively unproven business model that promise to expand and earn huge profits. We are also not looking for companies in sectors that are appealing for investors at that time and focus instead those that are not on most investors’ radars, perhaps because they are small or somewhat obscure.

What type of companies does this correspond to?

We choose to look particularly at the small and micro-cap end of the market, where you can find the greatest under-valuations. Most managers of large funds won't look at companies below the £250m threshold because micro-caps don’t move the needle for them. It’s a perfectly rational, commercial reason, but it does create a market anomaly.

The size of this fund is such that we're able to take advantage of that anomaly and today, around 20% of the fund is in micro-caps.

Why should investors pick your fund?

If an investor is prepared to invest for at least five years, there is the potential to make good returns with this fund.

We're not in control of if and when share prices go up, so ours is a buy-and-hold strategy – it does take time for some of these companies to develop and grow. The fund can go through a number of years of fairly mediocre performance, but over a longer period, if we’re able to be patient with the holdings, we can get the benefits.

Why did the fund drop to the fourth quartile over three years?

The fund had strong gains in 2020 and 2021, when there was a boom in Europe, fuelled by Covid-era subsidies. With hindsight, we were too slow to take profits on number of Covid winners, for example, the Finnish sauna equipment maker Harvia. We were selling it on the way up and on the way down making good money on it, but we didn't take the chance to sell enough of it higher up.

There were a few other examples like that, which cost us on the way down in 2022.

Performance of fund against sector over 10 and 3yrs

Source: FE Analytics

Why are European small-caps a better investment than global or UK ones?

In Europe, you are investing in a market which is still somewhat underdeveloped compared to the UK and the US in terms of the equity culture. The size of the stock markets, compared to GDP, is also clearly lower in Europe.

On top of that, there are certainly headwinds which are affecting small companies now, but sometimes investing when the sky is a little bit cloudy can be better than when the sky is completely clear blue.

The war in Europe – obviously a human tragedy – is impacting the valuations of European equities, particularly the ones focused on domestic European economies. Most of these are smaller companies, which have got less diversification by geography compared to large-caps.

What stock was the best contributor to performance recently?

The fund’s biggest holding currently is Sarantis, a sort of Greek Unilever selling basic household goods. Its share price has gone up from €6.5 to €11 over the past 18 months, partly because of its aggressive growth plan.

It has expanded from Greece into the Balkans and Southeast Europe as bigger groups such as Procter and Gamble have retrenched from peripheral countries. Serrantis’ model is to acquire sales force in new countries and bring their products to the newly acquired retail customers, paired with some organic growth too.

We bought into it for the first time in 2016, a time when Greece was seen as a no-go zone for some investors. But the company itself had a good buying story behind it and we still hold it today.

What didn’t work as well instead?

A French company called Bilendi has been struggling but should be posed for recovery. It runs online research panels collecting data by asking any sort of questions to paid volunteers and then selling that data onto other companies who write market research.

The company did well for a period of time until last year, when its sales growth started to suffer, more than halving the share price. Today it’s at €17.9, down from €20.5 at end of December 2022.

We've held it because it didn't have any financial difficulties, it’s simply experiencing a headwind to its growth. One of its competitors however has recently become overly indebted because of a private equity buyout, so it might be an opportunity to gain some market share back.

What do you do outside of fund management?

I have a very full family life. I have four children so I'm often supporting their activities. Or I’d be hill walking with friends or family.

People have a shocking lack of understanding when it comes to their retirement savings.

Pensions are in the spotlight as both the Conservative and Labour parties draw their lines in the sand over what to do with retiree’s savings ahead of the general election in July.

It is probably the biggest dichotomy between the two main rivals in the financial sphere, with different opinions on the lifetime allowance and the ‘triple-lock’ scheme, with prime minister Rishi Sunak proposing ways for retirees to keep more of their state pension.

Even without this, however, there is a clear lack of understanding among people and their pensions. Data from AJ Bell found almost half (48%) of British adults under state pension age say they don’t know when they’ll receive it, for example.

Tom Selby, director of public policy at AJ Bell, said: “Millions of Britons risk sleepwalking into a retirement shock, with almost half of all adults under state pension age admitting they don’t know when they’ll receive their state pension.

“This likely in part reflects a lack of engagement with pensions, particularly among young people, and in part the lack of certainty that exists around state pension policy.”

So, let’s talk about pensions. They are crucial for people as the state pension alone may not be sufficient to maintain your desired lifestyle, even if the Conservatives do plan on supercharging the current triple-lock scheme.

At present, the state pension age is 66 years old for both men and women but this will start gradually increasing again from 6 May 2026. For those aged between 18 and 34, it will rise to 68 by the time they get to retirement.

The full level of the State Pension is £221.20 a week in the 2024/25 tax year, which produces an annual income of £11,502.40, although this can be lower depending on how many years you have paid national insurance (35 years is required for the full amount). It rises in line with inflation, wage growth or 2.5% – whichever is higher.

Daniel Chaplow, wealth planner at Succession Wealth noted however that this alone “may not be sufficient to maintain your desired lifestyle”.

As such, it is important for people to contribute to a pension plan, whether that be through a workplace pension scheme or a self-invested personal plan (SIPP).

The obvious benefit to putting into a pension today is tax relief: you will receive tax relief at the highest rate of income tax that you pay. The basic 20% tax relief will be added to each contribution, while higher or additional rate taxpayers will need to claim back the extra tax relief via their tax return. The maximum you can typically squirrel away each year is £60,000.

Yet, even here there is confusion. According to a survey by Hargreaves Lansdown this week, a whopping two thirds of respondents did not know their retirement savings were invested in the stock market.

Helen Morrissey, head of retirement analysis at Hargreaves Lansdown: “People have fundamental misconceptions about pensions. These findings are stark, but not altogether unexpected.

“We talk about saving into a pension rather than investing and so it’s highly likely people think their contributions are going into some kind of savings account rather than into the markets.”

When you invest in a workplace pension, the money will likely be put in a default fund, which will invest in a mixture of equity funds and bond funds with the weighting to each based upon your age and years to retirement. The younger you are, the more you will have in equities. The older, the more in bonds.

This is a great way for people with no investment experience to invest but is not right for all and can tend to be overly cautious the closer you get to retirement. It is always worth keeping track of what you are investing in and if it aligns with your goals – seeking financial advice if you are unsure.

If you know nothing about your retirement planning or where your pension is invested, now is the time to get looking at it.

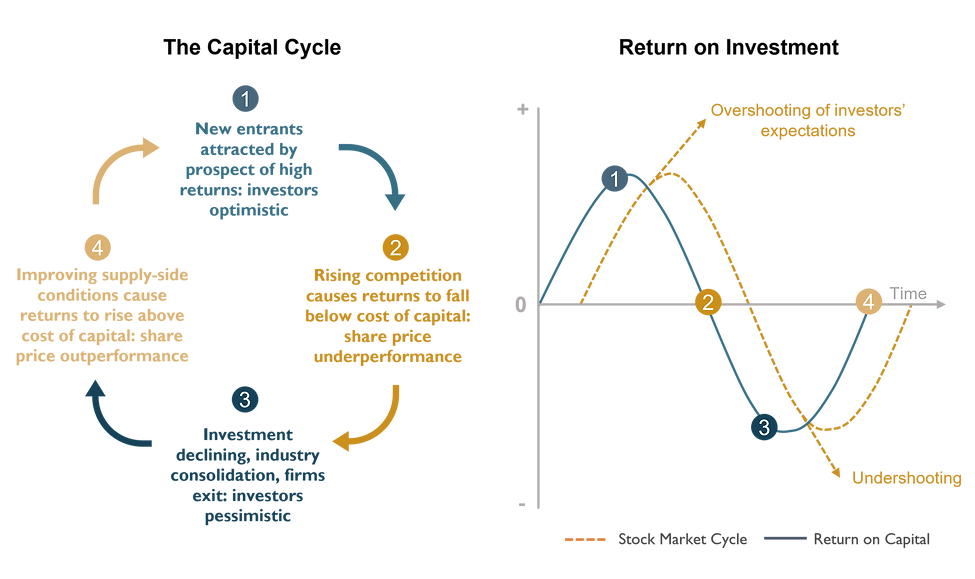

Following the capital cycle model, both sectors will have lower returns going forward.

What do investments focused on the green economy and those buying into artificial intelligence (AI) have in common? They are both due to generate disappointing returns going forward, according to Django Davidson, portfolio manager at Hosking Partners.

In Hosking’s global equity strategy, Davidson’s goal is to deploy a capital-cycle approach to find hidden gems and at the same time avoid market bubbles. His verdict on green investments and AI – both are bubbles and best avoided.

The green capital deployment cycle fits the bubble description, said the manager, as it's been driven by predictions of future demand, government regulation and diktats, generating a very significant supply response.

“It all goes back to that idea of demand stories and supply facts. Investors in the green energy transition sector have been sold a cake-and-eat-it story: you can have higher returns and do good for the planet,” he said.

“But as per capital cycle theory, when management teams raise money and deploy it in the stock market, seeing valuations of two to five times the invested capital, the result is capital misallocation.”

While it goes without saying that we all want future generations to inherit a planet in the best shape it can be, capital cycle investors such as Davidson are “hardwired” to be highly sceptical of demand-based stories such as this.

The main point that he made is that, with all else being equal, the more cash goes into an industry, the lower returns will be for that capital within that industry due to more competition, which drives down prices and lowers returns.

Cash is then pulled out, which leads to pessimism and consolidation. Then the newly-reset supply side sets up a more exciting supply-side venture and returns improve, he explained.

To further illustrated his point, the manager used the chart below, where the blue line represents the industry return on capital and the yellow line is the stock market's interaction with the underlying return on capital.

The capital cycle and returns on investment

Source: Hosking Partners

“The stock market is terrific at amplifying these cycles all the way up and on the way down and management teams are the great accomplices in this tool,” Davidson said.

“If you can deploy $1 of capital and have it valued at two or three or four times that, the incentive is to deploy capital.”

Following this model, the manager is predicting woes for three areas in particular – electric vehicles (EVs), offshore wind, and AI.

An example of the capital-cycle approach in action is what’s happening in the EV space, which Carlos Tavares, chief executive officer of automaker Stellantis, called “a bloodbath” by looking at Tesla car prices and the competitive response in China.

This is also something that has concerned Douglas Scott, co-manager of the Aegon Global Equity Income fund, who said if there was one member of the US’ ‘Magnficent Seven’ that would be under pressure it would be Tesla.

“China has 100 electric car companies. It’s a big number. China is not going to displace Microsoft or Amazon. Nvidia would be very difficult given the position it is in. Google no. Apple maybe a little bit.

“[Tesla has] 100 competitors out there and a product that the man in the street can’t afford. They just can’t afford $50,000 for a car. If you give them something similar for $20,000 they’ll take it.”

Davidson noted Chinese manufacturer BYD sells its Seagull model for even less than this – just $10,000 in China, referring to it as the “Volkswagen Polo of the EV world”.

“Even if we put on 100% tariffs, that is still $20,000 – pretty good value compared to what the original equipment manufacturers are offering,” he said.

“It's highly likely that the very significant proportion of the capital deployed into the EV space is going to see a prolonged period of lower returns as per capitals cycle theory. That's why we can see these car parks of Chinese EVs clogging up European ports,” the manager concluded.

A similar misallocation of capital went on in offshore wind companies such as Danish energy company Oersted, which was a symbol of the European green transition and at its peak was valued at 13 times sales.

That was “a terrific environment” for Oersted to raise capital, according to the manager, with the subsequent 75% fall in share price “demonstrating the value destruction that can happen because of these demand-led, futurology investment waves”.

Stock price of Oersted A/S over the past year

Source: Google Finance

That’s what investors should prepare for in the AI space as well. In fact, the increase in the level of capital being deployed by the cloud hyper-scales is “extraordinary” – a perfect run-up to disappointment.

In 2019, the invested capital of the four large hyper-scalers in cloud computing was $180bn; by the end of this year, with rolled-forward capex plans, it will be $75bn, the manager explained.

“More capital, with all else being equal, means lower returns, even in AI. Now, the response to that will be: ‘but it's a great market, there aren't very many hyper-scalers, and they'll be able to effectively collude on pricing’. I don't believe that,” Davidson said.

“I would also point out that in China, no one makes any money with cloud. It's working well for the large US companies today, but there is no preordained structure that means you must make a lot of money in this industry.”

Experts ponder whether the recent rally in Chinese equities is sustainable.

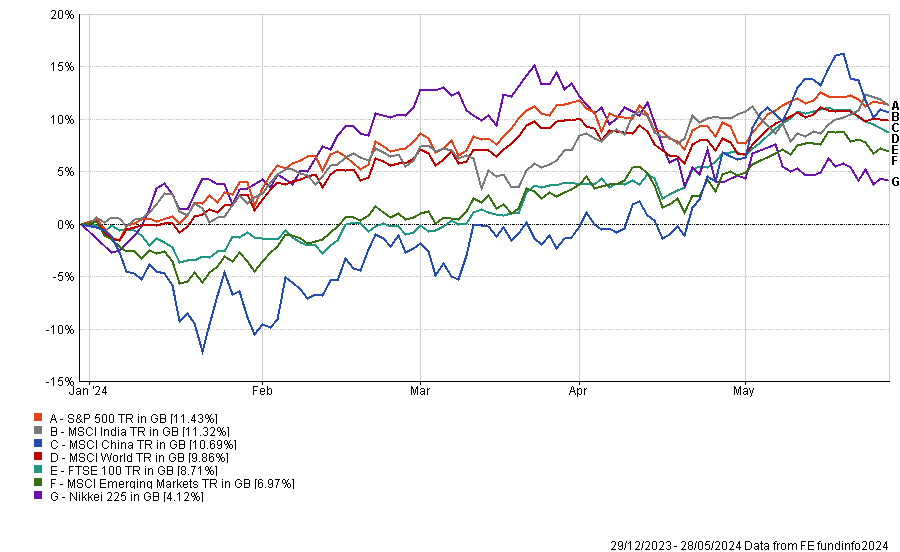

Chinese equities have recently staged a comeback after three consecutive calendar years of significant negative returns, linked to regulatory crackdowns, a crisis in the property sector and questioning around the country’s growth trajectory.

Since the beginning of the year, the MSCI China index has outperformed the MSCI World and MSCI Emerging Markets, although it has lagged the S&P 500 and its emerging markets rival, MSCI India.

George Efstathopoulos, multi-asset portfolio manager at Fidelity International, attributed China’s rebound to a combination of factors.

“The ‘national team' [state-backed financial companies] has stepped up their involvement in markets after the capitulation earlier in the year,” he said.

“The growth outlook appears to have improved – GDP growth recently surprised to the upside, leading many analysts to raise year-end growth estimates and causing some foreign investors to cover underweight positions. Policy support has also increased recently, with the ailing property sector the latest recipient.

“Meanwhile, Chinese companies have carried out more buybacks recently and earnings beats are being rewarded in this earnings season, which hasn't been the case in the last few years, a further indication that the capitulation period is over.”

Performance of indices year-to-date

Source: FE Analytics

The question for investors now is whether this rebound is sustainable or merely a dead cat bounce.

Sandy Pei, deputy manager of the Federated Hermes Asia ex-Japan Equity fund, argued that the bounce has been “very modest” so far and that absolute and relative valuations remain attractive. She believes that investors in China have huge upside potential if Chinese equities re-rate to “normal” multiples.

David Townsend, managing director of Value Partners’ business in Europe, the Middle East and Africa, is also bullish on China and argues it is in the early stages of a U-shaped recovery.

He said: “From a fundamental perspective, we maintain our investment thesis that the stock market has reached an inflection point, supported by the recent strong market performance.

“We anticipate the start of a longer-term market upturn, supported by strong fundamentals such as healthy corporate balance sheets and large household deposits, which could sustain China’s long-term growth story.”

“From a technical perspective, it also looks like the market rally could continue for some time, especially given the very light / underweight positions for many investors in China. It does look as though some capital is starting to come back to the market to reduce the underweight exposure of many long-only investors.”

Yet, others believe it is still too early to tell whether Chinese equities are back on track.

For instance, Efstathopoulos stressed that earnings will need to deliver for the bounce to prove sustainable and this will require an improvement in the currently fragile consumer sentiment in China.

Rob Brewis, co-manager of the Aubrey Global Emerging Markets Opportunities fund, also warned that the property market is still in the doldrums, monetary growth subdued and deflation remains predominant. He also believes that geopolitics and trade frictions are going to increase ahead of the US election, while a trade war between China and Europe seems to have started.

For example, ministers of Germany, France and Italy called for a common front against China’s expanding export power last week during a G7 meeting. Moreover, the European Union is investigating a range of Chinese products, including electric vehicles, to assess whether they are receiving unfair subsidies from the Chinese government or being sold below cost.

Another risk highlighted by Pei is an unexpected reversal of the monetary policy stance, which is currently centred around monetary easing, consumption stimulus and being capital friendly.

Therefore, Townsend stressed that investors will need to keep an eye on the ‘Third Plenum’ in July 2024.

He explained: “In addition to further supportive measures for the property market, the structural reform agendas – traditionally a focal point of the ‘Third Plenum’ – are worth watching as they may be necessary in navigating both cyclical headwinds and demographic challenges.

“A key risk could be that if the communication disappoints the market, in the sense that investors begin to feel that the government is starting to turn its attention to focussing on things other than the economy, there may be something of a pull back.”

Nonetheless, GQG Partners’ investment team believes that things are unlikely to get meaningfully worse from here for China.

“There is a bevy of earnings coming out of some of the largest weights in the benchmark and in our view, earnings remain like gravity and it will be individual company execution rather than macro noise that will ultimately drive the attractiveness of select Chinese equities,” GQG analysts concluded.

Nonetheless, the GQG Partners Emerging Markets Equity fund is structurally underweight Chinese equities due to their lack of durable earnings growth, heightened geopolitical risk and better opportunities elsewhere.

Market volatility paves the way for investors to buy solid businesses at attractive prices.

Even following the market pullback in April, risk appetites have remained largely intact thus far in 2024, even as the potential trajectory of interest rates has grown increasingly murky. Persistently sticky inflation readings and more-recent signs of economic weakness have markets reconsidering how many federal funds rate cuts will happen this year – or if any will happen at all.

Evolving interest rate expectations have been a prime driver of risk assets thus far in 2024, as they were in 2023. While confidence in a potential US Federal Reserve pivot fuelled rallies across a range of risk assets beginning in late 2023, ‘higher for longer’ has re-emerged as the dominant policy narrative in 2024 as macroeconomic readings have tempered expectations around the timing and magnitude of federal funds rate cuts.

Swaps traders entered the year expecting six cuts totalling 1.5 percentage points during 2024 but now see only one 0.25% cut.

While the enthusiasm for risk assets that emerged toward the end of 2023 persisted through the first quarter of 2024 – especially for large-cap growth names – year-to-date to 30 April, the Russell 2000 Value Index is down 3.7%, lagging the 0.7% loss for its growth analogue and the 6.0% gain for the S&P 500 Index.

Yet even with dampened expectations for rate cuts, signs of market complacency remain widespread. Measures of implied equity market volatility have subsided after an April spike and tight credit spreads, upbeat corporate earnings forecasts and rich multiples for some stocks suggest optimism.

Potential for choppiness

Despite generally resilient equity markets, we believe there are reasons to be wary in the current environment. Tight labour markets and wage growth may trigger still higher inflation ahead and rates that remain higher for longer can be challenging for smaller companies with relatively limited access to capital.

The tight-money environment can also dampen merger and acquisition (M&A) activity by private equity vehicles, historically a source of support for small-cap valuations.

Beyond monetary policy, the escalation of geopolitical risks or unforeseen local political developments – there are federal elections scheduled for more than 70 countries in 2024 – could upend positive market momentum with little advance warning.

Meanwhile, massive swells of public debt in most developed economies combined with a general lack of fiscal discipline have the potential to spark a sudden and painful reconsideration of risk premia.

Relying on investment discipline, not Fed policy

In the small-cap space, volatility may provide us with the opportunity to acquire fundamentally solid companies at valuations that may be distorted by cyclical forces.

There are a number of ways in which US-based smaller companies could receive a boost from a Fed rate cut, from greater operational and financial flexibility to an uptick in M&A activity – but even so, none of our investments are based on the assumption that a much-desired central bank pivot will come to pass.

Regardless of the Fed’s actions, it seems likely that small companies that are cheap for a reason will continue to face a challenging operating environment, while many of those with solid businesses and catalysts for improvement may progress toward fuller valuations.

By controlling what we pay for these assets, we seek to construct a portfolio that is a little cheaper than the market on a valuation basis while being well-positioned for strong upside should our investment theses play out.

Prospects for revaluation

At the end of the day, investors can control only which stocks they buy and how much they pay for them. They make these choices without knowing what the economy is going to look like down the road, the policies that will be implemented, the trajectory of interest rates or the direction of oil prices. All these factors are unknown, so investors make one real choice only – what to buy and how much to pay. If this decision proves wise, they stand to be rewarded.

We believe those who devote their efforts to identifying and investing in good businesses at attractive valuations may see the most success over the long run.

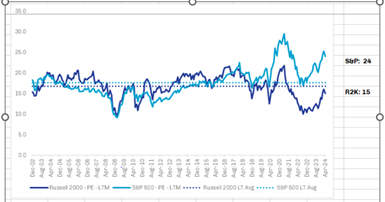

Even following strong gains over the past year, US small-cap valuations continue to suggest an environment with available opportunities. The Russell 2000 Index trades at more than a 10% discount to its historical average and a 38% discount to the S&P 500 Index.

As the chart below shows, a discount for small-cap stocks is a relatively recent phenomenon. For most of the period between 2003 and 2017, small-caps traded at a premium to large-caps, and depressed small-cap valuations have historically been followed by rallies.

Trailing price-to-earnings multiples of US small-caps vs S&P 500

Source: FactSet, data as of 30 Apr 2024

Even within an overall valuation discount for small-caps, however, selectivity remains key. Given that 44% of the companies in the Russell 2000 were unprofitable as of March 31, 2024 – versus only 7% of the S&P 500 – we think sorting the wheat from the chaff is a worthwhile endeavour in the broad and diverse small-cap universe.

As Warren Buffett (quoting Benjamin Graham) once said, a “wildly fluctuating market means that irrationally low prices will periodically be attached to solid businesses”. Smaller companies are one of those markets and we believe that their volatility and inefficiency create opportunities for active managers to potentially generate alpha, more so than any other equity asset class, as the table below shows.

Active manager success rate versus index

Source: Morningstar, data as of 30 Apr 2024

Navigating uncertainty ahead

Our focus going forward remains on separating strong businesses from those that are cheap for a reason. With the US in an election year, small businesses may have concerns about the regulatory burden, government spending and debt levels, and how these might affect interest rates.

The Fed’s success rate in its previous attempts to engineer a soft landing is an obvious reminder that uncertainty persists, and conditions are likely to become more challenging as the accumulated impacts of policy tightening continue to mount, especially among smaller companies with more limited access to capital.

In the face of these challenges and concerns, our focus remains on separating strong businesses from those that are cheap for a reason. With catalysts for growth or improvement, we look for sound businesses that may be positioned for solid returns.

Bill Hench is head of the small-cap team at First Eagle Investments. The views expressed above should not be taken as investment advice.

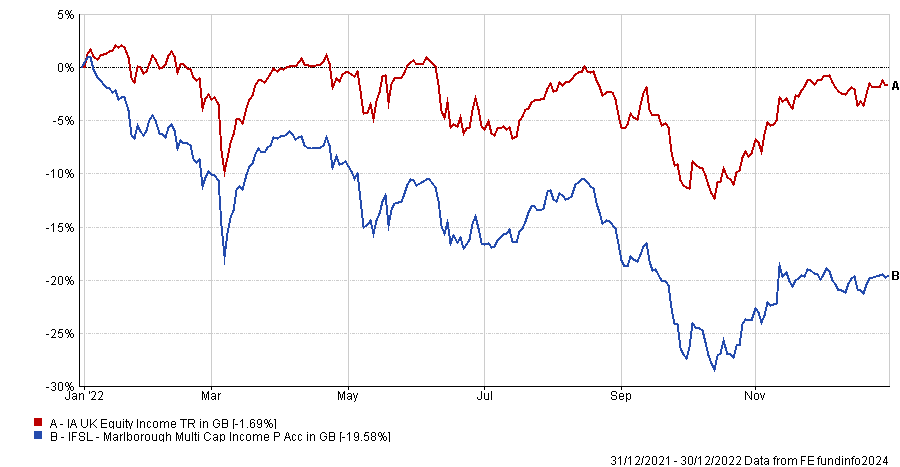

Performance has picked up recently and the IFSL Marlborough Multi Cap Income fund remains ahead since launch, but a poor 2022 has impacted long-term returns.

Sometimes good managers have a bad year that can derail their performance figures for years to come. For Siddarth Chand Lall, manager of the £465m IFSL Marlborough Multi Cap Income fund, that time was 2022.

The year was so poor that it has impacted the fund’s medium and long-term figures, with the portfolio sitting in the fourth quartile of the IA UK Equity Income sector over three, five and 10 years. It remains ahead of the sector average since launch in July 2011, however.

In the decade prior to 2022, the fund was the fourth-best among its 60 peers, smashing its average rival by more than 70 percentage points, as the below chart shows.

Performance of fund vs sector from 2012-2022

Source: FE Analytics

“The performance was top quartile over one, three five and 10 years up until the end of 2021; 2022 was the year that we struggled,” said Chand Lall.

“That is what has spoiled the three and five-year numbers. It isn’t that we have had bad performance every year.”

His fund tends to invest mainly in mid- and small-caps, with some 83.6% of the portfolio invested in this area of the market, while just 10.3% is in larger stocks.

As a result, the fund was buffeted from all sides, including the UK macroeconomic picture worsening due to rampant inflation, which had a particularly big impact on the more domestically-focused mid-cap stocks.

Couple this with a weaker pound (making imports more expensive) and the situation for the lower end of the market was difficult.

As such, his fund lost some 19.6% in 2022 alone – the worst year on record for the fund since its launch in 2011 – with the manager also noting there were some stock-specific issues as well.

Performance of fund vs sector in 2022

Source: FE Analytics

Yet the name of his fund is multi-cap, suggesting he has the option to move up the scale where appropriate – something Chand Lall admits was a lesson he learned during the course of that difficult year.

“How would we have positioned if we had known now what we knew then? We would have made much more use of the large-cap allocation. Whereas it’s almost always been between 5% and 15% to the FTSE 100 we would probably have moved up the scale,” he said.

However, it was not as easy, he noted, due to the makeup of the investors in the fund. “At the time there were specific clients who wanted us to keep the small-cap and mid-cap bias the way it was because we made up a portion of their allocation across many portfolios,” Chand Lall said.

“We were told ‘if you do underperform at least we know why you are, what we don’t want is for you to double up on where we already have exposure through other funds’.”

This is no longer an issue for the manager as these clients are no longer invested in the fund and so he has “much more flexibility” in the future should the environment change as dramatically as it did in 2022 when inflation and interest rates rose steeply.

“We will move much larger without changing the investment process,” he said, which includes looking for good companies with strong balance sheets indicated by metrics such as net debt to net assets of sub 50% (or preferably net cash) and free cashflow covering the dividends.

Chand Lall added: “In the event we get a scenario where there is potentially high inflation and interest rates, we would take advantage of the flexibility the strategy allows. That is the learning. I don’t mean 60% of the fund would be invested in the FTSE 100, but instead of 10-15% it might be 30-35%.”

Yet to change the portfolio now would be “silly”, he argued as mid- and small-caps are coming into their own. Indeed, the fund has been one of the top performers of the IA UK Equity Income sector so far in 2024 and since its nadir in October 2023 it is up some 28%.

Performance of fund vs sector over 1yr

Source: FE Analytics

“At this current juncture it would, to a certain extent, be almost silly to do it [move into large-caps]. We are getting so much alpha at this moment so I wouldn’t want to move away from that just to buy large-cap for the sake of it,” he said.

This recovery is in-keeping with previous periods, he noted, such as following the Brexit referendum in 2016 and the Covid pandemic collapse of 2020.

“What’s driving that is the aspect of beaten up valuations and also stocks trading better. We have gone past that element of caution and worries over a recession in the UK GDP figures. In the latest quarter it was 0.6% which was better than expected,” he said.

“That macro aspect does have some correlation with your micro. Also companies are trading better – we have had more good updates than bad. The multiple expansion will come.”

GAM Investments’ head of global growth equities, two fund managers and an analyst have joined Liontrust Asset Management.

Liontrust Asset Management has established a new global equity group and brought in a team from GAM Investments to lead it. Mark Hawtin, who headed up GAM’s global growth equity team and managed long-only and long/short strategies, will run the new division. He will be joined at Liontrust by three GAM colleagues: investment managers David Goodman and Kevin Kruczynski, and analyst Pieran Maru.

Hawtin and Goodman are bringing their GAM Star Alpha Technology fund with them to Liontrust and have been appointed sub-investment managers of the strategy until the portfolio officially changes hands.

Ewan Thompson, Tom Smith and Ruth Chambers, who currently manage emerging markets and Japanese equity funds at Liontrust, will move internally into Hawtin’s group. All three joined Liontrust when it acquired Neptune Investment Management in October 2019.

The new global equity team will manage the Liontrust Balanced fund and the Liontrust Global Alpha fund, along with other global and regional equity funds.

This move follows Liontrust’s attempt to buy GAM last year, which collapsed when shareholders rejected the deal.

Hawtin has 40 years of investment experience. Before joining GAM in 2008, he was a partner and portfolio manager at Marshall Wace Asset Management, running one of Europe’s largest technology, media and telecoms hedge funds.

Hawtin said: “We are really excited to have joined Liontrust as it is in the process of building a strong global equity platform. We look forward to extending the product offering at a time when the global equity opportunity is so great.

“My experience of running global funds at Marshall Wace and then GAM has allowed me to see markets through many different cycles. This knowledge will serve us well as we navigate a period marked by unprecedented levels of change caused by structural disruption as well as geopolitical uncertainty.”

Hawtin believes that, to succeed, companies must adapt their business models rapidly in response to threats that challenge the traditional world order. This dynamic should create opportunities for active managers due to the polarisation between the winners who adapt and the losers who do not, according to Liontrust.

GAM hired Paul Markham in February to replace Hawtin at the helm of its global growth equities and disruptive growth teams. He was previously head of global opportunities equities at Newton Investment Management.

Experts pick European equity funds poised to profit from looser monetary policy.

The European Central Bank (ECB) will, in all likelihood, cut interest rates next week, becoming the first major central bank to ease its monetary policy.

This move is likely to support European equities, which have suffered from the poor economic outlook for the continent as a result of the Russian invasion of Ukraine, spiralling energy costs and a slowdown in global manufacturing.

Tom Stevenson, investment director at Fidelity International, said: “Many of the headwinds for Europe are now turning into tailwinds. Inflation has fallen back rapidly towards the ECB’s target. This will enable the central bank to lead the way when it comes to interest rate cuts this summer. Monetary policy is now pulling in the same direction as supportive fiscal policy.

“Against this improving backdrop, European shares are not expensive. They trade at a significant valuation discount to their US peers. Any shift away from Wall Street could benefit Europe.”

Below, experts suggest funds that investors may want to consider to benefit from the upcoming ECB rate cuts.

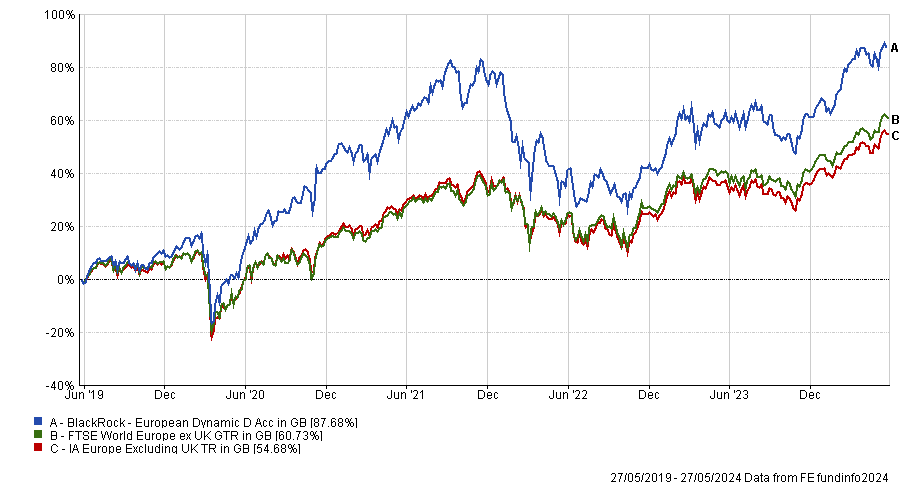

BlackRock European Dynamic

Amaya Assan, head of fund origination at Square Mile Investment Consulting and Research, recommended BlackRock European Dynamic.

This fund’s unconstrained approach enables FE fundinfo Alpha Manager Giles Rothbarth to adjust the portfolio strategically, taking advantage of the current economic backdrop and the opportunities it offers.

Performance of fund over 5yrs vs sector and benchmark

Source: FE Analytics

Assan said: “Given the flexible approach employed by the manager, the portfolio is currently tilted to be overweight cyclicality which should be a beneficiary of a falling interest rate environment.

“The manager has identified areas such as construction, where volumes are recovering from their worst levels in over a decade and share prices are likely to benefit from falling rates, having been hit hard in the prior rising interest rate environment.”

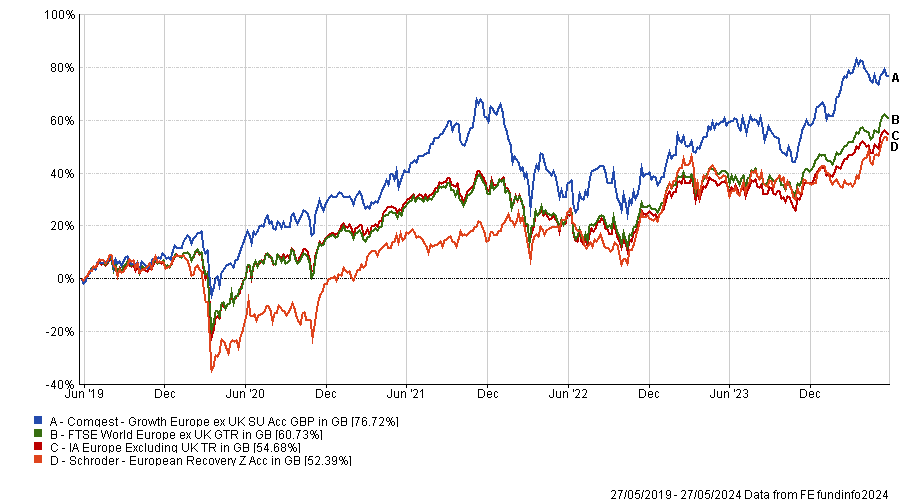

Comgest Growth Europe ex UK and Schroder European Recovery

Tom Stevenson proposed two options for investors: a fund focusing on growth and another one following a contrarian approach.

For growth, Stevenson pointed to Comgest Growth Europe ex UK, which has a quality bias and boasts some well-known names among its top 10 holdings such as Novo Nordisk and LVMH.

“The managers look for companies with established brands or unique products or technology,” he explained.

Performance of funds over 5yrs vs sector and benchmark

Source: FE Analytics

Schroder European Recovery takes a different approach, as the managers invest in companies they believe to be undervalued relative to their long-term earnings potential. Current holdings include the likes of Sanofi, BNP Paribas and Allianz.

Premier Miton European Opportunities

Small- and mid-cap stocks are theoretically more sensitive to changes in interest rates and should, therefore, particularly benefit from the ECB rate cut.

As a result, Sheridan Admans, head of fund selection at TILLIT, highlighted Premier Miton European Opportunities, managed by FE fundinfo Alpha Managers Carlos Moreno and Thomas Brown as well as Russell Champion. The fund offers exposure to European mid-caps with high-quality growth characteristics, he said.

Performance of fund over 5yrs vs sector and benchmark

Source: FE Analytics

“The managers particularly look for companies with high returns on capital. They believe this is a key metric determining quality, sustainable returns and long-term growth. This fund has a clear focus on stocks that can deliver long-term compound growth,” Admans explained.

“The team is lean and the managers are involved in every aspect from idea generation and research to decision-making.”

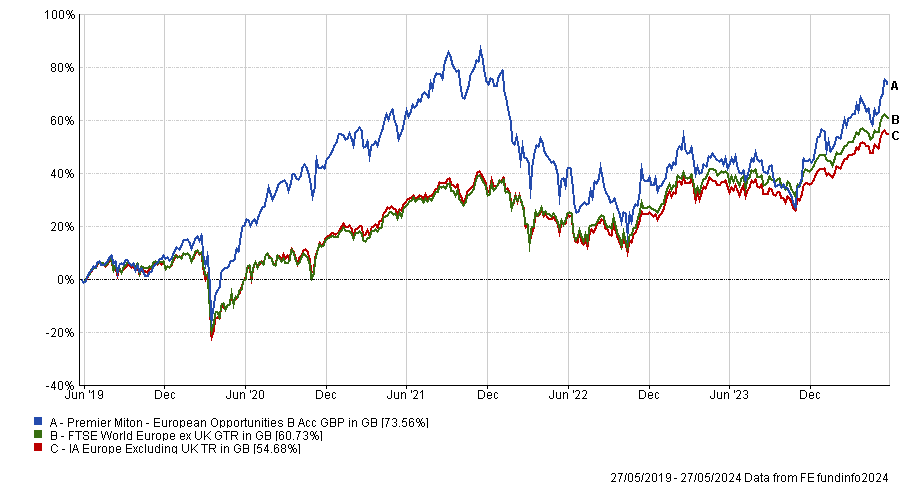

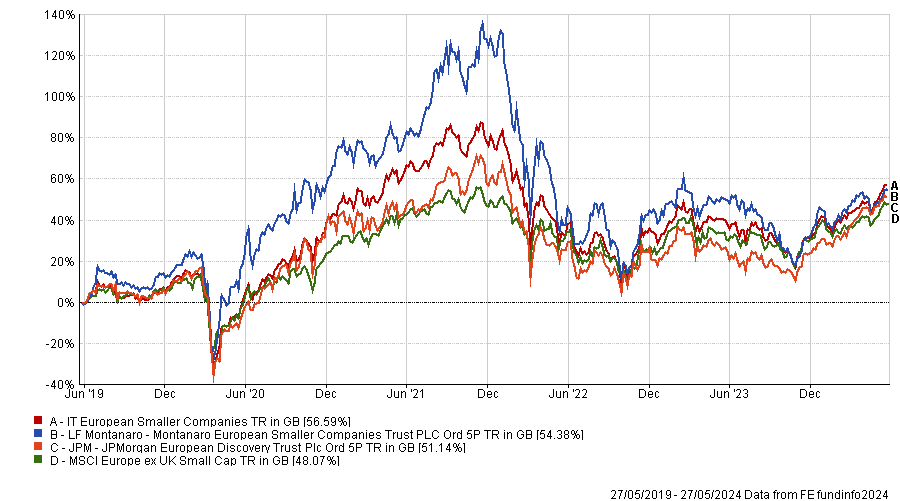

Montanaro European Smaller Companies Trust and JPMorgan European Discovery Trust

For investors comfortable with exploring opportunities lower down the market capitalisation scale, Admans also suggested Montanaro European Smaller Companies Trust.

“The managers are small company specialists and run a fairly concentrated portfolio with a quality growth, bottom-up investment approach,” he said.

Admans also highlighted the focus on environmental, social and governance (ESG) factors in the trust’s investment process.

Performance of investment trusts over 5yrs vs sector and benchmark

Source: FE Analytics

Alternatively, investors could consider JPMorgan European Discovery Trust, which was tipped by Billy Ewins, fund research analyst at Quilter Cheviot, for its “solid, well-resourced team”, enhanced by JPMorgan Asset Management’s “strong research capabilities”.

Ewins said: “The trust is a differentiated offering and unique to other funds, many of which tend to bias to larger companies today.

“However, just because it is a small-cap investment trust, does not mean it doesn’t have exposure to leading brands, with several of the companies having a strong consumer presence, such as Italian coffee machine manufacturer DeLonghi.

“Crucially, however, the trust is well diversified and has exposure to other exciting business areas which are less reliant on the consumer, including geosciences in the shape of Dutch company Fugro.”

US tech is now within income investors’ grasp, says Alpha Manager Saldanha

What can you do with $80bn leftover cash? Admittedly, it’s a nice problem to have, but the answer wasn’t a straightforward one for Google parent Alphabet, which sat on the cash for a while before deciding only this year to pay its first dividend.

What took it so long? That’s what Richard Saldanha, FE fundinfo Alpha Manager of the Aviva Global Equity Income fund, asked.

“After all its funding was done, including the capital expenditure programme Alphabet was sitting on $80bn after. In some ways, you could ask: What took it so long to paying it out as a dividend?,” he said.

But while this is an interesting development for income investors, who now gain access to a whole new set of income opportunities in US technology, the manager was more excited about the broader trend and the growth potential, rather than the dividend itself.

While this might look like a sizable amount in terms of dollars, the yield percentage is not going to set the pulse racing, at just about 0.5%. However, cash isn’t only accumulating on Alphabet’s books, but also across the industry and Saldanha sees only one direction that this trend could go.

“This opens up a new opportunity set and we expect this trend to continue,” he said. “Don't be surprised if you see more and more of these technology companies initiating dividends. Tech is a sector that now is very much within income investors’ grasp.”

Until now, the options for income investors were limited to Microsoft, which has been paying dividends for a long time and “has a very mature dividend framework”.

Like with the others, it isn’t the nominal yield that’s interesting in Microsoft’s case, but the growth profile.

“The underlying growth of these companies is quite interesting. We expect their dividend to grow in line with the cash flows. For Microsoft it's been consistently double-digits,” Saldanha said.

Microsoft historical dividend growth

Source: Company filings

Whether there will be a large uptake of US tech within income portfolios is still to be seen and will depend on managers’ considerations around valuation and yield, but Saldanha has no doubt many funds will be increasingly looking at this sector.

“It's going to be interesting to see how that progresses. For us, it’s going to be a steady evolution,” he said.

The only large tech company currently in the Aviva Global Equity Income portfolio is Microsoft, but Alphabet is held in another fund managed by Saldanha, Aviva Global Equity Endurance and was described by the manager as the most convincing stock among the Magnificent Seven.

“Alphabet is a very strong company that is going to grow cash flows at a at a healthy rate, so it is certainly of interest now for the equity income fund too,” he said.

“For now, however, this fund gets its tech exposure via Microsoft and other routes in the supply chain. We've been very much invested in the semiconductor space, for example, where companies have much more mature dividend structures.”

Examples of these are the artificial intelligence chips suppliers Broadcom, which sells to Alphabet, and TSMC, which manufactures the chips for Nvidia.

“We're very pleased however to see this opportunity set continue to evolve and increase,” the manager concluded.

Performance of fund against sector and index over 1yr

Source: FE Analytics

We expect high single-digit earnings growth in the future from the asset class, with the potential for upside should current trends accelerate.

The surge in investor focus on generative artificial intelligence (AI) has led to one of the most powerful rallies in technology stocks in recent memory.

In our view, generative AI has the potential to be a game changer not only in our everyday lives but also in the growth profiles of the infrastructure supporting it. We are currently seeing strong pricing power for data centre owners, accelerating load growth for public utilities, and increased demand for renewable developers and low-carbon portfolios to provide clean energy to support data centre assets.

This generative AI-related growth comes in addition to infrastructure’s broader secular underpinnings, which include the demands for global decarbonisation, energy security and modernised assets.

Infrastructure’s irreplaceable role in AI

Current data centre capacity, ramping power/cooling needs and access to power for new-build data centre assets are bottlenecks to generative AI-related growth. Today, high occupancies of data centres are already spurring pricing power and margin improvements for existing essential assets in those listed companies.

For example, vacancy rates are at a decade-low across North American markets, while 2023 data centre leasing activity is likely to have doubled 2022 levels and finish eight times above what was recorded in 2019.

Power use at existing facilities is also on the rise, as it is estimated that generative AI requires 20-100 times more power compared to data centre usage prior. For example, a generative AI purpose-built data centre requires a minimum of 250MW of capacity, compared to a historical data centre capacity size of circa 10MW.

While power use is increasing, transmission grids are unprepared and new investment is required to support generation connections. Generative AI-related demand in the power grid is expected to grow at a 30% compound annual growth rate (CAGR) over the next five years, with some estimates coming in as high as 70%.

In response to this phenomenon, major listed utilities are multiplying their forecasts for electricity demand growth. Industry-wide, current levels of anticipated power growth for the next five years double expectations as of 2022 and are more than 9 times the long-run average.

Increased load growth represents a paradigm shift for US utilities, with the potential to enhance earnings, increase required investment and further improve long-term earnings visibility.

In addition, the draw for low-carbon generation from generative AI and its data centres is immense; it is spurred by data centre developers prioritising green power to minimise carbon footprints in the face of unprecedented growth.

In fact, renewable power purchase agreements (PPAs) from Amazon, Google, Meta and Microsoft have ramped up by 6 times compared with 2018 levels, and the development backlog for leading listed renewable energy developers is currently dominated by data centre-related projects. By 2025, generative AI-led PPAs could reach levels equal to half of the current market.

Secular growth at a discount

Given the secular growth potential of infrastructure, valuations remain at a discount today. We expect high single-digit earnings growth in the future from the asset class, with the potential for upside should current trends accelerate.

Following a historic lag to large-cap tech and broader equities last year, as well as recent underperformance to private equity infrastructure indices, infrastructure’s price for its growth is compelling.

On a 2025 price/earnings to growth ratio (PEG ratio) we see listed infrastructure potentially trading at a 1.5x multiple for 2025, compared to 2x for the ‘Magnificent 7’.

On a relative valuation basis, infrastructure is at a 10% discount to global equities, compared to its history of a 10% premium. When we further consider the private market and analyse notable large-scale privatisations over the past five years, we see listed infrastructure trading at a 30% discount to private equity acquisitions.

Jeremy Anagnos is portfolio manager of Nordea’s Global Listed Infrastructure strategy. The views expressed above should not be taken as investment advice.

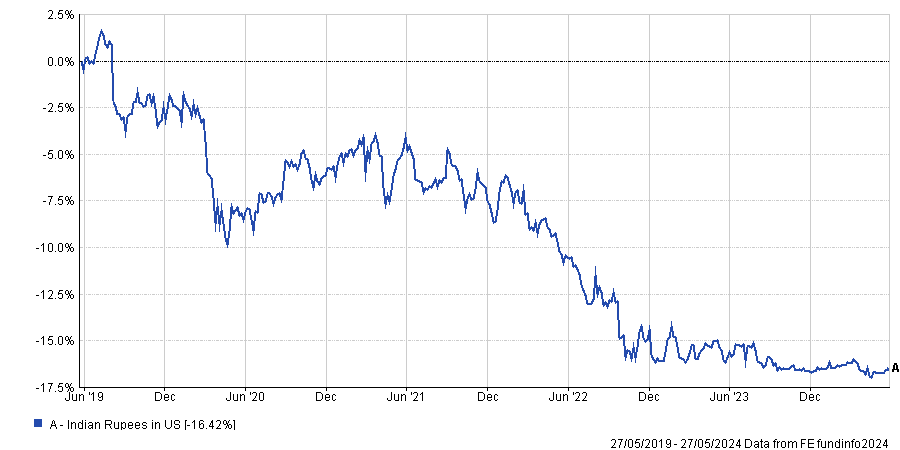

Currency risk takes a bite when investing in India, says India Capital Growth’s Narain.

Investing in emerging markets has always meant taking on more risk, whether it be from geopolitics, different economies or currencies.

That’s also true for India, where perceived geopolitical risks include the outcome of the ongoing elections, its relationship with Russia and environmental, sustainability and governance (ESG) issues.

At the same time investors also need to think about currency, according to Gaurav Narain, manager of the India Capital Growth trust, who said they must be willing to take an average hit of 2% to 3% every year before they can break even.

The Indian Rupee has been volatile in recent years. Over 12 months it is 4% lower against the pound while over five years this rises to 17%.

Against the dollar the figures are comparable. Over one year the Rupee is just 0.7% weaker, but this climbs to 16.4% over five years and 29% over 10 years. And this depreciation might not be reversing any time soon, although it should slow down.

Rupee versus US dollar over the past 5 years

Source: FE Analytics

“Historically, the currency has depreciated between 3% to 3.5% on average every year over the past five, 10 and15 years against the dollar”, Narain said. “But my own sense is that now it will be slightly less, around 2% to 3%.”

There are three main reasons why the manager is expecting a lower depreciation trend going forward.

Firstly, the export of services is now worth $340bn and also growing at a much faster pace than before. Secondly, India is getting a lot of forex reserves in the form of remittances, last year that amounted to about $110bn. And thirdly, India is attracting a lot of foreign direct investment, almost $60-$70bn a year.

“In particular, the result of the forex reserves are very strong and provides a lot of cushion on the currency. In volatile times, the Reserve Bank of India has a lot of flexibility, so you shouldn’t see the big swings that have historically happened,” explained the manager.

“The currency has been remarkably stable against the dollar and the country is in a much better position. But if you're investing in India you must account for that 2%-3% hit.”

The other risk that has been very present on investors’ minds recently is the election, with results to be announced next week. The current prime minister Narendra Modi is expected to maintain his majority, which is good news for investors, as he is “very good for the market”, according to Narain.

“He is doing all the right things for the economy. He’s thinking long term, trying to eliminate corruption and is very strong on execution, so he's genuinely good for the economy,” he said.

On top of that, has been doing an “incredible balancing act” on the international arena, remaining friendly with the Western world while still purchasing oil from Russia.

“India is among the top-three oil purchasers in the world, mainly from the Middle East and the US, but also Russia. Imagine what would happen to oil prices if the country stopped buying from Russia,” Narain said.

While Modi is the favourite candidate, election results are hard to predict. If he loses his majority, the market will “definitely correct”, said Narain, at least in the short term, because of the uncertainty.

“But then it all boils down to what the new government does on policies,” he said. “India is a democracy and has policy continuity, you don't see someone come in and change policies completely. Which is why India over the last two decades has grown at 10% in nominal GDP in dollar terms.”

Another potential issue for investors is that the market is trading on particularly high multiples, given the substantial growth that’s recognised and already priced in by the market.

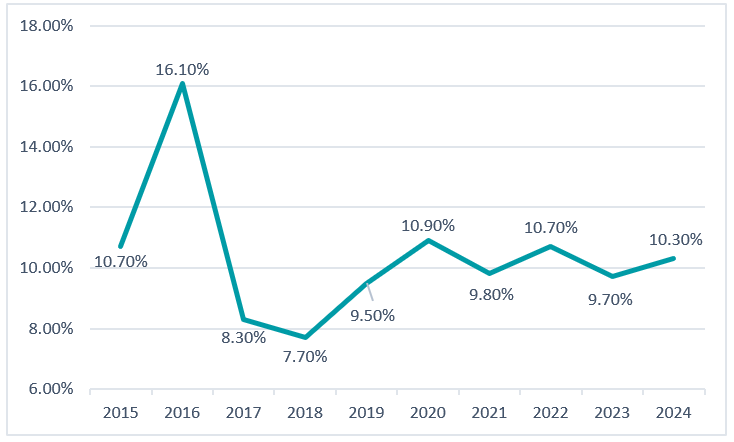

The average IA India fund has grown by 9.5% so far this year and the country has delivered strong returns for much of the past decade.

Performance of indices over the past 12 months and 10 years

Source: FE Analytics

The India Capital Growth fund has been tops amongst its IT India/Indian Subcontinent peers over the past 10 years. It mainly focuses on mid- and small-caps, which make up 38% and 50% of the portfolio, respectively.

Fund managers explain why defence stocks could move even higher and how they are playing this theme.

Some investors have shunned the defence sector, considering it to be incompatible with their environmental, social and governance (ESG) principles. Yet it has been brought back to the fore following the outbreak of the war in Ukraine and conflict in the Middle East.

Purely from a stock market perspective, investors who ignored defence stocks have incurred a significant opportunity cost, as the sector has performed exceptionally well over the past three years, especially in Europe.

Performance of indices over 3 years

Source: FE Analytics

After such a strong show of force, the question for investors now is whether defence stocks will continue to push forward.

Graeme Bencke, co-manager of Amati Global Innovation, believes defence stocks have the potential to go higher from here, but said the initial wave is already behind us.

“Many of these companies traded on quite low valuations in the past as defence spending had stagnated, but multiples have expanded with the increase in demand as geopolitical tensions have increased,” he explained.

“This re-rating process drove the sharp rise in share prices, and price development from here will be more reliant on revenue and earnings growth.”

David Coombs, head of multi-asset at Rathbones, agreed and sees some additional tailwinds which could drive long-term returns in the years ahead.

He said: “The doctrine and needs of militaries are changing rapidly because of technological advances and the new fronts they open up. New threats require new solutions, and while large defence contractors are mostly known for the big machines they have produced in the past, a much more meaningful part of their business is now focused on cybersecurity and digital warfare.

“A kicker to this need for military investment is the potential for Donald Trump to win a second term as US President and the war in Ukraine, which both seem likely to push European members of NATO to spend more on defence.”

Alec Cutler, manager of Orbis Global Balanced, went a step further, as he believes that whoever wins the US election this autumn, the US protection guarantee is gone, which means Europe will need to ramp up its defence spending anyway.

How are managers playing the defence theme?

Defence is a broad industry made of a wide range of distinct segments. Therefore, Bencke stressed the importance of focusing on areas where spending is most likely to grow over the coming decades.

He said: “While military spending is somewhat opaque, most governments produce defence strategy-related papers outlining the direction of travel for investment.

“Outside of specific large programmes, like the US 30-year submarine fleet renewal or the 'Future Long Range Assault Aircraft' replacing the Blackhawk helicopter, there are some clear areas of attention. Most of these make intuitive sense when we think about the potential threats. Better anti-aircraft and missile defences, counter-drone weapons, improved battlefield communication and control, for example.

“However, some others are perhaps less obvious but also seeing considerable growth in funding. The nature of conflicts between powers has changed over the past decade with a much greater threat from cyber-espionage and cyber-attacks on military and civilian infrastructure. Improved intelligence gathering and secure communications means increased spending on space-based initiatives, although much of this is classified.”

As a result, Bencke holds MOOG – a provider of highly accurate electric actuators and bearing systems – which he believes is poised to benefit from space, aircraft and missile-related spending.

He also pointed to Leonardo DRS, which should profit from mobile air defence spending through its M-SHORAD platform, as well as providing new electric propulsion systems for the navy.

Another stock Bencke highlighted is technology consultancy firm Booz Allen Hamilton, which is involved in cyber defence and also assists developments with US agencies such as the CIA and FBI.

Jacob de Tusch-Lec, co-manager of Artemis Global Income, finds European defence companies attractive in spite of their recent strong performance, as Europe still has plenty of catching up to do.

“Defence is like insurance. You don’t like paying it until you need to make a claim. Since 1992 and the collapse of the Soviet Union, the world has enjoyed a massive peace dividend and the benefits of globalisation. With that has come a huge under-investment in defence," he said.

“If you look at Europe today versus 30 years ago, we’ve got fewer than 4,500 tanks compared with nearly 19,000 then. You can’t build 15 thousand tanks in a few weeks. We’ve also got half the ground attack aircraft and submarines we once had. On top of this, a lot of materials have been sent to Ukraine.”

Therefore, de Tusch Lec is bullish on Düsseldorf-based Rheinmetall, which he expects will benefit from a big demand inflection that might last for a decade.

He added: “It’s currently sitting on an order backlog of €38bn, that is five times the size of what it sells in a year. Replenishing munitions inventory is not going to happen overnight.”

Closer to home, Cutler likes BAE Systems and Rolls Royce. The former is well-positioned in warships, has content in many of the leading weapon systems such as the US stealth fighter jet F-35 and has a large share of US research and development contracts.

As for Rolls Royce, he believes it should benefit from long-term contracts, such as the one to supply new engines for the US B-52 aircraft fleet, providing the UK company with non-cyclical cash flows.

He also mentioned some defence companies in Asia, such as Mitsubishi Heavy in Japan, Hanwha Aerospace in Korea and Hindustan Aeronautics in India, because tensions are also heating up in that part of the world.

Performance of stocks over 3yrs

Source: FE Analytics

As for Coombs, he has long owned US-listed Lockheed Martin and French defence and aerospace company Thales to “mitigate the risks of a more stressed geopolitical age”.

“Both Thales and Lockheed Martin have a comprehensive suite of cyber capabilities, supported by elements of artificial intelligence, machine learning and automation to deal with the complexities of today’s deployments,” he said.

“These technologies also have civil uses, beyond the military ones that drive their creation. For example, Lockheed Martin is using its artificial intelligence capabilities and hardware to support firefighters dealing with wildfires by connecting land, air and space-based sensor and monitoring, which help predict and mitigate the spread of wildfires.”

Are defence stocks compatible with ESG?

The rapid increase in geopolitical tensions and the ensuing need for higher military spending have sparked debate on whether defence stocks are compatible with ESG principles.

For Bencke, while warfare is “abhorrent and anachronistic”, it nevertheless remains a reality.

“Sadly, the words of the Roman general Vegetius are as true today as when uttered over 1600 years ago – ‘if you want peace, prepare for war’,” he said.

“We would not endorse or invest in weapons or practices which breach modern conventions on warfare, but sadly the industry remains important for the defence of our democratic way of life.”

De Tusch-Lec agreed, adding that the legacy of the war in Ukraine is that individual countries need to revisit their priorities.

He said: “Nations are having to think about those areas at the bottom of Maslow’s pyramid of needs – the essentials in life like food, water and security. From that perspective, defence stocks are compatible with ESG and as investors we obviously avoid those companies which have links to cluster bombs or land mines.”

However, Coombs does not believe defence stocks are compatible with ESG and Rathbones does not hold them in their sustainable multi-asset funds, in which ESG is more linked to values rather than financial risk.

Finally, Cutler believes that peace is an imperative starting point to implement ESG ideals, but that defence is a necessary evil to create those conditions.

He concluded: "Peace through strength is at the base level of a society's hierarchy of needs. Peace is a have-to-have, without which higher order desires relative to the environment, society and governance will never achieve sustained traction.”

It will be managed by the emerging companies team.

BlackRock has announced the launch of a new global smaller companies strategy, offering UK investors the opportunity to “capitalise on the high alpha potential within the smaller companies universe”.

Co-managed by Matt Betts and Dan Whitestone from the BlackRock’s emerging companies team, the fund follows a fundamentals-driven approach and invests in companies with defensible market positions, competitive products and structural growth drivers. It is benchmarked against the MSCI World Small Cap index.

According to the press release, active management is “key” for small-cap funds, particularly as dispersion of returns can be high in this under-researched universe.

Whitestone said: “As active managers, we believe small-cap stocks can present us with the most attractive hunting ground as these companies tend to operate in an inefficient, under-researched area of the market and can offer the potential to generate returns for our clients over the long term.”

Another advantage of smaller companies are their cheap valuations, Betts said, with small-caps now trading at the all-time-high discount to large-caps of approximately 26%; additionally, they are expected to provide sustainable returns in the long term too.

“Alongside the attractive valuation opportunity right now, we believe that small-cap funds can provide excellent long-term investment due to their historic outperformance compared to large-caps,” Betts said.

Finally, the investment team said interest rates coming down in 2024 will “act as a potential catalyst for investors to reappraise the valuation opportunity in both absolute and relative terms”.

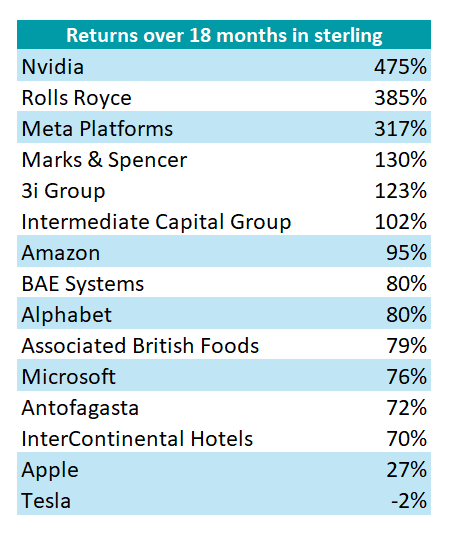

Rolls-Royce has outperformed six of the Magnificent Seven in the past 18 months, while M&S exceeded five of them.

The Magnificent Seven have dominated headlines, so it may come as a surprise that a handful of British companies have delivered returns close to, or even exceeding several of the American tech behemoths over the past 18 months, whilst trading on far lower multiples.

Rolls-Royce has returned 385% over 18 months, beating six of the Magnificent Seven (Nvidia being the exception) and outperforming Meta Platforms’ 317% rise in sterling terms.

Marks & Spencer, 3i Group and Intermediate Capital Group all exceeded Amazon, whose shares rose 95% in sterling terms over 18 months.

Associated British Foods and BAE Systems performed in line with Alphabet, while Antofagasta wasn’t far behind Microsoft.

Dan Coatsworth, investment analyst at AJ Bell, said: “Some 41 FTSE 100 stocks have delivered a better return over the past year and a half than Apple and 79 have beaten Tesla. That is proof that the UK market is alive and well and that strong returns are not restricted to the go-go-growth segment of the US stock market.”

Returns for well-known US and UK stocks over the past 18 months

Sources: AJ Bell and SharePad, data for 18 months to 23 May 2024, total returns in sterling

Imran Sattar, portfolio manager of the Edinburgh Investment Trust, agreed. “There is a perception that the UK market is essentially made up of low growth and lower quality businesses; we strongly disagree. It is possible to build a well-diversified portfolio of advantaged UK businesses with high returns and good growth prospects at a discounted valuation.”

Below, Trustnet explores why the UK’s strongest performing companies have done so well, highlighting the stocks that have beaten five of the Magnificent Seven over the past 18 months.

Rolls Royce

Rolls Royce is a turnaround story and its new chief executive Tufan Erginbilgic, who joined on 1 January 2023, deserves much of the credit for cutting costs and maximising profits.

Rolls Royce has also benefitted from the post-pandemic recovery in air traffic, said Stephen Anness, head of global equities at Invesco. “The resumption of international travel, as well as the management turnaround story beginning to take shape, meant it produced a total shareholder return of 221.6% for 2023, matching Nvidia.”

Coatsworth added: “The engineer continued to issue bullish trading updates and that fired up the share price.”

Marks & Spencer

M&S has beaten expectations multiple times in the past year, Coatsworth said. Earlier this month, the retailer announced strong full-year results, with a 33.8% increase in adjusted operating profit and a 9.4% increase in total sales. It also introduced a 3p dividend.

James Henderson, co-manager of the Henderson Opportunities Trust, Lowland Investment Company and Law Debenture, was an early convert. “We began adding to M&S early in its recovery, which has helped our funds as the bears have turned slowly bullish. Marks’ recent results were very good – much better than the best estimates by analysts,” he said.

M&S has generated strong cash flow, which has enabled it to reduce debt and start paying a dividend again, but now the retailer is embarking on the “next stage of the story”, he continued.

“It is now spending half a billion pounds on improving the offer – upgrading its stores and investing in the online infrastructure. After a period of rationalisation and store closures, this is the next phase and is essential if M&S is to continue its growth,” said Henderson.

3i Group

Nick Shenton, co-manager of the Artemis Income fund, said 3i Group has been the best performing stock in his portfolio over the past year. The £28.5bn investment company produced a total return of 85.5% in 2023 and has been “a tremendous performer over the very long run”.

Anness attributed 3i’s rapid growth to its stake in Action, Europe’s fastest-growing non-food discount retailer, heralding it as “one of the brightest companies on the continent”.

“The cashflow generation of this underlying company has been incredible: the payback period for each newly-opened store is roughly one year. Action currently has more than 2,300 stores and plans to open 400 a year by 2026. We think it could have a 20-year runway for further expansion in Europe alone,” he said.

Intermediate Capital Group

Intermediate Capital Group (ICG), which manages private equity, private debt and real assets funds, has enjoyed a strong 18 months and is one of Jefferies’ “top picks”, said equity analyst Julian Roberts. “We view ICG as a quality compounder with plenty of long-term potential.”

ICG released its results yesterday for the year ended 31 March 2024, surprising on the upside. “We believe new guidance of $55bn of fundraising over the next four years is likely to be taken well, and $13bn of funds raised in the past 12 months compares with $12.4bn expected by analysts,” Roberts said. This included client commitments of almost $1.5bn across three first-time funds.

The firm announced an 11% increase in its fee-earning assets under management to $70bn and a 16% increase in third-party fee income to £578m, well ahead of consensus expectations of £540m.

Associated British Foods

Associated British Foods has performed strongly as inflation cooled, with share buybacks providing further support.

Primark’s owner benefited from its conglomerate structure, Coatsworth said. “Its interests across retail, agriculture, grocery and food ingredients means risks are spread across different industries. When one segment is not doing so well, other parts of its business are there to pick up the slack, and we’ve seen that dynamic at work in recent years.”

BAE Systems

The defence sector was thrust into the spotlight by Russia’s invasion of Ukraine. With geopolitical tensions on the rise, governments around the world have been increasing their defence spending, which has driven a rally in BAE Systems’ shares.

Defence projects tend to be highly complex, involving multiple companies in different countries, said Jason Hollands, managing director of Bestinvest. This means that BAE Systems benefits from global rather than just domestic military expenditure.

Defence order books are multi-year in nature and therefore relatively insensitive to the economic cycle, he continued, which “makes defence ‘defensive’ from an investment perspective”.

GQG Partners has amassed $140bn in eight years and delivered sector-leading performance but the US firm is still relatively unknown in the UK and Europe.

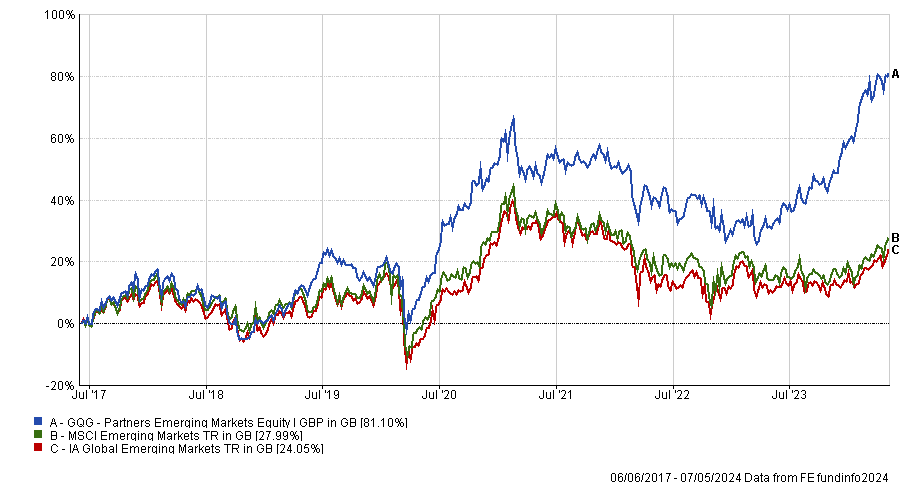

GQG Partners manages $140bn in global and regional equities and its flagship emerging markets fund is the best performer in its sector, yet the Florida-based firm is still relatively under the radar in the UK and Europe.

The $3bn GQG Partners Emerging Markets Equity fund is the top performing strategy in the IA Global Emerging Markets sector over one and five years and the sixth best performer over three years. It has left both its benchmark and sector in the dust since inception, as the chart below shows.

As such, its managers Rajiv Jain, Brian Kersmanc and Sudarshan Murthy have just won the FE fundinfo Alpha Manager of the Year award for Asia and emerging market equities. GQG’s global and US equity strategies were also nominated for awards.

Fund versus benchmark and sector since inception

Source: FE Analytics

One of the reasons for its stellar track record is GQG’s ability to spot risks, avoid the downside and, essentially, win by losing less. Here, GQG has a secret weapon: journalists, accountants and former private equity professionals.

The global equity manager has built a team of people with experience atypical of buyside analysts and charged them with identifying risks and patterns, and helping the firm to avoid groupthink. Their research dovetails with another team of more traditional stock-picking analysts.

Financial journalists were writing articles about issues in the US subprime mortgage market as early as 2006, which triggered GQG founder Jain’s interest in working with reporters and non-Wall Street professionals.

Chulantha De Silva, a client portfolio manager at GQG and former investment banker, said: “Wall Street does have a lot of smarts but it does have a herd mentality.”

Jain had a team of former journalists at his previous employer Vontobel, but expanded this function at GQG, which he established in June 2016, to include accountants, private equity specialists, technologists and healthcare experts.

“We have multiple different eyes from different vantage points on the same franchise,” De Silva said. He thinks following conventional wisdom is a huge problem in fund management and to outperform, managers need an “outside advantage”.

Accountants are adept at tracking patterns and can provide insights into the quality of companies’ management teams by studying corporate accounts. “Accounting is the language of business,” he observed.

Professionals with a background in private equity, meanwhile, can analyse the capital structures of companies.

“Tech folks double up as disruption specialists. The catalyst for that tool was to make sure none of our companies got ‘Amazoned’ out,” De Silva continued. With the advent of generative artificial intelligence (AI), “every stock in every sector is at risk of disruption”.

All of these “non-traditional folks” assist GQG with wealth preservation by identifying major risks to companies in the portfolio, so GQG can sell them before their share price tanks. “Every manager does a great job of buying stocks. Where most people falter is knowing when to get out,” he explained.

Another element of the firm’s sell discipline is that analysts and portfolio managers are afforded the flexibility to change their minds and challenge their own investment thesis. “At most firms you are frowned upon for changing your mind. At GQG you are incentivised to change your view on a stock,” he said. “We’d rather be found out wrong in a conference room at GQG than by the market.”

Another unconventional hiring strategy was to deliberately introduce a younger cohort three years ago – not junior analysts per se but young people specifically.

The Florida-based firm had always prided itself on its diversity (half of its staff were born outside the US and 40% are women) but one key area in which it was not diverse was age. As a result, no-one in the firm was using certain apps that have a younger audience. “How do you manage risk when you are not in the disruptive ecosystem?” he asked.