All three UK equity sectors are now among the highest returning of the year, Trustnet finds.

UK smaller companies funds have jumped to the top of the 2024 performance charts thanks to “sellers’ exhaustion”, a recovering economy and increasing mergers and acquisitions (M&A).

According to FE Analytics, the average fund in the IA UK Smaller Companies sector made a 10.8% total return over the first five months of 2024 – making it the highest-returning peer group.

The average smaller companies fund is even beating the IA Technology and Technology Innovations and IA North America sectors, which have been buoyed by the continued strength of the Magnificent Seven stocks.

The IA UK Equity Income and IA UK All Companies sectors hold fourth and fifth places year to date, with respective average returns of 8.5% and 8.1%.

Average return of Investment Association sectors over 2024 so far

Source: FinXL. Total return in sterling between 1 Jan and 31 May 2024.

This is a stark turnaround from earlier in the year, when the three UK equity sectors were much lower down in the performance tables, and is down to some strong returns from the UK in May.

Simon Evan‑Cook, fund manager on the VT Downing Fox multi-asset range, said: “The asset class has been so hated, and therefore heavily sold, that there are just fewer disillusioned souls left to sell them down.

“This is borne out by talking with our fund managers, who tell me that stock prices are no longer being eviscerated if the company reports slightly disappointing results. This had been the norm for the last few years, and this change in behaviour has the ring of sellers’ exhaustion to it.”

Source: FinXL

Rob Morgan, chief analyst at Charles Stanley Direct, added: “This rally has been a while coming. The area has long been cheap but what it lacked was a catalyst to break through persistent negative sentiment and reverse the flows out of UK assets that had been depressing share prices.”

He said a number of factors have combined to “tentatively” turn the performance of UK funds around, one of which is an improvement in the domestic economy. Although the UK’s economic numbers are “still not great”, they are better than many feared and support improving sentiment.

“When things seem very negative, a bit of good news goes a long way,” Morgan said.

He also pointed to positive trends at a company level. FTSE 100 companies with international-facing businesses have benefitted from the strength of the US dollar, which increases the sterling-dominated earnings and has led strong company results. Meanwhile, sectors such as energy, mining and defence, which are big constituents of the UK market, are benefiting from rising demand.

Snapshot of UK equity market over 2024 so far

Source: FinXL. Total return in sterling between 1 Jan and 31 May 2024.

Both Evan‑Cook and Morgan credited increased M&A as a positive for the UK. Years of underperformance from UK stocks has left them attractively valued when compared with international peers, leading to a series of approaches.

“In UK small-cap world it’s become common to hear the refrain ‘they’re so cheap that if you don’t buy them, somebody else will’,” Evan‑Cook said. “Turns out that was true, because all of a sudden corporate and private equity buyers are snapping up UK companies like it’s the end of an episode of The Apprentice.”

Morgan also argued that this creates a halo effect that bolsters sentiment towards the whole market, not just the target businesses themselves.

While all these factors are supportive of UK equities, they may have had a disproportionate impact on smaller companies.

“As the most undervalued parts of the market, UK small- and micro-caps have risen the most as sentiment has turned,” Morgan explained. “It’s also where liquidity is more limited so even a little bit of an uplift in interest can have a big impact.”

But whether the recent rally has legs is a more difficult question.

Morgan expects the M&A theme to continue to underpin valuations, but said it may not boost all stocks equally. Buyers such as private equity investors look for very specific characteristics in a target company, so the main beneficiaries would likely be active managers who are seeking the same qualities and who thereby end up owning natural M&A targets.

“Meanwhile, more extensive than expected interest rate cuts is a tide that would lift all the boats. Unfortunately, it isn’t that likely, but the gradual impact of lower interest rates further out should still help,” he finished.

“Finally, for UK small-caps the performance of the domestic economy is influential. Expectations are pretty low, so continued growth, albeit at a sedate pace, would create a benign environment.”

Retail investors in the UK continue to shun their domestic stock market despite its strong performance.

UK equity funds suffered their second-highest outflows on record in May, with domestic retail investors withdrawing £1.1bn despite strong performance since late February, according to the latest Calastone Fund Flow Index.

Calastone attributed these outflows to profit taking after the recent rally. Edward Glyn, head of global markets, said: “While buoyant markets usually attract new capital, many investors have seemingly chosen the UK rally as an opportunity to jump ship rather than a moment to reappraise the UK’s prospects.

“The election announcement made no difference to selling patterns during the month – this is a long-term trend of selling, not a news-driven flurry.”

On the other side of the Atlantic, US equity funds took in £826m in May, which was six times the long run average but one-third lower than April’s inflows.

Equity funds with environmental, social and governance (ESG) principles garnered £581m in May, with most of this money going to North American strategies.

“The heavy weighting of many US tech stocks in ESG funds helps explain why this is happening,” Glyn said.

“If we exclude North America, ESG-compliant funds have continued to suffer outflows in recent months. So what is going on? Investors can obviously buy funds that only invest in technology stocks though these are small in size, but they may be picking North American ESG-compliant funds as an alternative route to tech exposure.”

Global equity funds raked in £1.4bn and European equities attracted £462m in May.

Meanwhile, fixed income funds were hit by outflows for the first time since October 2023 as inflation data in the UK and US disappointed markets, rate cut expectations were pushed out further and bond yields remained high. Net outflows of £643m marked bond funds’ worst month since March 2020 and second-worst month during Calastone’s almost 10 years of data.

“The prospect of interest rate cuts in the US and the UK has receded yet again, with only the European Central Bank likely to move in the short term. Bond yields are approaching once more the post-global financial crisis highs they reached in late 2023, pushing down bond prices as they have climbed,” Glyn said.

“If you are confident rates will fall, then it’s possible to lock into these high yields for a very long time through fixed income funds, but the see-saw of hopes and fears over rates has finally led some investors to call time and withdraw capital for the first time in months, choosing instead to take refuge in cash or money markets.”

Indeed, investors moved £143m into safe-haven money market funds in May to access the relatively high yields on offer before central banks cut rates. Mixed-asset funds, however, suffered outflows of £531m.

The platform highlights stock market winners and losers from a potential Labour victory.

What impact the UK’s forthcoming general election will have on portfolios is a question that many investors are asking and AJ Bell investment analyst Dan Coatsworth has some answers.

Housebuilders, building materials suppliers, nuclear engineers and renewable energy specialists should perform well if the Labour party wins the election, while rail operators, outsourcing providers and UK oil and gas producers would flounder, he said.

Below, he addresses these sectors one by one, giving examples of companies whose activities complement Labour’s policies.

Industries and stocks that would prosper under Keir Starmer’s Labour

First up, housing. Coatsworth expect Labour to implement changes to the planning system and put greater emphasis on building affordable homes.

“This could be good news for companies involved in the provision of materials to the property sector and for housebuilders,” he said.

“Labour has pledged to upgrade draughty homes and help residents to stop wasting heat by it escaping into the great outdoors. That implies a boost for construction workers, engineers and electricians.”

There are multiple companies on the UK stock market that might benefit from Labour’s housing strategy, for example Travis Perkins, Wickes and B&Q/Screwfix-owner Kingfisher, all of which “could see higher demand from tradesmen and homeowners eager for the bits and bobs needed to spruce up flats and homes”.

But the list of companies that could get busier goes on to include construction groups such Morgan Sindall and Kier, ventilation specialist Volution and housebuilders, for example Vistry and MJ Gleeson.

Moving on to energy, where Labour’s Great British Energy initiative foresees the introduction of tougher measures on fossil fuel producers and a windfall tax on oil and gas projects to rack up £8.3bn. These proceeds will be directed towards wind, solar, hydrogen and carbon capture and storage technologies.

Some of the UK-focused oil and gas operators (such as Serica Energy and Harbour Energy) have already begun reducing their exposure to the UK North Sea, but others have doubled down on their exposure. Ithaca Energy, for instance, has purchased UK assets from Italy’s ENI.

Coatsworth highlighted specialists listed in the UK including Costain, which advises on energy transition work, and environmental services group Ricardo.

But an expected push for nuclear power would also play into Rolls-Royce’s strengths.

“Rolls-Royce has been among the best-performing shares on the UK stock market in recent years as investors bought into its recovery story,” he said.

“Being in a strong position to capitalise on small modular reactors looks like fortuitous timing for Rolls-Royce if Labour gets elected and could potentially act as another catalyst for its share price.”

Calls for the nationalisation of UK railways are creating a “major overhang” for FirstGroup, but ticket seller Trainline should come out of this situation intact, according to Coatsworth. The Labour party has said that it would not revive the Conservatives’ plan for a national retailing app for train tickets.

“Trainline’s shares have already experienced a wobble over potential changes to the UK rail system, but they’ve started to recover,” the analyst noted.

Industries and stocks unlikely to cheer for a Labour victory

Labour was responsible for the previous outsourcing boom and now it might be the architect of its demise, said Coatsworth.

“Starmer wants to bring public services back into government hands, suggesting that waste collection, cleaning, catering and maintenance services and more will no longer be a ripe opportunity for the UK’s army of outsourcing specialists,” he added.

“A lot of people think Conservative politicians awarded lucrative contracts to their friends and associates, and now Labour wants to bring an end to this questionable practice.”

If this is enforced, Serco, Mitie, Babcock and Capita all look vulnerable.

Retail, leisure and hospitality would also struggle. These industries have all benefited from immigration as a source of workers, but both the Conservatives and Labour favour stricter rules on immigration.

“Brexit has already made it harder for certain foreigners to find work in the UK and companies have faced a smaller pool from which to recruit, which has pushed up wages. Consumers have shouldered the brunt of these additional labour costs through higher prices,” Coatsworth said.

“This situation could be exacerbated if Labour wins the election and changes the zero hours contract system. It wants to ban ‘exploitative’ zero-hour contracts as part of a broader initiative to boost wages, make work more secure and support working individuals.”

Frasers is among the names on the stock market to have made full use of zero-hours and any change to the system means it has less flexibility for its workforce.

This scenario extends into other places such as the support services industry, with Mitie among the potential losers from a ban on zero-hours.

Finally, Rishi Sunak’s party looks ready to pass the baton onto Labour in its war on smoking and vaping – bad news for big companies in this sector such as British American Tobacco, Coatsworth concluded.

Passive funds tracking the FTSE 100 will be forced to sell St James’s Place, Ocado and RS Group.

Wealth manager St. James’s Place has been relegated from the FTSE 100 to the FTSE 250 index after regulatory pressure and fee changes prompted investors to jettison the stock. Online grocer Ocado and industrial services company RS Group have also left the UK’s large-cap index.

Meanwhile, Darktrace, LondonMetric Property and Vistry Group have been promoted to the FTSE 100 as part of FTSE Russell’s annual review. Darktrace, which specialises in cyber security using artificial intelligence, is being acquired by US private equity group Thoma Bravo.

The FTSE 250 Index has six additions and the same number of deletions. As well as the companies moving between the mid- and large-cap indices, Alpha Group International, Renew and XPS Pensions Group are joining the FTSE 250, while Ferrexpo, Mobico Group and Octopus Renewable Infrastructure Trust are leaving.

The changes will be implemented at the close of business on 21 June 2024 and will take effect from the start of trading on 24 June 2024. They will impact the portfolios of investors who own passive and exchange-traded funds tracking the UK’s large and mid-cap indexes.

St James’s Place’s (SJP) share price peaked in December 2021 and January 2022 but has plummeted since then, as the chart below shows.

SJP share price total returns over 5yrs

Source: FE Analytics

SJP scrapped its controversial exit fees last year in response to the Financial Conduct Authority’s Consumer Duty legislation. Fee changes had a detrimental impact on profit margins, according to David Cumming, manager of the BNY Mellon UK Income fund, who recently sold the position in St James’s Place he had inherited when he took over the fund two years ago. Not selling it sooner was a “mistake”, he admitted. “The management were more optimistic than things turned out and we probably stuck with it too long.”

SJP halved its dividend this year and held back £426m in provisions to refund clients who paid its ongoing advice fees but did not receive an “acceptable standard” of service, according to its full-year results.

Chief executive officer Mark FitzPatrick said: “A combination of the provision we have established and an expected decrease in the level of profit growth in the next few years as we transition to our new charging structure, reduces our ability to invest for long-term growth in our business over the next few years.”

Meanwhile, short sellers have been anticipating Ocado’s fall from grace, with the online broker becoming the UK’s second most-shorted stock last month. BlackRock, Millennium International Management and D1 Capital Partners, among others, are betting against the online grocer.

At the other end of the spectrum, LondonMetric Property and housebuilder Vistry joining the FTSE 100 augurs well for the property sector. LondonMetric Property merged with LXI REIT in January to create one of the largest publicly-traded property companies in the UK.

Vistry recently issued guidance that its annual and six-monthly profits would be ahead of last year. Dan Coatsworth, investment analyst at AJ Bell, said: “Investors like what they’re hearing and Vistry’s shares have steadily ticked up since last October with a 38% total return year-to-date (as of 29 May 2024). That makes Vistry the best performing housebuilder in the mid-cap index and the 21st best performing FTSE 350 stock so far in 2024.”

Experts suggest UK and global funds from Evenlode, Guinness, Fidelity and others.

Retired investors often have a specific income target and an aversion to losses. Bonds, therefore, make up a significant part of their portfolios but equities have a role to play as well by providing dividend income and capital growth.

Equity income funds tend to hold up better than bonds during periods of inflation, said Richard Parkin, head of retirement at BNY Mellon Investment Management.

He thinks actively-managed funds make more sense than passive trackers, “if you buy into the idea that retirement isn’t about maximising returns, it’s about avoiding losses”. Although most active managers struggle to keep up with raging bull markets, the best are adept at cushioning investors from bear markets and avoiding “howlers”, he said.

Jason Hollands, managing director of Bestinvest, recommended prioritising managers who focus on income growth potential, rather than trying to maximise current yields. “If you are going to supplement your retirement income through equity income funds, you will probably want to avoid erratic payouts but will also need to see both capital growth and income growth over time, so that payouts can keep pace with inflation,” he explained.

To that end, Trustnet asked fund selectors to recommend equity income funds that combine downside protection with growth potential.

Martin Currie UK Equity Income

Tom Stevenson, investment director at Fidelity International, argued for an allocation to UK equities.

“For investors looking to achieve a high and growing income stream in retirement, a UK equity income fund might fit the bill. The UK is traditionally a good source of equity income and today our domestic market stands at an attractive valuation discount to many other markets,” he said.

FTF Martin Currie UK Equity Income was Stevenson’s first choice. It is managed by FE fundinfo Alpha Manager Ben Russon, Colin Morton, Joanna Rands and Will Bradwell, who Stevenson said “have good experience in finding companies that can pay sustainable and growing dividends”.

The fund is relatively focused with 48 holdings, including Shell, BP, Unilever, AstraZeneca, National Grid and Imperial Brands.

BlackRock UK Income

Hollands suggested BlackRock UK Income because it “balances the need for stable, growing payouts with continued capital growth”. Managers Adam Avigdori and David Goldman have produced attractive returns with an above-market yield and the fund has held up well in difficult markets.

“The focus is on companies able or with the potential to pay a growing dividend alongside rising capital, rather than investing in businesses paying a high but stagnant yield. The managers are nimble and are able to move the portfolio around depending on the market environment and valuations,” Hollands said.

Performance of UK equity income funds vs benchmark over 10yrs

Source: FE Analytics

Evenlode Income and Evenlode Global Income

Hollands also recommended Evenlode Income, managed by Hugh Yarrow and Ben Peters. “The team has a clear and consistent investment philosophy, focused on high-quality companies with strong free cash flow that can support dividend growth and with a high return on capital. The managers prefer capital-lite businesses where shareholder capital isn’t constantly being drained by the need to reinvest heavily in things like plant and machinery,” he said.

“The fund may tend to lag in rising markets, but it has historically delivered strong and consistent outperformance.”

The fund’s global sibling is another solid choice for retired investors, according to Kamal Warraich, head of fund research at Canaccord Genuity Wealth Management. Evenlode Global Income focuses on generating attractive total returns, dividend growth and a sustainable income, he said.

“The portfolio is biased towards quality companies that generate high and consistent levels of free cash flow. Importantly, the hallmarks of this process tend to provide protection on the downside,” he explained.

JPMorgan Global Growth and Income and JPM Global Equity Income

Samir Shah, fund research analyst at Quilter Cheviot, said the JPMorgan Global Growth and Income trust is a good option for retired investors because it provides growth plus a 4% yield.

“The fund selects from only JPMorgan Asset Management’s firm-wide highest conviction ideas that offer superior earnings quality with a faster growth rate. In addition, it pays a dividend set at the beginning of each financial year equivalent to 4% of net asset value, which is funded by a combination of revenue and capital reserves,” Shah explained.

“Along with a strong track record of returns, the ability to pay a market-leading yield while also providing their best ideas from a total return perspective is attractive.”

The trust was trading at a discount of -1.1% as of 3 June 2024 and has £2.7bn in total assets. It is run by FE fundinfo Alpha Managers Helge Skibeli and Timothy Woodhouse along with Rajesh Tanna.

Juliet Schooling Latter, research director at FundCalibre, recommended another JPMorgan AM strategy managed by Skibeli – JPM Global Equity Income, which takes a value-oriented approach. “The fund's experienced management team prioritises risk management, seeking to deliver a compelling yield without compromising growth potential,” she explained.

“The managers strategically balance ‘compounders’ (companies with consistent long-term growth), high-yielding stocks and higher-growth opportunities within the portfolio. This well-diversified strategy positions the fund as a core holding for investors seeking a balance of income and capital appreciation.”

Guinness Global Equity Income

Guinness Global Equity Income is an equal-weighted portfolio of around 35 stocks, split between cyclical and defensive names. Managed by Ian Mortimer and Matthew Page, the fund has low turnover, which limits transactions costs.

Sophie Turner, a research assistant at FE Investments, said: “This fund focuses on stocks with quality characteristics and low debt, which the managers believe can provide consistent performance throughout the entire economic style. It invests into companies which have strong balance sheets and the ability to grow their dividend stream over time.

“This strong emphasis on quality and dividend growth names means the fund protects well in downturns but tends to lag in strong bull markets. The fund has shown consistent best-in-class performance over a long period, as a result of its well defined, robust and repeatable process.”

Performance of global funds vs MSCI ACWI over 10yrs

Source: FE Analytics

Fidelity Global Enhanced Income and Fidelity Global Dividend

Fidelity Global Enhanced Income uses derivatives to generate extra dividend income, with 40-60% of the fund overlaid by a covered call sleeve. This boosts the fund’s defensive profile, so it should protect capital in a falling market, although performance will lag when the stock market is rising, Turner said. Indeed, performance has been slightly below the fund’s benchmark since inception but with far less volatility.

The fund’s underlying stocks are also quite defensive, Turner pointed out. The managers – David Jehan, Fred Sykes, Jochen Breuer and Vincent Li – invest in companies with strong balance sheets and high-quality earnings which are trading at attractive valuations.

Meanwhile, Schooling Latter suggested another Fidelity International fund. “Fidelity Global Dividend is a core global income fund designed for investors seeking a stable and potentially rising stream of income,” she said.

The fund invests in companies with healthy and sustainable dividend yields, aiming to provide regular and growing distributions while prioritising capital preservation.

“We commend manager Dan Roberts’ value-driven philosophy, which emphasises disciplined investment. This reduces the risk of overpaying for stocks and potentially mitigating losses during market downturns,” she stated.

Premier Miton explains what fund managers usually get wrong.

Many traditional fund managers fail to understand a simple market dynamic that would help them build truly defensive portfolios, according to Anthony Rayner, co-manager of the £268.6m Premier Miton Cautious Monthly Income fund.

Managers who buy bonds to diversify from equities, for example, show a lack of understanding that volatility and correlation levels vary according to the investment environment.

“The more traditional fund managers will be looking for bonds to diversify equities, reflected in the common narrative that bonds are always good diversifiers of equity,” the manager said. “This is also reflected, for example, in the fact that most funds have very little in commodities like gold.”

But they aren’t the only ones who are getting this wrong. Index funds are drawn to have a “material” exposure to government bonds and a bias to longer duration, while funds with a sustainable focus will have a bias against oil, despite it being “one of the best diversifiers from equities” over time.

This tendency leaves investors to choose from a pool of investments funds that are blindly looking at what is working right now to diversify equity risk, rather than what has worked in the past and extrapolating that forward. In other words, people are failing to recognise the wake-up call of 2021, when equities and bonds took everyone by surprise crashing simultaneously.

The two graphs below look back over the past 50 years. The first chart looks at the correlation between US equities, as represented by the S&P 500, and 10-year US government bonds.

Correlation between US equities and US bonds

Source: Premier Miton, Bloomberg Finance L.P and S&P 500

“There are a number of important observations to make. Firstly, there are extended periods when bonds don’t diversify equities and, in fact, bonds have generally only diversified equities during periods of disinflation, that is when inflation risk isn’t elevated,” Rayner said.

“Secondly, in more normal periods, meaning when inflation is elevated, equities and bonds tend to be strongly correlated to each other.”

The second chart looks at the correlation between US equities and the Bloomberg Commodities index.

Correlation between US equities and commodities n

n

Source: Premier Miton, Bloomberg Finance L.P and S&P 500

In the majority of the same periods where inflation risk is elevated and bonds have been correlated with equities, commodities have proven to be “a pretty good diversifier”, the manager noted.

“Intuitively it makes sense that commodities do well when inflation is elevated, even if equities and bonds don’t. Oil and foods are often primary drivers of inflation spikes, while gold often responds positively as an inflation hedge,” he said.

“This has been borne out in more recent times, which both charts show, as the environment has been characterised by inflation, so bonds have been correlated to equities, whilst commodities have provided some diversification.”

Recognising that the same asset class has not always been the best diversifier of equity risk over time is particularly important for a defensive portfolio but also for all multi-asset portfolios, as investors understand the importance of having a defensive element to their portfolio.

“For most multi-asset portfolios, equity beta tends to be the biggest portfolio risk. Therefore, from a risk perspective, one of the most pertinent questions is how, and by how much, to diversify equity beta,” he said.

“It might sound blindingly obvious that the environment drives an asset class’ behaviour, but all too frequently investors do not follow this logic through when it comes to the practice of portfolio construction,” Rayner concluded.

It’s natural to worry about how possible regime change in Westminster may affect our investments, but we see four reasons for comfort.

The context of the forthcoming election is that the Conservative Party has a mountain to climb to avoid a heavy defeat. Labour has a large lead in the polls (around 20 percentage points) that has been sustained for more than a year and a half.

The polls can of course be wrong, or shift – but it would take a historic swing in such a short time to make a big difference to the outcome.

UK election opinion polls

Source: Rathbones

It isn’t just the polls suggesting that the Conservatives face an uphill battle, the public rate Labour better than the Conservatives on all three of the issues they care most about – the economy, the NHS and immigration.

Rishi Sunak is personally unpopular too, in contrast to the start of his premiership. His net approval rating is now close to that of Liz Truss at the end of her ill-fated time in Number 10, and far behind that of Keir Starmer.

Local elections earlier this month also saw the Conservatives lose hundreds of councillors, while several recent by-elections have seen swings to Labour well above 20 percentage points.

In other words, the chance of a change in the political landscape, after 14 years of Conservative rule, is high. It’s natural to worry about how possible regime change in Westminster may affect our investments, but we see four reasons for comfort.

No dramatic short-term change in fiscal policy on the cards

Shadow chancellor Rachel Reeves has taken a leaf out of the Blair/Brown 1997 playbook in shadowing a lot of existing economic policy. She has pledged not to raise the most significant taxes – income tax, national insurance, capital gains tax and corporation tax.

And she has committed to follow a set of fiscal rules virtually identical to the current ones (as well as showing her commitment to those rules by ditching previous pledges which don’t comply with them).

This cautious strategy means the election is not likely to alter the short-term path of the economy much, or to upset the gilt market. Labour’s clearest points of difference on fiscal policy are arguably its plan to charge VAT on private school fees and to change the tax treatment of carried interest.

That’s significant for those affected but doesn’t move the needle for the economy. We’d expect it to continue its recovery from the shallow recession of last year.

Total managed expenditure

Source: Rathbones

Whichever party wins the next election will eventually have to confront the so-called ‘fiscal fiction’ which underlies current spending plans. This is the assumption that there will be significant spending restraint in key departments, which are likely to prove politically impossible in practice. But that isn’t a Labour-specific issue.

Labour has dropped radicalism of Corbyn era

The past general election in 2019 offered voters two radically different economic visions, Boris Johnson’s pledge to ‘Get Brexit Done’ against Jeremy Corbyn’s socialist agenda.

But the Labour Party has transformed since then, emphasising ‘partnership with business’ and courting the City. There are some key differences between the two parties’ economic policy platforms today, but these are much smaller than in 2019.

Gone is Labour’s commitment to nationalisation. The party does plan to renationalise virtually all passenger rail services within five years, as existing contracts with private operators expire. Yet things have been moving in this direction by stealth anyway.

The current government has already taken over several major rail franchises, including Southeastern, LNER, ScotRail and TransPennine. Labour also plans to establish a publicly owned company to invest in green energy, such as floating offshore wind, but this is no wholesale nationalisation.

New government may have political capital for much-needed reform

Reflecting the long-term poor performance of the UK economy, there are a few key areas which both main parties have identified as ripe for change, but where the current government has failed to muster the political capital to pass any significant reform. A new government with a fresh mandate could make a positive difference.

GDP per hour worked in dollars

Source: Rathbones

The context behind all of this is the weakness of productivity growth in the UK since the global financial crisis, which in turn is linked to the long-term weakness of investment. (shown in the chart above and below.)

Investment as a percentage of GDP

Source: Rathbones

Many of the specific problems policymakers worry most about – from regional inequality to the state of the health service – are ultimately connected to insufficient investment.

A key issue both parties have identified as a barrier to investment is the UK’s unusual planning system. Our system is discretion-based, whereas virtually every other advanced economy relies more on zoning and rules.

It is slow and unpredictable, discourages development and makes building much-needed infrastructure harder. Infrastructure projects here face much higher costs than other advanced economies, in part because of planning-related delays and legal challenges.

London’s CrossRail, for example, cost 10 times as much per mile as Madrid’s metro system. The spiralling costs of HS2 are notorious, and the project has been the defendant in 45 separate legal cases since 2018.

This would be an appealing area for a new government with a fresh mandate to address, particularly as it can be done without the need for large spending commitments.

Rachel Reeves said, “This Labour Party will put planning reform at the very centre of our economic and political argument.”

There is likely to be a more standardised approach to what is and isn’t allowed. More planners will be hired to reduce backlogs and delays too. So-called ‘grey belt’ land may be targeted for development – things like car parks and wasteland which are currently part of the green belt.

Investors have set the bar for success low

UK assets currently appear cheap compared to their fundamentals on a variety of different measures. International investors fell out of love with UK equities in the period of instability which followed the 2016 Brexit vote. It wasn’t until then that the gap between the valuations of stocks in the UK and elsewhere (particularly the US) emerged.

Price-to-earnings ratios, adjusted for sector composition

Source: Rathbones

The gap is much larger than can be explained by the relative growth and quality characteristics of UK firms, or by the sectoral makeup of the UK market. The story is similar when we analyse currencies – sterling trades well below measures of its ‘fair value’ based on economic fundamentals.

Some reasons for international investors’ antipathy towards UK assets could change. Following years of domestic political instability – characterised by a succession of prime ministers and a lack of policy space to address structural issues – the possibility of a new government with a reasonable majority engenders hope.

Stability alone might be an improvement on the political and economic turmoil that has existed since 2016. Investors have set the bar for success for the next administration low.

Oliver Jones is head of asset allocation at Rathbones. The views expressed above should not be taken as investment advice.

Three Allianz bond funds have their ratings removed following Mike Riddell’s departure.

Three of Allianz Global Investors’ bond funds have been expelled from the Square Mile Academy of Funds, the investment consulting and research firm announced today.

Baillie Gifford and GAM funds also lost ground.

The departure of Mike Riddell, lead manager of the A-rated Allianz Strategic Bond, Allianz Index-Linked Gilt and Allianz Gilt Yield funds, spurred Square Mile’s decision to remove its ratings from all three strategies.

“Julian Le Beron, chief investment officer of core fixed income at Allianz, will assume immediate control of the funds, bringing a different investment approach,” Square Mile explained.

“As the funds’ ratings were centred around the analysts’ conviction in Riddell and the process which he built over several years at Allianz, they feel they can no longer support their inclusion in the Academy of Funds.”

In the wake of Riddell’s move to Fidelity International, fund selectors suggested five alternative strategic bond strategies for investors looking to move their money.

Elsewhere, Baillie Gifford Multi Asset Growth also lost its a rating after its medium-term performance failed to live up to analysts’ expectations.

“This, coupled with changes within the underlying team, has led to conviction falling to a level where they no longer feel they can support the fund’s place within the Academy of Funds,” Square Mile noted.

Performance of fund against sector and index over 5yrs

Source: FE Analytics

Square Mile’s conviction in the GAM Star Japan Leaders fund also waned, due to “instability in the management team over recent years and a continual decline in assets under management”.

The size of the fund peaked at approximately £320m in September 2021 and steadily declined to today’s £73m. Therefore, the analysts decided to remove the fund’s A rating..

Moving to the new entrants, two strategies joined the Academy of Funds with newly awarded A ratings.

The first was the Fidelity China Special Situations trust, which Square Mile said was ideal for long-term investors seeking broad exposure to China, offering access to both listed and unlisted companies, as well as those with significant interest in Chinese markets.

It has significant exposure to medium and smaller companies and was prized by Square Mile analysts for the combination of “an experienced portfolio manager supported by a well-resourced analyst team, and an efficacious process within an under-researched opportunity set”.

While the IT China/Greater China sector only includes three trusts, Fidelity’s solution has topped the rest across all time frames and came first for performance over 10, five and three years, as well as one month.

Performance of fund against sector and index over 5yrs

Source: FE Analytics

The second entrant was Capital Group New Perspective, which was officially launched in 2015, but the broader strategy dates back over half a century. It has “a proven track record of delivering excess returns through the cycle” and of keeping up when market leadership changes.

“Drawing upon Capital Group’s multiple-manager approach, the fund takes a flexible approach to managing assets to identify transformational changes in the global economy and to benefit from long-term structural trends in markets,” Square Mile analysts said.

“Overall, we believe this fund to be a solid offering for long-term investors looking for a global equity strategy that is managed in a risk-aware manner and seeks to remain competitive across most market conditions.”

Source: FE Analytics

Finally, the Premier Miton Multi-Asset Distribution and Multi-Asset Monthly Income funds were downgraded from AA to A ratings as the long-standing co-head of the multi-manager team, David Hambidge is stepping back from day-to-day fund management responsibilities on 1 July.

David Cumming, who manages the BNY Mellon UK Income fund, has taken counter-consensus positions in real estate and oil companies.

Income investors tend to swim against the tide, buying companies that are undervalued and therefore are paying out yields above the market. This method of investing has been a tough one in recent years as growth investors – and in particular those favouring technology – have thrived.

Yet David Cumming, who manages the £1.6bn BNY Mellon UK Income fund, is sticking with his contrarian stance. “One of my favourite lines is: only dead fish swim with the stream,” he said, implying that investors should challenge the conventional wisdom.

He is a big believer in meeting with company management and through these conversations, he aims to identify trends early and take counter-consensus views. These currently include owning oil companies, going overweight banks and going “slightly long” property, which he thinks has “probably bottomed”.

Real estate investment trusts are trading at 30% discounts while the underlying assets are yielding around 6%, he said. He owns Land Securities and Hammerson and favours retail property, which should benefit from the UK’s economic recovery and interest rates plateauing.

His contrarian bets are paying off. Cumming has been running the fund for just over two years, having joined Newton Investment Management (the BNY subsidiary where he leads the UK equity team) in March 2022 from Aviva Investors.

Performance of fund over 2yrs vs benchmark and sector

Source: FE Analytics

Between 1 April 2022 and 28 May 2024, the fund has delivered top-quartile performance and ranks 13th amongst the 77 funds in the IA UK Equity Income sector. Over three years to 28 May 2024, it is the second-best performing fund within its sector.

One of his biggest calls has been to buy banks, which used to be a lonely position but is becoming more mainstream, with Barclays and NatWest rallying strongly since February.

Performance of banks year-to-date

Source: FE Analytics

Banks underperformed for a decade after the financial crisis while they steadily built up their capital reserves. “A lot of people just stopped owning them and ignored the fact that they've become very cheap,” he observed.

As interest rates increased, banks’ profit margins improved, which was the catalyst for a re-rating but even Cumming, who has been long banks for a while, was surprised by the speed and scale of their recovery this year.

He owns Barclays, Lloyds, Standard Chartered and HSBC, all of which he said have good management teams, good cash flows and high dividends. “If you add buybacks and dividend yields together, you're getting 10% plus,” he said. Barclays and Standard Chartered are still trading at around half book value despite the recent rally, he added.

The fund can invest up to 20% of its assets outside of the UK and Cumming has bought shares in Swiss private bank Julius Baer, which should be able to take market share following the collapse of Credit Suisse and its merger with UBS, he argued. The company also has a strong position in Asia where wealth is growing quickly.

Cumming has also invested in asset management group M&G this year, as it pays a 9% yield and has “double-digit upside potential”.

“There's a high payout ratio and growth, which is quite a combination,” he said. M&G’s shares should track or beat the market but he expects a higher total return because of the dividend.

M&G has a strong position in fixed income, robust distribution capabilities, good investment performance, an established market position in Europe, and it is growing its business in the Middle East, he concluded.

Cumming also thinks oil companies have plenty of upside, good recovery prospects and low valuations. BP and Shell tend to trade at 30% discounts to equivalent US-based companies and have double-digit free cash flow yields.

Demand for oil and for energy is increasing and while climate change is still a vital issue, people are acknowledging that oil is a necessary part of the transition. “I would say the [environmental, social and governance] ESG zeitgeist is going more pro-oil,” he said.

BP could be vulnerable to bids from international acquirers given its low valuation, he said, although he is not entirely sure that the government would allow BP to be acquired.

Cumming is also leaning into the UK’s economic recovery by increasing his exposure to economically sensitive sectors, including materials and industrials, as well as financials and energy. On the other hand, he is light consumer staples, telecoms and utilities. “Most income funds are low beta but we’re the opposite. We hope to outperform in a rising market,” he explained.

Trustnet uses Investment Association data to highlight the top payers in the sector.

Just six funds have consistently beaten the FTSE All Share’s yield by more than 10% each year, a study from Trustnet has found.

Income investing has been resurgent of late as investors have started to put their cash to work ahead of impending interest rate cuts from the Bank of England later this year.

Top of most agendas is getting a decent payout from dividends, with yields of particular interest to investors who want to get the highest income possible.

The IA UK Equity Income sector has strict rules in place to ensure investors are getting a fair yield. At present, each fund in the sector must achieve a yield that matches the FTSE All Share index over three years. If it fails, it is removed from the Investment Association (IA) peer group.

Additionally, should a fund deliver less than 90% of the FTSE All Share’s yield in any given year, it will also be excluded. It is worth noting, however, that these rules were relaxed during Covid, with funds given a pass on these requirements in either 2020 or 2021 (they could choose one, but were not permitted both).

With this, all of the funds in the sector have achieved their goal and remain in the peer group. However, these current rules only came into effect in 2017.

The new guidelines were amended after a swathe of income funds – including some of the largest portfolios at the time – failed to meet the previous criteria. This was to achieve a 110% yield over a three-year period.

For this study, Trustnet increased this hurdle rate one step further, looking at funds that have achieved a yield that is higher than110% of the FTSE All Share’s in every year since 2010, when the IA began collecting these records.

To do this we used data from the IA and took the yield as at the fund’s own end of year reporting window.

Source: Investment Association

Just six funds had a 100% track record. Fidelity Enhanced Income and Santander Equity Income Unit Trust were the two with the longest track records, achieving higher-than-market yields in each of the 14 years looked at. It currently yields 6.91%.

The former has been managed by David Jehan since its launch in 2009, with Rupert Gifford joining in 2020. The strategy is specifically designed to produce an income that is 50% higher than that of the index. To do this it predominantly invests in equities, but can also use derivatives such as cover call options to enhance the income.

Gifford runs the equity portion having worked closely with former longtime manager Michael Clark, identifying steady companies, which have tended to cope well with difficult economic conditions. Jehan looks after the derivatives portion of the fund.

Analysts at Square Mile Investment Consulting & Research give the £219m fund a ‘Positive Propsect’ rating and said: “The combination of these two elements is an appealing proposition for investors who have an income requirement. However, unit holders must recognise that what is gained on the swings is likely to be lost on the roundabouts.

“In this case, income will be higher than more traditionally managed UK equity income strategies, but this is likely to be at the expense of capital appreciation. That being said, on a total return basis (i.e. the combination of income and capital growth), there is unlikely to be too much difference, particularly on a risk-adjusted basis, in returns over the very long term.”

The £118m Santander fund has been managed by Robert McElvanney since 2020, who has continued its track record of beating the FTSE All Share yield by more than 10% in each year, although its aim is to match the current guidelines set by the IA.

It currently yields 4.34% and has been by far the best performer of the group over the past decade, returning 76.9%, placing it in the second quartile of the IA UK Equity Income sector over this time.

The fund managed to make the list ahead of its Santander Enhanced Income Portfolio stablemate. This fund, like the Fidelity portfolio, aims for a yield of 5% per year, but failed to beat our high hurdle rate in 2020, when its end of year date (31 March) coincided with the market collapsing due to the pandemic and the FTSE All Share had a supranormal yield.

Next, Premier Miton Monthly Income has achieved the feat in 13 consecutive years, while its cousin Premier Miton Optimum Income has achieved a yield of above 110% of the FTSE All Share in 10 years.

Emma Mogford has run the former as sole manager since 2020, replacing Eric Moore, who had in turn replaced Chris White. She was also added as co-manager to the Optimum Income fund at the same time, running it alongside Geoff Kirk.

Analysts at RSMR rate both funds and said the firm has a “highly experienced UK Equity Income team”.

On the Monthly Income strategy, they said it was a “traditional, uncomplicated UK equity income fund which has performed well (particularly from an income perspective)”.

“The focus on dividend growth has help contribute to income returns. The fund provides a better than average dividend yield with lower volatility. In addition, the manager aims to grow the dividend yield by 5% per annum. This has been achieved over the previous five consecutive fund years.”

On the Optimum Income fund, they liked its “core large-cap strategy”, while highlighting its use of a covered call strategy to enhance the overall level of income.

IFSL Marlborough Multi Cap Income and VT Downing Small & Mid-Cap Income are the final funds on the list to achieve the feat. Both invest predominantly in mid- and small-cap stocks. This has hit performance in recent years as this area of the market has struggled.

Sectors not regions will be the way to outperform as US exceptionalism wanes, according to Pictet Asset Management.

Double-digit returns from US and global equities will be consigned to the history books as the factors underpinning US exceptionalism and high valuations dissipate, according to Pictet Asset Management.

Overall, global equities will deliver 7.6% per annum for the next five years, but the way to generate much higher returns going forward will be to choose the right sectors, said chief strategist Luca Paolini.

Technology, healthcare and industrials will benefit from innovation and artificial intelligence (AI), ageing populations, climate change and protectionism. These three sectors should outperform global equity benchmarks by a cumulative 20% over the coming five years, he said.

“These industries are pivotal in resolving some of our greatest long-term challenges, namely climate change, fraught geopolitics and growing labour shortages. In other words, in times of increasing uncertainty, we seek exposure to sectors that are the problem solvers,” he explained.

Pictet expects returns from growth and value strategies to be more evenly balanced over the next five years. Growth strategies will benefit from developments in AI but value strategies with a higher weighting to industrials will profit from onshoring, nearshoring and “muscular industrial policy”, Paolini added.

The markets that will do well

From a geographical perspective, Pictet is expecting annualised returns of 7.5% from US equities over five years – still around the world average but below its recent dominance. “Elements of US exceptionalism are rolling over,” Paolini said. He thinks low taxes and record amounts of government spending are unsustainable, while US leadership in AI and GLP-1 weight loss drugs will boost growth only marginally.

The S&P 500 is trading at a price-to-earnings (P/E) multiple of 21x compared to a long-term historical average of 16x. Paolini thinks a P/E multiple of 19x would represent fair value over the next five years and said the stock market’s current rich valuations will compress long-term returns.

US exceptionalism will not necessarily go into reverse but it will pause, giving other regions the chance to catch up, he predicted.

Emerging market companies in particular are getting better at translating economic growth into earnings growth and India is the world’s fastest growing region, he said.

Pictet expects emerging market equities to return 8.3% per annum in US dollar terms for the next five years and Latin American equities to do even better, returning 8.5%, as the chart below shows.

Five-year return forecasts in US dollar terms

Source: Pictet Asset Management, Refinitiv, Bloomberg

Inflation is a headwind for emerging market stocks – which explains their flat performance this year – but if inflation normalises and the global economy holds up, then emerging market equities should perform well, Paolini explained.

The UK and Europe are falling behind

Languishing at the bottom of the league table are UK and eurozone equities, which are projected to return 6.7% and 6.8%, respectively.

The UK is a defensive market full of well-managed, cheap companies but it does not have a vibrant or large technology sector so the market is “not very exciting”, Paolini admitted.

Arun Sai, senior multi-asset strategist, described the UK as a “stagflation play” because of its exposure to commodities. “You would need a peculiar macro set up for the UK to out-deliver on earnings versus global peers,” he noted. “The UK is essentially defensive value.”

A word on bonds

Turning to fixed income, total returns from 10-year US government bonds are forecast to be 5.6% on an annualised basis for the next five years, with 10-year Treasury yields settling at 3.75%. This means that equities will still outperform bonds, but by a relatively slim margin, as rising bond yields enhance the appeal of fixed income.

Paolini suggested that asset allocators move some money out of equities into credit, predicting a 6.3% annualised return from US investment-grade bonds. Returns from corporate bonds are likely to be on a par with equities, but with less risk and lower volatility as default rates remain benign.

Currencies and alternatives

Currency movements will assume greater relative importance going forward as they will eat into the muted returns that Pictet expects equities and most other asset classes to deliver.

Pictet predicts that the US dollar will weaken gradually by 2% per annum over the next five years, which will be a tailwind for local currency emerging market debt – an asset class that is forecast to return 8.9% per annum, beating hard currency emerging market debt and emerging market equities.

Meanwhile, Paolini believes investors should maintain exposure to alternatives and real assets but he acknowledged that these strategies are less attractive relative to listed assets than in the past.

In private equity, private debt and real estate, the gap between the best and worst performing managers is “massive” so manager selection is more important than asset allocation, he said.

The ultimate winners in the AI race have yet to be determined but the infrastructure needed to support AI, from data centres to semiconductors, is already experiencing a capex boom.

The rapid development of generative artificial intelligence (AI) tools has been a central concern of businesses and markets over the past three years. Demonstrated by the dominance of the ‘Magnificent Seven’, valuations reflect the widespread expectation that this will be an ongoing phenomenon.

Much of the discussion about AI technologies has focused on the hypothetical. Speculation is at fever pitch regarding the potential for AI to transform tasks as mundane as grocery shopping and as advanced as surgery. Yet, few tools have become mainstays of daily life.

Up until now, activity in the AI sector has focused on training models and machine learning. This has aimed to produce systems sophisticated enough to support complex requests and applications.

The significant transition that is only just beginning is for the technology to rotate from training to usage.

It is here that the outlook for the sector becomes murkier. The ‘winners’ in terms of both models themselves and their makers have not been determined.

However, capital expenditure has been – and continues to be – significantly ramped up in a bid to capture future markets. Companies such as Meta and Microsoft have staggering sums of money to spend, supported by their prodigious earnings growth from their existing businesses and cash-rich balance sheets.

In the first quarter of 2024, Microsoft’s capex rose 79% to $14bn, while Meta plans to increase its capex in 2024 overall by at least $5bn.

The question that most readily comes to our minds is: where is all that money going?

It is here that a more certain set of winners lies. AI may itself have a dramatic impact on our lives, society and physical world. The resources needed to support its evolution, though, are already experiencing – and creating – such an effect.

The expansion of AI requires significant infrastructure support – and that needs to be firmly in place before any transition can happen.

With this in mind, tangential operations such as data centres have become increasingly central to the AI revolution. Estimates suggest that AI-supporting data centres use two and a half times more energy than legacy data centres. With extra processing comes extra heat produced. As such, cooling technology has become a central requirement in the AI transition, accounting for up to 40% of that energy use.

Another example is memory. Devices will need to have additional memory capabilities to support the most challenging AI applications. As these functions come online, that hardware will need to be in place already.

As Nvidia’s meteoric share price rise demonstrates, semiconductors are a crucial component of this transition. This opportunity is investable via semiconductor producers themselves, through to the producers of the equipment used to manufacture the chips. The AI investing pool runs deep.

Indeed, down to the cabling required to carry so much additional data both within the data centres and around the world, a global supply chain is establishing itself.

Another question to ask ourselves though is: who will be the eventual winners among the AI service providers?

Ultimately, this is hard to forecast. One thing that seems certain is that our technology platform is likely to expand dramatically. Cisco has predicted that 500 billion devices will be connected by 2030, a rise from 13 billion in 2013.

This ultimately circles back to having the resources in place to support any applications that do come online. The demand for energy has already surged with the use of large language models. This exacerbated the increase in electricity use that was already coming from electric vehicles, heat pumps and other areas of the green transition.

The tension that this represents was most clearly reflected when Amazon purchased a data centre with its own nuclear power source earlier in the year.

With Western societies unused to energy needs increasing, this presents a significant challenge. However, among established energy producers, it also presents an opportunity.

Ben Lofthouse is the fund manager of Henderson International Income Trust. The views expressed above should not be taken as investment advice.

Experts discuss the departure of the manager and investment case for the fund.

Veteran manager Kevin Murphy will leave Schroders after 24 years at the firm to join his brother Dermot and former Jupiter Asset Management fund manager Ben Whitmore at the newly founded Brickwood Asset Management.

With the move, he will give up his role as co-manager of the Schroder Recovery, Income and Income Maximiser funds. Schroders has announced that Nick Kirrage, who currently leads the global value team, will join Andrew Lyddon and Andy Evans on all UK value portfolios, taking back a position that he held between 2006 and 2022.

A Schroders spokesperson said: “Continuity is key with the transition and succession being meticulously managed on behalf of our clients whose service and investment focus will remain unchanged.”

Performance of fund against sector and index since Murphy’s tenure

Source: FE Analytics

Murphy’s departing has dealt “a blow” to the Schroders team, according to Tom Green, fund analyst at FE Invest.

“This is a blow to the team, as Murphy was one of the founding members of the value team and does a lot of the work around the evolution of the funds process,” he said.

The income fund has a “long-term, successful track-record in value investing” and was recommended by FE Investments for its ability to move into positions quickly when stocks sell off aggressively as well as the team’s contrarian positions, which historically paid off in the long term.

The exit doesn’t necessarily impact these strong points, according to Green, who retained his conviction.

“Other members of the team also work with Murphy and due to the very experienced wider team, we have fewer concerns than if this was a single-manager structure,” the analyst concluded.

Ben Yearsley, investment consultant at Fairview Investing, broadly agreed with Green.

“It's a slightly strange move [for Murphy], as it results in two big beasts of the value jungle [Murphy and Whitmore] together. Maybe the opportunity to work with Whitmore as well as his brother was a big draw,” he said.

“It’s a shame for Schroders, as Murphy and Kirrage have always made an excellent team. But long gone are the days when it was only the two of them – it’s a much broader team now, which will be headed up by Kirrage solely.”

As for how investors in one or multiple products run by the team should react to the news, Yearsley said that “those who were happy holders before have no reason to change that view”.

Also not changing their views were the analysts at Square Mile Investment Consulting and Research, who have an ‘A’ rating on the Schroder Income fund.

Senior investment research analyst David Holder said that while it is “disappointing” that the Schroders team has lost “such a seasoned value investor”, the main effect of the move is to “further enhance Brickwood’s credibility” within the value investing space.

As for the consequences for Schroders, the re-introduction of Kirrage into the team “should very much comfort investors”.

“The three-person sub-team overseeing all UK value mandates is very well placed in terms of collegiate understanding, depth of investment knowledge and experience in this area of the UK market,” Holder said.

“The strength and depth of experience within the team remains cohesive and strong and as such, Square Mile has retained the A rating on the Income fund as well as the Recovery and Income Maximiser funds.”

Alphawave Semi’s transition away from China has hit its earnings expectations.

Alphawave IP Group (known as Alphawave Semi) has been targeted by short-sellers after revising its earnings expectations downwards. The company, which provides high-speed connectivity solutions for data centres, artificial intelligence and 5G wireless infrastructure, revealed in mid-April that its 2023 earnings would fall below its original forecasts due to its “accelerated transition away from China”.

The company warned that its investments in research and development would have a negative impact on profits and that revenues from “long-term contracts in advanced nodes” would be lower than expected.

Alphawave Semi published its annual report a week later, on 23 April 2024, with revenues of $321.7m for 2023. This represented a 74% increase compared to 2022 but fell below the company’s original outlook of $340m to $360m.

JPMorgan Asset Management disclosed a short position in Alphawave Semi last month amounting to 1.4% of the latter’s share capital. Marshall Wace, GLG Partners and Kuvari Partners have placed smaller bets against Alphawave Semi, according to the Financial Conduct Authority.

These bets have catapulted Alphawave Semi into the 10 most shorted UK-listed companies, ranked by the percentage of their share capital in the hands of short sellers.

Alphawave Semi listed on the London Stock Exchange three years ago and its share price peaked at £4.52 on 6 August 2021. It fell to £1.80 by 5 November 2021 and has been fairly range-bound since then. It was trading at £1.36 at the time of writing on 3 June 2024.

Short-sellers have also increased their bets against Ocado, which was the second most-shorted stock last month and risks being ejected from the FTSE 100 in its imminent reshuffle.

Dan Coatsworth, investment analyst at AJ Bell, described Ocado as “one of the most Marmite names on the UK stock market”.

“Investors either love or hate the quasi grocery/technology group and some even change their mind on a daily or weekly basis,” he said.

“There is always a ‘will it, won’t it’ element in trying to second guess what Ocado is doing strategically. On paper, the business model is focused on winning more grocery clients to power its online shopping warehouses, while also trying to improve the performance of a joint venture with Marks & Spencer. In reality, progress has been lumpier than gravy in a school canteen,” he concluded.

Energy facilities company Petrofac remains the UK’s most-shorted stock, as the table below shows.

Source: Financial Conduct Authority

Don’t miss out on the possible resurgence of the domestic market, experts warn.

Momentum is gathering for UK stocks, which surged through record highs last month, and the upcoming elections are drawing even more attention to the domestic market.

Indeed the FTSE 100 peaked at 8,445.8 in May, almost 600 points ahead of its pre-Covid levels, although it remains some way below the likes of the US’ S&P 500 index (11.2% return year-to-date), with the UK large-cap index up 9% in 2024 so far.

Whether this resurgence will be enough for investors to reconsider their preference for global investments and return to the unloved UK market remains to be seen, but experts are becoming more vocal about the opportunities cropping up domestically.

Trustnet has recently asked whether it's time for a patriotic punt on the UK stock market and many commentators pointed out the favourable entry point due to cheap valuations, increased international merger and acquisition (M&A) activity, improvement in economic data, imminent rate cuts and “voracious” share buybacks.

On top of that, many UK stocks have surged past most of the magnificent seven, with very few people noticing.

Hal Cook, senior investment analyst at Hargreaves Lansdown, said there is a lot to like about the UK stock market.

“With mature industries such as banks, oil and gas and tobacco, the UK has been known as a good place to look for dividend income, but there are plenty of growth opportunities too – from big consumer goods companies selling their products globally to smaller businesses looking to grow into the giants of tomorrow,” he said.

“We think this combination and the discount on offer compared to other regions make the UK an attractive place to invest right now.”

The main way – and the cheapest – to invest in the UK are exchange-traded funds (ETFs), according to Cook, whose preference was for two iShares and one Vanguard solutions.

For investors who want to get exposure to the largest UK companies, he recommended the iShares Core FTSE 100 ETF, which tracks the performance of the FTSE 100 index.

Performance of fund against sector and index over 1yr

Source: FE Analytics

“It does this by investing in every company and in proportion with each company’s index weight. This is known as full replication, which can help the ETF track the index closely,” he said.

The £2.2bn fund is passively managed by Blackrock, has achieved an FE fundinfo passive fund Crown-rating of five, and only charges 0.07%.

ETFs also offer access to income-paying stocks and Cook’s pick was iShares UK Dividend ETF, a low-cost option for tracking the performance of the FTSE Dividend UK+ index with a price tag of just 0.40%.

Performance of fund against sector and index over 1yr

Source: FE Analytics

This £848m vehicle offers exposure to 50 of the highest dividend-paying stocks listed in the UK, while still making sure it’s diversified across multiple sectors. The trailing 12-month yield is currently 5.45%.

Finally, medium-sized companies enthusiasts should consider the Vanguard FTSE 250 ETF, which aims to track the performance of medium-sized companies in the UK as measured by the FTSE 250 index.

Performance of fund against sector and index over 1yr

Source: FE Analytics

FE Investments analysts highlighted this fund for its simple method of replicating the performance of the index by direct ownership of all the underlying securities as well as its usage of stock lending, a practice by which a select third party borrows a limited amount of the passive fund’s holdings in exchange for a fee.

This supplements fund returns and compensates for the trading costs involved with direct ownership of the securities.

Among the investment management houses, Hawksmoor has been betting big on a UK recovery. Chief investment officer Ben Conway said that a FTSE 250 tracker would be a good option to capture a broad spectrum of opportunities in the mid-cap space, but fans of active management can also consider Aberforth Smaller Companies and Odyssean.

Not everything will be smooth sailing for the UK, however, and work remains to be done in a number of areas. The finance industry has been advocating for a number of changes to get Britain back on track.

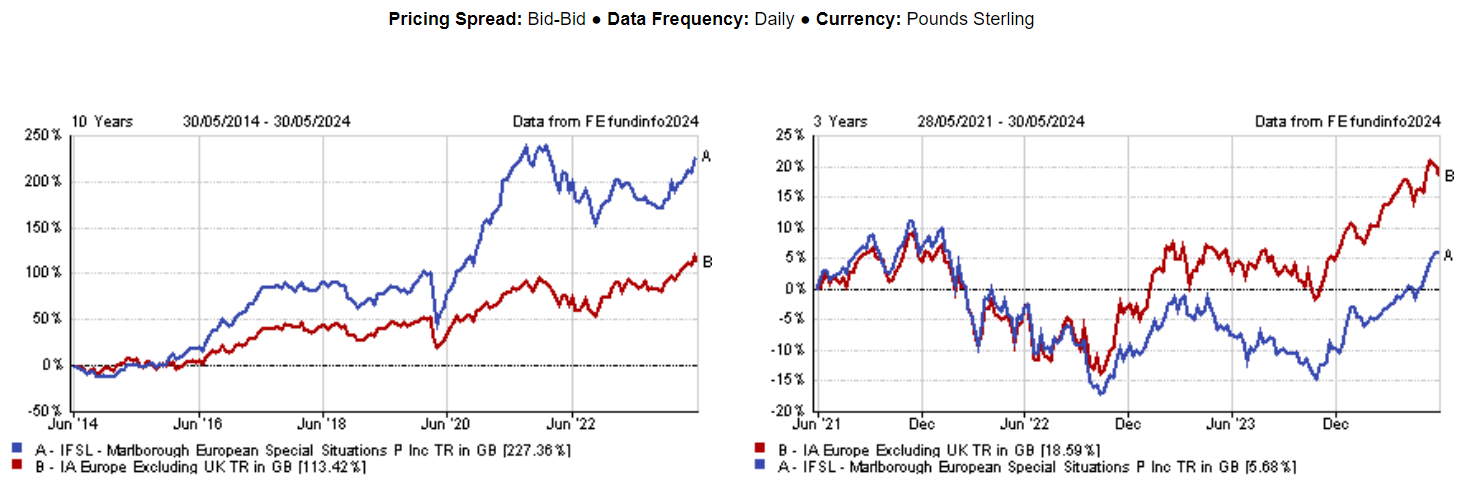

Chelsea Financial Services and FundCalibre managing director Darius McDermott examines the catalyst for continued outperformance from emerging markets.

The last decade has been challenging for investors who have backed the emerging markets (EM) growth story. In that time the MSCI Emerging Markets index has produced around a third of the returns produced by developed markets (73% vs. 213%)*.

There are plenty of reasons for this – many EM economies have suffered since the 2001-2010 boom, which was fuelled by the likes of China’s rapid growth and the commodities super cycle. This is because many had uncompetitive currencies and failed to reform, particularly among those who exported commodities. The US dollar has also been largely strong since 2014, hampering US-dollar earnings-per-share growth for EM companies. We’ve also seen commodities prices ease, China’s growth engine slow and intensified geopolitical concerns.

The start of this year saw the MSCI Emerging Markets index fall 4.7%, the largest fall since January 1998**. This was because investors believed the strength of the US economy would lead to the Federal Reserve holding rates at their peak for longer. But the expectation of loosening financial conditions (lower rates) across the globe has started to initiate a broader recovery, with riskier assets like EMs up 6.1% in the past three months alone***.

Could a recovery in earnings growth, resilience in the US economy and the potential peak in US interest rates be the catalyst for continued outperformance in EMs from here? Clearly there are still dangers, there are plenty of elections in the region this year (not to mention the US), while many believe there is a lagged effect from high interest rates which will drag on the economy.

Falling rates one of a number of reasons for optimism

Although more rate cuts were anticipated at the start of 2024, the expectation is they are not too far away now and they should benefit many EMs, particularly areas like Latin America. This is where the US dollar comes into play, as rates come down in the US the dollar should stabilise (it will not be as strong) and weaken against other EMs. History shows the positive impact of rate cuts on EMs – with equities in the region rising by an average of 14% in the initial 12 months following the first Federal Reserve rate cut****.

GDP growth in EMs is also accelerating at a time when it is slowing in the developed world. Figures from the International Monetary Fund project growth of 1.7% and 1.8% for developed world economies in 2024 and 2025 respectively (vs. 4.2 per cent for EM’s in both years)^. Part of this is because EMs came out of Covid later, meanwhile EM consumers were not supported by governments in the emerging world, this means the recovery for the consumer has taken longer.

The third point is the ripple effect of China’s underperformance on EMs. Having fallen over 40% since February 2021, the re-rating of its equity market has been indiscriminate – and that has created plenty of valuation opportunities in the region for active managers^^.

Then there is earnings growth and valuations across the board. Consensus earnings growth for EM in 2024 and 2025 stands at 19% and 15% respectively, compared to 11% and 13% in the United States**. Meanwhile valuations look compelling, with EMs trading on a price-to-earnings multiple of 12x, compared to 18.9x for the developed markets and 21.9x for the US**.

Dispersion the order of the day

As we know many of these markets have different drivers supporting their growth today, so dispersion across countries and sub-regions is likely to be rife. Research from S&P Global indicates growth may moderate for many countries that outperformed in 2023 (such as Brazil, Mexico, and India) but remain relatively strong. By contrast those who underperformed last year (Colombia, Peru, Thailand, Hungary, Poland and South Africa) will grow modestly faster this year^^^.

When you add in the long-term demographic tailwinds and the rise of the middle-class, EMs do look attractive at this point, but you have to accept those bumps in the road. You also have to have a view on China and the impact it has on the wider region, but there are now plenty of different ways to invest across the region without being tied to one specific theme.

Those looking for exposure to the asset class might want to consider the likes of the JPMorgan Emerging Markets Investment Trust, which invest in around 60-100 high quality business, with the average investment held for 10 years. An alternative high conviction name would be the FP Carmignac Emerging Markets fund, a high conviction portfolio of 35-55 large and mid-cap firms.

Those who want a reasonable exposure to China may want to look at the FSSA Global Emerging Markets Focus fund, managed by Rasmus Nemmoe and Naren Gorthy, which currently has a third of its exposure in the country with names like Tencent, Tsingtao Brewery and JD.com sitting in its top 10 holdings^^^^.

By contrast, those who are wary of China might look to the likes of the Jupiter Asian Income fund, with manager Jason Pidcock citing political concerns as the main reason for not investing in China. He sold his last remaining mainland China stocks, as well as one Macau-based business, in July 2022, but had been underweight China for some time, due to his low expectations of corporate profitability relative to the rest of the region. Pidcock aims to yield 20% more than the respective benchmark. The portfolio is typically high conviction with between 30-50 stocks held. The focus on large companies with reliable returns, makes it an attractive defensive option.

*Source: FE Analytics, total returns in pounds sterling, from 30 May 2014 to 30 May 2024

**Source: Lazard, Outlook for Global Emerging Markets, April 2024

***Source: FE Analytics, total returns in pounds sterling, from 27 February 2024 to 27 May 2024

****Source: Franklin Templeton, 8 January 2024

^Source: International Monetary Fund, World Economic Outlook, April 2024

^^Source: FE Analytics, total returns in pounds sterling, from 1 February 2021 to 30 May 2024

^^^Source: S&P Global, Economic Outlook Emerging Markets, 26 March 2024

^^^^Source: fund factsheet, 30 April 2024

Darius McDermott is managing director of Chelsea Financial Services and FundCalibre. The views expressed above are his own and should not be taken as investment advice.

Experts explain the differences between Scottish Mortgage and Ark Innovation and share their preference.

Cathie Wood’s ARK Invest recently launched three of its exchange-traded funds (ETFs) in Europe, including the firm’s flagship strategy ARK Innovation ETF.

The latter is an aggressively-managed fund aiming to identify businesses that can be transformational and have the potential to generate exceptional long-term growth.

As a result of this investment process, the ARK Innovation ETF has proven to be volatile and has struggled in risk-off markets when the growth investment style fell out of favour.

This description may remind UK investors of a fund they are perhaps more familiar with: Scottish Mortgage.

Alex Watts, fund analyst at interactive investor, said: “There are some similarities in philosophy and positioning. Both funds take unconstrained approaches to investing in disruptive businesses that are driving innovation and are at the helm of cutting-edge and growing themes.

“This naturally leads them to invest in higher-multiple growth stocks, compared with more conventional and benchmark conscious peers.”

Despite their similar high growth approach, ARK Innovation and Scottish Mortgage differ in many ways too. As an investment trust, Scottish Mortgage has access to additional tools, such as the ability to leverage its portfolio and hold unlisted assets. It is also subject to a premium/discount mechanism, offering investors the possibility to buy assets below their net asset value. As an exchange-traded fund, ARK Innovation does not have access to these instruments.

They also diverge in their respective investment strategies: ARK employs a more active trading approach, whereas Scottish Mortgage uses a buy-and-hold strategy.