The manager of the Stonehage Fleming Global Best Ideas Equity fund explains why quality has a price and why he does not believe in value investing.

Everyone makes mistakes and has regrets, which is true of even the most seasoned investors such as FE fundinfo Alpha Manager Gerrit Smit. His greatest career regret is not having paid up for high quality businesses such as Apple, because he thought they were overvalued at the time.

From this experience, Smit has concluded that growth investors should be prepared to pay rich valuations at times to participate in some of the world’s most promising companies.

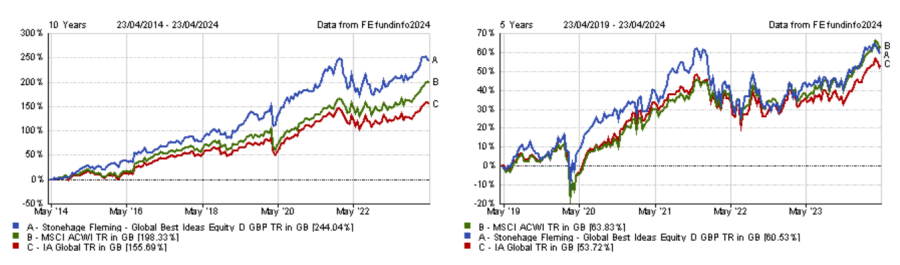

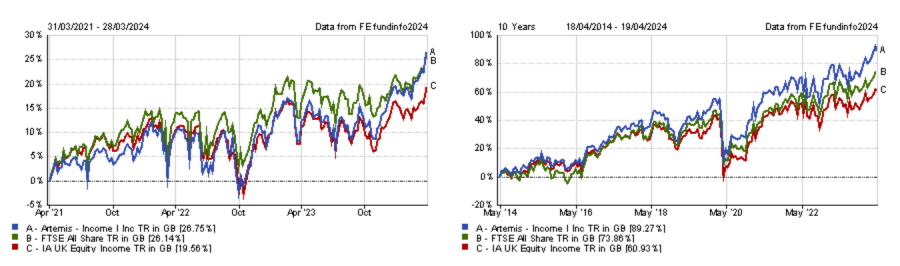

Smit has managed the Stonehage Fleming Global Best Ideas Equity fund since its inception in August 2013. The fund strongly outperformed the MSCI All Country World Index over the past decade but has delivered benchmark-level returns in more recent years. Overall however, the fund has comfortably beaten its sector and benchmark by buying quality companies and holding them over the long term.

Performance of fund over 10yrs and 5yrs vs sector and benchmark

Source: FE Analytics

Below, Smit dissects his performance and explains why investors have to accept that quality has a price.

Could you explain your investment strategy?

We aim to hold the world's best of breed, highest quality businesses. Each one has to have a strategic competitive edge. Lastly, they have to be attractively valued.

We emphasise having conviction in the quality of the management team. We spend a lot of time trying to understand the culture of a business and how management is orientating the business for sustainable growth over the long term.

In essence, we look to buy and hold the world's best businesses for an indefinite period.

That makes the fund a strong candidate for any investor looking for a conservative equity exposure that can be held continuously.

How important are top-down considerations in your investment process?

Our process is completely bottom up: we identify good companies that can keep growing. However, that growth depends on what happens in the world.

So it’s a combination of looking for the right company and understanding the macro-economic environment.

Along with that, we try to understand capital markets to identify when it would be a good time to buy a business and when not.

The fund has outperformed the MSCI World index over 10 years, but not over five. Why is that?

The fund is not always going to outperform. Over the past five years, the technology sector has done exceptionally well. We're not a technology fund, so we didn't keep up with that. However, when technology is underperforming for a certain period, the chances are that we will be outperforming.

However, an important point to make is that the fund has added value over the index after costs, with a level of risk below that of the market over the long term, because it is made of very high quality companies.

What have been the best and worst performing stocks in the portfolio over the past 12 months?

There are two ways of putting it: the stock that had the best performance and the stock that made the greatest contribution.

In terms of the best performance, it was Amazon, but in terms of contribution, it was Alphabet.

Alphabet and Amazon were the fund’s second and fourth largest holdings as at 31 March 2024, worth 7% and 5.5% of the portfolio, respectively. Alphabet rose 54% during the 12 months to 24 April 2024, while Amazon is up 72.2%.

The worst performer on both fronts has been Estee Lauder, which is down 40.4% over the past year.

Performance of stocks over 1yr

Source: FE Analytics

What is your outlook for the global equity market for the next five years?

Clearly, companies are sensitive to the economic and geopolitical circumstances, but I do believe that businesses make the economy rather than the economy making the business.

What’s more, this is the asset class that exposes you directly to the ability of humankind to create. There are not many other asset classes for which we could make that point.

Over the longer term, equities have delivered about an 8% per annum compounded return. I cannot find many reasons to believe that cannot continue to be the case, on the condition that you identify the winners. You cannot simply believe all equities will give you that type of return.

What are the greatest risks facing the equity market?

I perceive myself to be an optimist, but I do worry a lot, so I'm a very conservative optimist.

If I had to condense my concerns into a single issue, it would be the level of US inflation and the level of US interest rates. I emphasise the US, because capital markets anywhere in the world follow what happens in the US.

Also, one has to take geopolitical issues into account. One cannot ignore what's happening in the Middle East.

Along with geopolitical issues, there are developing sanctions in different sectors and industries and between certain countries.

As an investor, what are your biggest sources of pride and regret?

My biggest pride is that, despite being a conservative investor, the fund has been able to do better than the index. At times that has meant making difficult calls. For example, last year, the world thought Google was going to find it difficult to grow because of new competition from Open AI. We trusted the management and made the call to do nothing.

Most of my regrets involve not having been willing to pay up for some high quality businesses because I thought they were overvalued. From that, we've learnt that you cannot expect to get a good business at a low valuation. You have to be realistic and you have to be willing to pay for a good business.

For example, we missed Apple 10 years ago because we thought it was fully valued, but it has done well since. We still do not hold it. We have some reservations about the sustainability of the top line growth. It is probably one of the best managed businesses, but for four quarters in a row last year, the top line didn't grow. It's difficult for a management team to keep increasing the earnings if the top line doesn't grow.

Does that mean you don’t see any merit in value investing?

In a low growth economic environment, the typical value stock, let’s say tobacco, is not going to grow. It's trading at a low multiple and a higher dividend yield.

So the question may be: why not buying this tobacco stock for the dividend yield? We're not convinced that this dividend can grow forever and therefore inflation may erode the income that you think you're getting. That's the main issue.

If you buy something because it’s cheaply valued and, therefore, seems to be attractive, chances are that there's something wrong in the business.

What do you enjoy doing outside of fund management?

I'm fond of travelling and music and I read a lot. Very often, the three of those go together.

Earnings results: Alphabet and Microsoft shine through the macro uncertainty.

The share price of Google parent Alphabet jumped 10% in today’s pre-market trading, following the best set of overall results it has ever released and the announcement of a dividend program of $0.20 per share.

According to Gerrit Smit, manager of the Stonehage Fleming Global Best Ideas Equity fund, this development “proves the company’s stature as one of the quality leaders in the global digital revolution”.

“With its advancements in generative artificial intelligence (AI) already showing improved engagement and advertising performance, the business is firing on all of its many cylinders, resulting in constant currency revenue growth of 16%. It is also pleasing to see the 28% revenue growth in Google Cloud with a multiple increase in profitability,” he said.

“Within a rapidly changing digital environment, it has been able to increase group profitability with a 4% increase in operating margin. Our long-held view that Alphabet can later become a dividend stock also got validated.”

Alphabet’s share price

Source: Google Finance

Microsoft also filed strong earnings and shot up 4% in after-hours trading, reliably delivering well on both organic growth and profitability, as Smit noted.

“The main features are its AI demand resulting in Azure Cloud growth of 28% and a further 2% basis points increase in profitability,” he said. “We perceive Microsoft as the staple of the digital world.”

The tech giants' surge injected a much-needed boost after Meta's cautious forecast failed to inspire confidence, SPI Asset Management’s Stephen Innes noted.

“Tension was taut following a rough day for Meta, which unnerved investors with its cost outlook and capex plan, both of which underscored just how expensive building the future is likely to be,” he said.

Another disappointment had come from the US GPD reading for the first quarter but despite prevailing macroeconomic unease, Alphabet and Microsoft's earnings reports shone through.

"Alphabet, for instance, experienced its most robust top-line growth in two years, announcing not only its inaugural dividend, but also a $70bn stock buyback,” said Innes.

“This news exceeded the expectations of even the most discerning ears.”

After a decade out in the cold, will value managers get their moment in the sun?

Value investing has outperformed growth over the very long term but has spent much of the past decade in the doldrums.

The difference between the valuations of growth and value stocks is more extreme now than at the height of the dot.com bubble, according to Simon Adler, who co-manages the Schroder Global Equity Income and Schroder Global Recovery funds.

Sources: JP Morgan Asset Management, LSEG Datastream and MSCI, data as of 24 Apr 2024

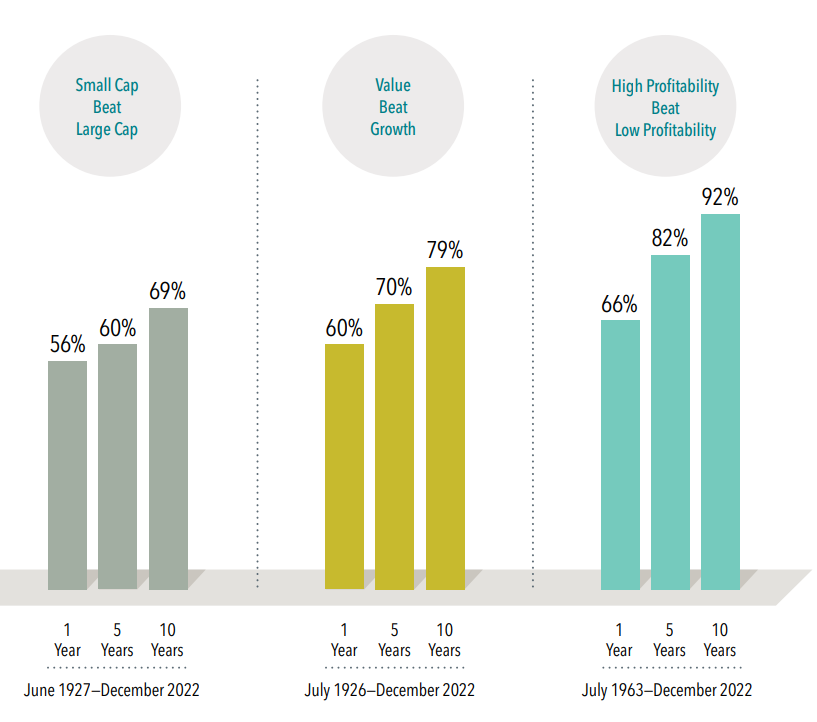

The undisputed fact that value stocks are deeply out of favour comes despite ample evidence that value beats growth over the very long term.

In fact, Dimensional Fund Advisors analysed a myriad of factors and styles going back decades and discovered that only three consistently work: value, the small-cap premium and high profitability stocks outperforming low profitability stocks.

Frequency of premium outperformance

Source: Dimensional Fund Advisors

That doesn’t mean value will beat growth every year or even every decade, as seen from the past 10 years.

Value vs growth over 10 years

Source: FE Analytics

The investment management industry – and human nature more generally – suffers from a recency bias. After watching growth stocks maintain the ascendancy for most of the past decade, it would take a brave investor to bet the farm on value. Not least because artificial intelligence (AI) and technological innovation, which favour growth stocks, are going nowhere.

This is true across most regions. FE fundinfo Alpha Manager Nitin Bajaj, who runs Fidelity Asian Smaller Companies and Fidelity Asian Values, said it has been a decade of “swimming against the tide” despite evidence that small-cap value stocks in Asia grow their earnings faster, as the chart below shows.

Asia ex-Japan: Earnings and returns by style

Sources: Fidelity International, LSEG DataStream, 19 Apr 2024

Nonetheless, fortunes have reversed, even in recent times. Growth sold off in 2022 as the rapid interest rate hiking cycle drove up borrowing costs and the tech sector endured a bear market. Value stocks proved more resilient through this torrid period for equities, highlighting the importance of style diversification, as the chart below shows. Value stocks also rallied sharply after ‘Vaccine Monday’ in October 2020.

Value vs growth over three years

Source: FE Analytics

Yet last year, AI advances put growth and tech firmly back on the agenda.

All this has left the prices of value-oriented stocks languishing in the doldrums. Adler argues that, from such a low starting point, there is plenty of upside potential on a five-year view and attractive valuations alone should justify the inclusion of a value fund in a well-diversified portfolio.

Adler believes it is futile to search for a catalyst that could trigger a value rally or to try timing the market because stock markets move so quickly that investors who wait on the sidelines are likely to miss the start of the next rally.

Other industry participants more inclined to look for catalysts claim that the current macroeconomic environment of high inflation, high rates and resilient growth should favour sectors typically considered the purview of value investors, such as financials.

Furthermore, the unloved UK stock market, whose sector composition (financials, energy and commodities) has more of a value bent to it than the tech-oriented US, seems to have finally turned a corner and hit record highs at the start of this week.

One benefit of all this for value managers – especially those focused on the still-cheap UK – is that they can snap up high-quality companies at egregiously low prices.

Jonathan Winton, co-portfolio manager of Fidelity UK Smaller Companies and Fidelity Special Situations, said: “As a value investor, you really do not have to sacrifice quality at the moment and that’s not something I think value investors have been able to say over the past few decades.”

The average company is his portfolio is trading at 9-10x earnings. “These are businesses that we think can grow and generate decent and improving returns,” he said. “And we're not having to take the balance sheet risk that you might have had to if you wanted to find things that were very cheap in the past.”

Ultimately, the take home for investors is to check the style biases of any equity funds they hold and ensure they have a balance of value managers – bargain hunters who invest in underappreciated stocks they hope will recover – and growth managers, who buy great companies they think will exceed expectations.

Of course, there are a multitude of styles falling in between those extremes (for instance GARP, which stands for growth at a reasonable price, in other words fund managers who want to own great companies but do not wish to pay too high a price for them).

But the message stays the same: combining managers with divergent styles puts investors in good stead to withstand unpredictable market movements and benefit from a mean reversion in style-based performance if and when it does eventually happen.

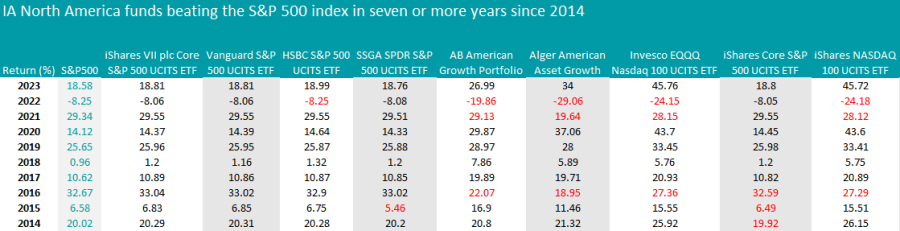

US equity ETFs have proved more reliable than active managers since 2014.

Investors who like steady strategies with predictable results should stick to exchange-traded funds (ETFs) when investing in US equities, data from FE Analytics shows.

Two trackers in particular – the iShares VII plc Core S&P 500 UCITS ETF and the Vanguard S&P 500 UCITS ETF – have outperformed the S&P 500 every year since 2014, something no other fund in the IA North America sector achieved

Being passive in nature, these ETFs are designed to replicate the S&P 500 so their tracking error is very small. However, their returns have been slightly better than the index every year and their fees are much lower than actively-managed funds.

This has been a decade in which the highly-concentrated S&P 500 – the most common benchmark in the IA North America sector – shot the lights out, making it a difficult hurdle for active managers to match. Large-caps have outperformed small- and mid-caps in recent years too, especially in 2023 when the ‘Magnificent Seven’ dominated – a factor that has gone against active mangers who tend to hunt for undiscovered opportunities lower down the cap spectrum.

Launched in 2010, the iShares portfolio is the bigger of the two passive giants, with £66bn of assets under management (AUM) compared to Vanguard’s £40bn.

The latter was recommended by FE Investments analysts for offering “great benefits” to end investors, including an ongoing charge of just 0.07%, made possible through Vanguard’s corporate structure and economies of scale, which facilitate heavy cost-cutting.

Both funds have a FE fundinfo passive Crown Rating of five – the highest score.

Source: Trustnet. The red highlights indicate underperformance against the specified benchmark.

Although the table above is full of passive strategies, AB American Growth Portfolio and Alger American Asset Growth are the exceptions and have outperformed in seven of the past 10 years.

The £5.7bn AB American Growth Portfolio is co-managed by Frank Caruso, John H. Fogarty and Vinay Thapar, who invest in 55 US large-cap companies and charge 0.94%.

The top 10 holdings make up 50% of the fund and include five of the Maginficent Seven stocks, leaving out Apple and Tesla. In the past 10 years, its performance has moved in tandem with the S&P 500 index 91% of the time.

Alger American Asset Growth is a much smaller vehicle (£307m) under the responsibility of Patrick Kelly, Ankur Crawford and Dan C. Chung.

Based in New York, the team focuses on companies with rapidly growing demand, strong business models and market dominance, or where the managers can find catalysts that could drive additional growth, such as new management, product innovation or M&A activity.

The fund charges a 1% management fee and was 90% correlated to the S&P 500 during the past 10 years.

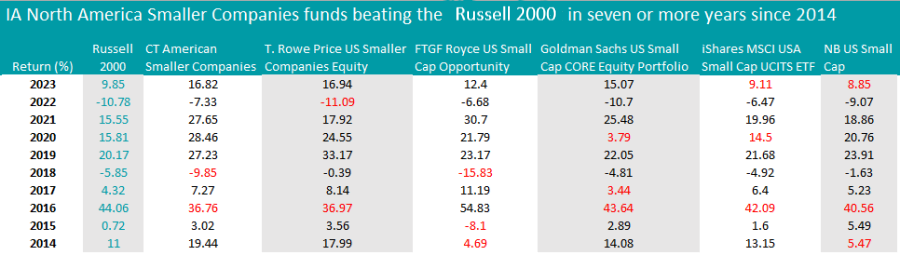

Active managers achieved more success in the IA North American Smaller Companies sector, where CT American Smaller Companies and T. Rowe Price US Smaller Companies Equity beat the Russell 2000 index for eight of the past 10 years.

Run by veteran manager Nicolas Janvier, the £946m Columbia Threadneedle Investments (CTI) fund was recommended by FE Investment analysts for the lead manager’s experience, CTI’s extensive analytical resources in New York and Boston, and the focus on bottom-up stock picking.

Limits are placed on the fund’s sector and factor bets, which “allows for more consistent performance relative to the small and mid-cap market, regardless of the stylistic and macroeconomic environment”, FE analysts explained.

Since 2021, the strategy has decoupled from its benchmark, the Russell 2500, and its average peer, keeping well ahead since then. It achieved a 249% return over the past 10 years against a sector average of 184.4%.

Its largest exposures are to industrials (19.9%), consumer products (17.9%) and telecom, media and technology (16.3%).

Source: Trustnet. The red highlights indicate underperformance against the specified benchmark.

The strategy shares the podium with the much larger £2.8bn T. Rowe Price US Smaller Companies Equity fund managed by Curt Organt and Matt Mahon.

While they prefer a slightly different sector allocation, favouring services (20.5%), media and tech (17.5%) and basic materials (15.3%), the two funds are 93% correlated to each other.

Another difference is T. Rowe Price’s small off-benchmark bet on European equities (1.4%), absent in the CT American Smaller Companies fund.

This article concludes our series on consistency. In previous instalments, we covered: Asia, Emerging Markets, IA Global, Europe, IA UK Equity, IA UK Equity Income, UK Small Caps, UK bonds, cautious funds, balanced funds, adventurous funds, technology, healthcare and financials.

The risk/reward balance is still in favour of holding TSMC.

Filtering out noise and disregarding short-term headlines are among the hardest challenges facing investors, but it’s where the noise is loudest that skilled fund managers see opportunities instead of pitfalls.

One example of a good investment case undermined by an unhelpful narrative is Taiwan Semiconductor Manufacturing Company (TSMC), according to Paul Flood, co-manager of the £2.2bn BNY Mellon Multi-Asset Growth portfolio.

Investing in China and Taiwan is perceived as particularly risky due to geopolitical tensions in the region, but at the beginning of this year, Flood went against the grain and added to TSMC exactly at peak noise, which he identified as a good entry point.

“During the Taiwanese elections [in January 2024], the narrative around China invading Taiwan led to an opportunity as the valuation came back by a long way,” he said.

“While we are paying 30 times earnings for high-growth US technology companies, we can pick TSMC up for low-to-mid-teens multiples and we’re buying a company that creates most semiconductors that we find in all our products.”

The fund’s weighting to the company went from 1.3% at the end of 2023 to 1.9% as at the end of February 2024, with the position then being worth £41.3m. Since the beginning of the year, the stock has grown 32%.

Performance of stock over the year to date

Source: Google Finance

From Flood’s risk/reward perspective, the scale is still tilted in favour of TSMC.

Approximately 90% of the world's high-end semiconductor content is made in Taiwan. If geopolitical events cut off access to Taiwan’s advanced chips, everything from electric vehicles (EVs) to hedge trimmers would be impacted, as the scarcity at the high-end of the market would trickle down through the whole supply chain, including to lower-quality chips.

“If China does invade Taiwan, TSMC is going to be the least of our problems, it will impact all other companies that we invest in on a global basis,” he said.

“If you can't get semiconductor content, how are you going to build things? Apple won’t be able to build mobile phones, Microsoft isn’t going to build out the cloud, and Volkswagen will stop making cars. Semiconductor content powers the world.”

Taiwan’s flagship also stands to benefit from competition between the great powers to ensure the security of semiconductor supply.

“TSMC has tax benefits and subsidies around the world as the US, Japan and Europe need to power everything from EVs but also the military side of things as well,” he noted.

Earlier this month, the US government announced a $6.6bn grant to help TSMC build three factories in Arizona.

Another area where Flood is poised to take advantage of market noise is the US, particularly around the upcoming elections and the future of the Inflation Reduction Act, with its subsidies for US industry.

“We've seen a lot of noise about reducing or getting rid of the Inflation Reduction Act and there's a lot of being said about the differences between Donald Trump and Joe Biden, but there are also a lot of similarities,” he said.

“For example, they are both big spenders, so we don't think that the outcome of the election will change the fiscal debate in the short term. The same capital and the same spending would just be allocated somewhere else. But Republican states are some of the biggest beneficiaries of the Inflation Reduction Act and we think it could be quite hard to unwind that.”

In the US, Flood is particularly bullish on home builders, with the market having “massively underestimated the changing business model” in the sector, as he recently told Trustnet.

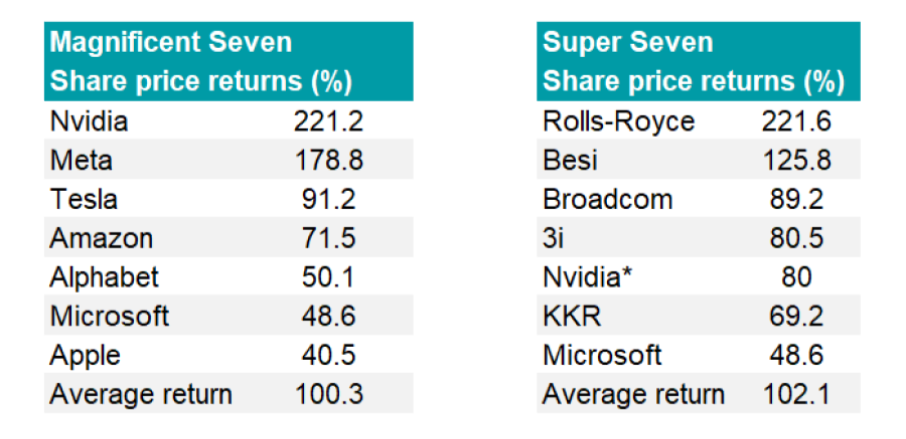

The ‘Super Seven’, a list of top-performing stocks from a range of industries, have more than kept pace with the ‘Magnificent Seven’ and provided a healthy element of diversification to boot.

On the face of it, events in 2023 seemed radically at odds with the notion that successful investing demands balance. Seven mega-cap technology stocks produced 60% of the S&P 500’s total return and accounted for almost a fifth of the MSCI World index in terms of size.

However, as recently as 2022, a different narrative dominated. Big tech giants such as Meta, Nvidia and Tesla experienced significant share price declines, highlighting the volatility that is typically inherent in concentrated investments.

This two-year contrast underscores the timeless adage: ‘Never put all your eggs in one basket’. Even today, with artificial intelligence cementing its status as a go-to theme, there is much to be said for diversification.

Particularly for global investors, who have the widest opportunity set to choose from, portfolio construction should still be a question of both quantity and quality. But amidst unprecedented market concentration, how do we get the balance right?

In search of a golden mean

The debate over diversification has raged for decades, with advocates on both ends of the spectrum.

On one side, we find proponents of the ‘all your eggs in one basket’ philosophy. This is currently en vogue in some circles, with advocates of the ‘Magnificent Seven’, or even a dynamic duo of only Microsoft and Nvidia, championing an unusually narrow focus.

At the other end would be a super-diversified portfolio of hundreds of stocks. Several studies have supported such an approach through the years, most notably in the early 2000s.

As with so many things in life, the ideal very likely lies somewhere between the two poles. It was originally outlined by ‘the father of value investing’, Benjamin Graham, in his two books, ‘Security Analysis’ and ‘The Intelligent Investor’, published in the 1930s and 1940s.

Graham advocated what is sometimes called 'concentrated diversification', which he described in The Intelligent Investor as “adequate, though not excessive”. This, he said, should translate into a portfolio of up to 30 holdings.

This argument is still relevant today. Too little diversification can invite unpleasant surprises, whereas too much can take investors into index fund territory, where the concept of beating the market surrenders to the concept of being the market.

Yet numerical balance is only half the story. Diversification within those holdings is just as crucial.

Casting a wide net

Graham’s stock-picking process was rooted in his defensive tests. He looked for companies characterised by adequate size, financial strength, earnings stability and growth, an established dividends record and moderate price-to-earnings and price-to-assets ratios.

Crucially, the ability to withstand rigorous scrutiny extends beyond the realm of big tech or even the technology sector as a whole. A company does not need to boast a trillion-dollar market capitalisation to be a solid investment.

Consider Tractor Supply Company: founded in 1938, it is a US retail chain specialising in agriculture, gardening and home improvement products, boasting a market capitalisation of around $25bn.

Or take Azelis: established in 2001 and based in Belgium, it has a market cap of around $4.6bn. It provides innovation services in the specialty chemicals and food ingredients industry.

We initiated or strengthened positions in both these holdings in late 2023. Why? Ultimately, we search for good businesses capable of contributing to a portfolio that is not reliant on any given theme, factor or macroenvironment.

In essence, balance in this context comes from giving due thought to different sectors, geographies, market caps and other considerations.

The proof is in the pudding

Of course, the argument for balance would seem lacking if a select group of theme-centric stocks were to constantly outperform. However, the events of 2022 dispelled that notion.

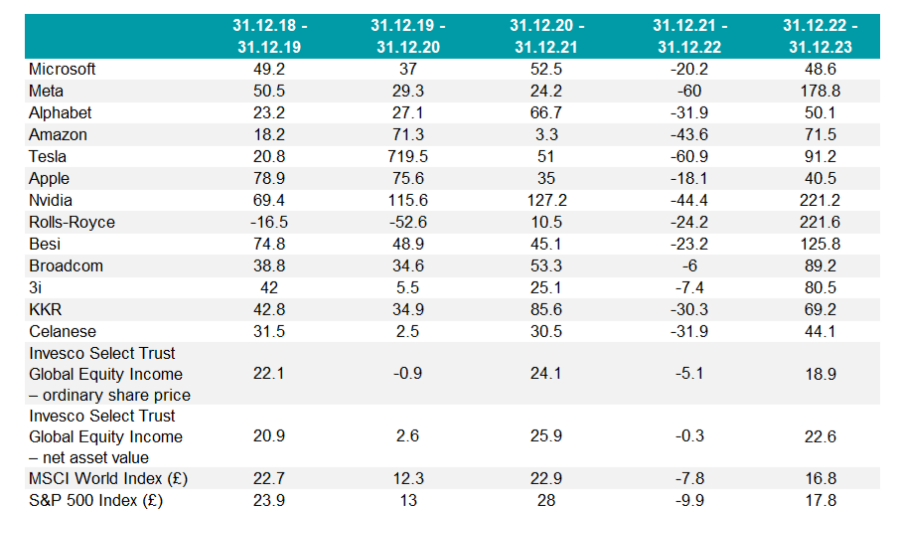

Perhaps it’s time for reflection. Collectively, the seven best-performing holdings in the Invesco Select Trust plc Global Equity Income share portfolio in 2023 – our very own ‘Super Seven’ – more than kept pace with the Magnificent Seven in terms of total shareholder return, as the tables below shows.

Naturally, big tech was represented in our line-up. Yet it was just one element among a much broader – and, in our opinion, much healthier – mix of industries, regions, capitalisations and investment styles.

Magnificent Seven versus Super Seven in 2023

Source: Bloomberg, data to 31 Dec 2023 in sterling terms

Source: Bloomberg, data to 31 Dec 2023 in sterling terms

* Nvidia was held in the portfolio from the summer of 2022 to April 2023

Magnificent Seven versus Super Seven – rolling 12-month performance

Source: Bloomberg, data to 31 Dec 2023

Source: Bloomberg, data to 31 Dec 2023

Stephen Anness is lead manager of the Invesco Select Trust plc Global Equity Income share portfolio. The views expressed above should not be taken as investment advice.

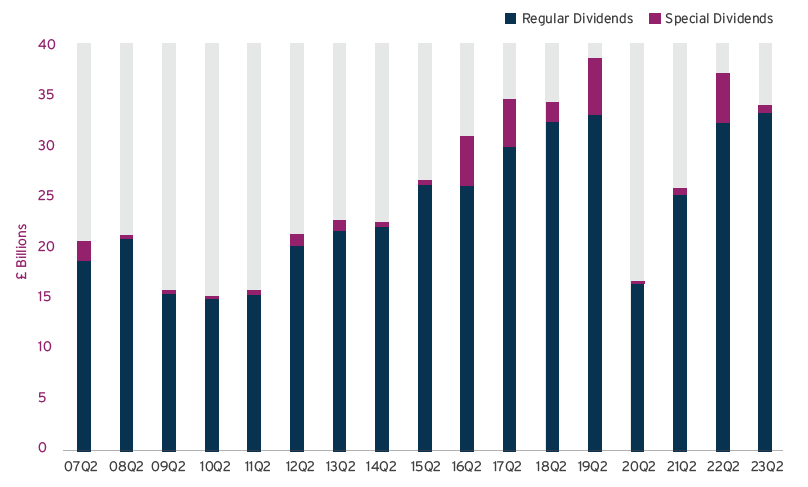

One-off payments will drive dividends in 2024, according to Computershare’s latest Dividend Monitor.

UK dividends increased 4.9% to £15.6bn in the first quarter of 2024, the latest Computershare Dividend Monitor report revealed.

However, most of this growth was driven by one-off payments. Underlying dividend growth remained steady at 2% – a “healthy but unexciting” trend, which will continue for most sectors throughout the year, reflecting a sluggish global economy, Computershare said.

With prospective yields on UK equities stuck at 4%, income-seeking investors may gravitate towards higher-yielding bonds and cash, said David Smith, manager of the Henderson High Income Trust.

“The UK equity market is attractively valued but cash and bonds are now greater competition for investors’ capital. The advantage that equities provide is inflation protection through dividend growth, but that is likely to be relatively low this year,” he said.

But there is light at the end of the tunnel for equity income investors. Things are expected to improve throughout the second half of this year as cost pressures ease, interest rates are cut and economies start to recover, driven by real wage growth and a more buoyant consumer.

Computershare experts upgraded their headline forecast from £93.9bn to £94.5bn in total payouts for 2024 – a 4.3% year-on-year increase against the previous forecast of 3.7%.

Most of this will be driven again by special dividends, which Computershare expects will be significantly larger than in 2023. Regular dividends are expected to be worth £89.5bn, up 1.5% year-on-year on a constant-currency basis.

UK dividends 2023

Source: Computershare Dividend Monitor

Mark Cleland, chief executive of issuer services for the UK, Channel Islands, Ireland and Africa at Computershare, said: “This modest growth in dividends reflects the earnings picture: cost pressures have eased for many businesses, but the cost of capital has risen sharply, and economic growth is sluggish at best in the UK and in much of the world. This makes it difficult for companies to build earnings momentum, which influences how much boards decide to return to shareholders in the form of buybacks or dividends.”

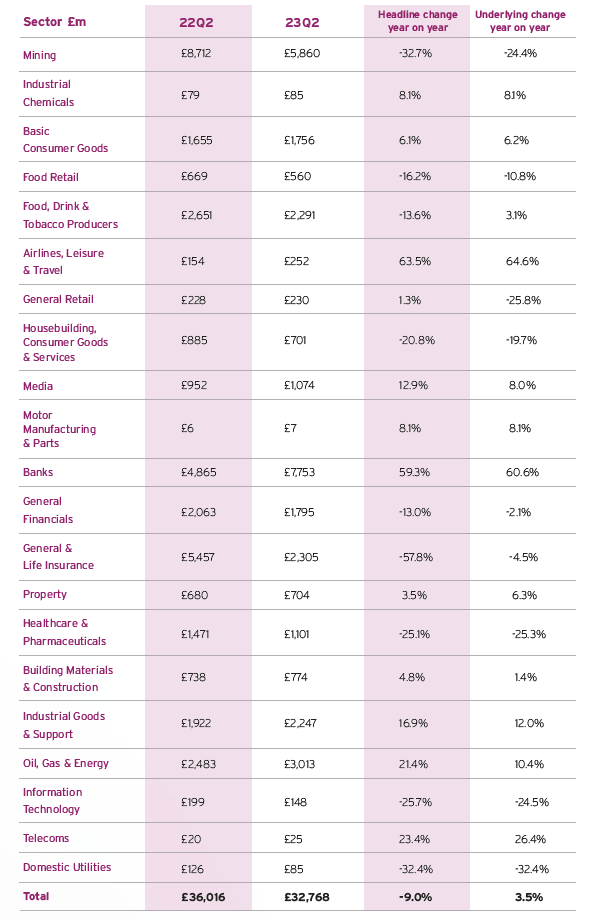

In the first quarter of this year, oil and pharmaceutical companies were among the highest payers, but the strong pound was a hindrance and, in the case of Shell and BP, offset the per-share dividend increases declared by the companies.

For the full year, oil dividends are likely to be roughly flat to slightly ahead, the report read.

“A more modest 2024 for the oil sector removes a significant engine of dividend growth from the UK market this year, after it made a major contribution during its recovery from the cuts made early in the pandemic. However, surplus capital will likely continue to be returned through share buybacks.”

Sterling strength also brought the value of pharmaceutical dividends down 2.9% in the first quarter as AstraZeneca held its payout flat in dollar terms.

Telecoms were also major contributors, but the largest payers, Vodafone and BT, didn’t increase their dividends.

Dividends by sector £m – Q1

Source: Computershare Dividend Monitor

Banks are likely to make the largest contribution to dividend growth in the UK for the third year running, Computershare experts noted.

Virgin Money was the only bank to make a payment during the first quarter, although its payout was reduced due to the impact of rising credit impairments on profits.

Nonetheless, Smith remained positive towards the banking sector. “Having been forced to stop dividend payments during the pandemic, it’s good that banks’ dividends have been restored and grown back to pre-pandemic levels. We expect further dividend growth this year given the rise in profits from higher interest rates have yet to fully flow through to earnings,” he said.

“Despite banking dividends now being better covered by earnings and strong capital positions in the sector, dividends yields are high, offering income investors an attractive opportunity. We believe those dividends should be sustainable, absent a severe recession in the UK.”

Banks have been buying back their own shares extensively, a practice that can have a negative impact on dividend payouts in the short term but should bring long-term benefits, according to James Lowen, senior fund manager of the J O Hambro UK Equity Income fund.

“Over the long term, the anticipated effect is to amplify dividend growth, as there will be fewer shares in issue for a set amount of dividend to be spread across. This is a powerful second derivative effect of buybacks for long-term dividend growth, which we see in numerous stocks.

“Fund dividend forecasts incorporate a shift towards lower dividends and increased buybacks from 2024, signifying a short-term dip but projecting higher returns in the medium term.”

The Rathbone Greenbank Multi-Asset Portfolios avoid companies or issuers that harm people or the planet and proactively invest in companies that do good.

The US government’s high defence budget has caused it to fall foul of Greenbank’s sustainability screens, while only two of the ‘Magnificent Seven’ technology stocks – Microsoft and NVIDIA – made it through the firm’s stringent negative and positive screening process.

Microsoft has a strong sustainability story, with a target to be carbon negative by 2030, said Will McIntosh-Whyte, who manages the Rathbone Greenbank Multi-Asset Portfolios. Furthermore, it plans to remove enough carbon by 2050 to account for its historic emissions.

“It is meeting increased demand for IT infrastructure with more environmentally friendly and energy efficient solutions and it is quite innovative, so it has been trialling having one of its data centres underwater to help with cooling. And it is very good in terms of benefits and employee development programmes,” he said.

When the Rathbone Greenbank Multi-Asset Portfolios were launched in March 2021, NVIDIA was not eligible for inclusion because it derived a large part of its revenues from cryptocurrency mining and gaming.

NVIDIA’s business model has changed since then and it now focusses on advanced chip design, which aligns more naturally with two of Rathbone Greenbank’s eight sustainable investment themes: innovation and infrastructure, and decent work.

If McIntosh-Whyte and co-manager David Coombs want to invest directly in a stock, they have to recommend it to their colleagues at Greenbank (the ethical, sustainable and impact investment team of Rathbones Group) for further analysis and screening. McIntosh-Whyte put Alphabet forward but it failed Greenbank’s tests.

Alphabet has historically had issues with sexual harassment, allegations of discrimination and other employment issues, he explained. In particular, there was severe controversy over allegations of hiring discrimination concerning software engineers in California and Washington. Rathbones also has concerns about digital rights and the responsible management of content.

Alphabet was reluctant to engage with Rathbones when approached to discuss its concerns, which was a red flag.

Rathbones’ core multi-asset funds invest in Amazon and Apple but McIntosh-Whyte decided against including them in the sustainable range because they have not always been at the forefront of positive employee relations.

With Meta, he said it would be difficult to argue how Facebook’s parent company could align to Greenbank’s sustainable investment themes or to the UN Sustainable Development Goals.

“Tesla is slightly different because obviously, from a product perspective, you can see how it might align with sustainability given it is very focused on electric vehicles,” he noted. “We’ve actually always been a bit wary of Tesla from a governance perspective and also from a business model perspective. It’s just not one that we particularly want to own.”

The firm also shies away from US Treasuries. Instead, he has bought dollar-denominated debt issued by supranational institutions such as the European Investment Bank, which behaves in a similar way to US Treasuries. Dollar-denominated 10-year supranational bonds are paying yields north of 4.5%, he said.

Governments must pass three out of four metrics to enable Rathbones’ sustainable funds to buy their bonds: corruption, civil and political liberties, environmental performance and defence spending. The three-year global average defence spend is 2% of GDP, so countries spending more than that are ruled out.

Not only is the US defence budget too high but it also scores poorly on environmental metrics, although its green credentials are improving under the current administration, he added.

The UK passed these tests with flying colours and scored well on the environment as it pushes for a net-zero economy.

Experts compare and contrast the strategies of Smithson and Edinburgh Worldwide and reveal their preferences.

Fundsmith Equity and Scottish Mortgage rank high on investors’ buy lists due to their impressive performance over the past decade.

As a result, fans of the two global large-cap portfolios might also be interested in their small-cap siblings, Smithson and Edinburgh Worldwide.

In theory, small-caps should outperform larger businesses over the long term, although that hasn’t worked out in practice over the past 10 years.

Jason Hollands, managing director at Bestinvest, said: “The past few years have been relatively tough for smaller companies given the disruption of the pandemic, which has been followed by the headwinds of rampant inflation and rising borrowing costs. Small-caps have also been overshadowed by the dominance of US mega-cap growth stocks.”

Performance of indices over 10yrs

Source: FE Analytics

However, with inflation and interest rates past their peaks, now could be a good time to reconsider small-caps. A lower rate environment should boost investors’ appetite for riskier assets, reduce borrowing costs and improve access to capital, all of which bode well for smaller companies.

Below, experts compare Smithson and Edinburgh Worldwide, explain which one they would choose and look at other options in the IT Global Smaller Companies sector.

Two different investment philosophies

Although both Smithson and Edinburgh Worldwide belong to the same sector and share a bias to growth stocks, their investment strategies have little in common.

Smithson follows a quality growth strategy, underpinned by Fundsmith’s mantra: “Buy good companies, don’t overpay, do nothing”.

Key characteristics that the trust’s managers Simon Barnard and Will Morgan look for are high returns on invested capital, high cash conversion and healthy profit margins.

By comparison, Edinburgh Worldwide has a greater focus on earlier stage, faster growth companies and holds a significant proportion in private companies, whereas Smithson has none.

In summary, Smithson favours sustainable growth, whereas Edinburgh Worldwide is more of a high risk, high reward strategy.

Smithson is not a pure small-cap strategy as it includes mid-cap stocks, whereas Edinburgh Worldwide typically holds companies with a market capitalisation of less than $5bn when the investment is made.

Matthew Read, senior analyst at QuotedData, noted that Edinburgh Worldwide is the “most small-cap focused by some margin” in the IT Global Smaller Companies sector, whereas Smithson stands at the opposite end of the spectrum, with the strongest bias to mid-caps.

Another reason why Smithson hunts for opportunities higher up in the market cap spectrum is due to its larger size. Despite being the youngest of the two investment trusts, it has a market value of £2.1bn, while Edinburgh Worldwide has £528m.

“Smithson had a very successful IPO and, through a combination of decent performance and further issuance, it is now the largest fund in the IT Global Smaller Companies sector by some margin,” Read observed.

“Although its closed-end structure allows it to hold the same kind of stocks as Edinburgh Worldwide, for these to make a meaningful impact, Smithson needs to hold much bigger positions and it is easier when trading in less liquid stocks to move the market against yourself.

“It therefore makes sense that Smithson holds larger stocks, but it may miss out on some opportunities as a result.”

Read also noted that Smithson is the most expensive of the two funds, in spite of its larger size, which should be conducive to economies of scale. As of 23 April 2024, Smithson had an ongoing charge figure of 0.9% versus 0.7% for Edinburgh Worldwide.

Another difference is that the small-cap declination of Fundsmith Equity is not geared, whereas Edinburgh Worldwide has a net gearing of 14.8%. This may explain why the Baillie Gifford trust has been more volatile over the past five years.

In terms of performance, both have lagged the MSCI World SMID Cap index over the same period, but while Smithson is still in positive territory from an absolute return perspective, Edinburgh Worldwide is down 26.5%.

Performance of investment trusts over 5yrs vs sector and benchmark

Source: FE Analytics

Which one should you pick?

Due to their distinctly different philosophies, each trust will cater to the needs of different investors.

Hollands said: “Edinburgh Worldwide is more of a ‘punt’ with potential significant upside if the likes of SpaceX IPO at some point, whereas Smithson offers access to a portfolio of high-quality companies that can compound returns over time and would therefore be a more core play in the global small and mid-cap space.

“Which one to invest in therefore depends what type of investor you are, but for me it would be Smithson of the two.”

James Yardley, senior research analyst at Chelsea Financial Services, also prefers Smithson, which his firm uses in the VT Chelsea Managed Aggressive Growth and VT Chelsea Managed Balanced Growth funds.

“Smithson has much better diversification across different sectors and has still delivered a good share price return of over 40% since its IPO, despite a severe headwind to its style in recent years,” Yardley said.

“The trust has had a tough time recently but we think the shares offer very good value at a 10% discount. We believe Simon Barnard and Will Morgan are strong managers and have a good process.”

While he deems Edinburgh Worldwide to be an “interesting” trust, he stressed that it comes with a high degree of risk, with severe drawdowns when things don’t play in its favour. Furthermore, it is heavily exposed to healthcare, biotech and software.

However, QuotedData’s Read prefers Edinburgh Worldwide as he believes it has greater long-term potential due to its exposure to artificial intelligence (AI).

“The market embraced the potential of generative AI last year and this has continued year-to-date and looks like it could be a structural trend for some time,” he noted.

“Edinburgh Worldwide has a significant focus on areas such as technology and healthcare and should be well positioned to benefit as the market’s focus widens beyond the initial large-cap beneficiaries. Smithson should benefit as well but perhaps to a lesser extent.”

Another option for small-cap exposure

Read proposed The Global Smaller Companies Trust as a more neutral option for conservative investors.

The small-cap version of F&C Investment Trust, it does not have any particular investment style or sector bias. It has a broader portfolio and a modest level of gearing, which has historically ensured more stable returns, while offering a small yield of 1.6%.

Read concluded: “The Global Smaller Companies Trust is arguably the safe bet within the global smaller companies space (it has one of the lowest NAV volatilities) but seems less well exposed to the technology-related trends that look like they might be driving markets for some time.”

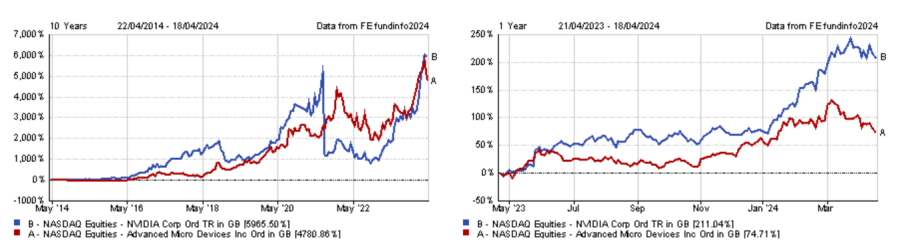

Experts ponder whether AMD could dethrone its larger rival.

Nvidia has been the poster child of the artificial intelligence frenzy, spearheading the accompanying stock market rally.

The stock fell back last week, however, along with the rest of the ‘Magnificent Seven’ (Alphabet, Amazon, Apple, Meta Platforms, Microsoft and Tesla).

But does this sudden change in fortunes mark a turning point for the graphics processing units (GPU) market leader?

The company is due to reveal its cards on 22 May when it will publish its results for the first quarter of 2024-25. Depending on the figures, this may or may not reassure the market that Nvidia can live up to the high expectations surrounding it.

Over the long term, possible threats to the company’s hegemony might include the emergence of a competitor in the GPU market, such as Advanced Micro Devices (AMD).

Zehrid Osmani, head of the Global Long-Term Unconstrained team at Martin Currie, said: “AMD is seen as an alternative company to Nvidia in the GPU segment and could potentially expand its market share from currently c.5% in data centres to 20% over the longer term.”

So should investors consider taking profits from Nvidia and investing in AMD?

Not so fast, said Chris Ford, co-manager of the Sanlam Global Artificial Intelligence fund. While AMD may well gain market share, it remains a “distant second player” to Nvidia, he said.

One of AMD’s issues is that it is spread thinly across both the GPU and central processing units (CPU) markets, where it trails behind Nvidia and Intel, respectively.

AMD is smaller than Nvidia, which means its research and development capacities are more limited, he continued. AMD is also constrained by the necessity to compete with Intel in the CPU space.

These dynamics have “led to a persistent capability for Nvidia to deliver significantly superior operational performance from their chips compared to AMD”, Ford concluded.

Dom Rizzo, portfolio Manager of the T. Rowe Price Global Technology Equity fund, added that chips from Nvidia and AMD are not interchangeable without “a noticeable degradation in performance”.

AMD is still the new kid in town, yet to gain recognition, he continued. “AMD’s product offering is relatively new to the market, so it has to go through testing. It is at a different stage in terms of adoption and acceptance, so it is difficult to make a direct comparison between the two.”

Nvidia has built a software and services ecosystem on top of its chips, which is something AMD lacks, as it has been focusing on a wider range of products.

Performance of stocks over 10yrs and 1yr

Source: FE Analytics

For Allan Clarke, investment manager at Aegon Asset Management, the GPU market bears resemblance to the smartphone market in the late 2000s with Apple and Samsung.

While Apple built an entire software ecosystem attached to the iPhone, Samsung didn’t and ran Google’s Android on its phones.

Clarke said: “That made a huge difference to the way the two companies were able to monetise the mobile market: shareholders in Samsung would have done fine since the start of the smartphone era, whereas shareholders in Apple have done very nicely indeed. Apple managed to extract something like 80% of the value of the mobile-era of computing, with other players fighting over the remaining 20%.

“Nvidia will be looking to achieve something similar from this next era of computing. If it achieves that (and it currently is), then AMD will be among a number of players fighting for the remaining 20%.”

In spite of this, Rizzo believes the GPU segment is growing fast enough to accommodate both companies and that capturing 10% of the market share would be enough for AMD to thrive.

“AMD has forecast the market to grow from $45bn to $400bn between now and 2027. If AMD were to secure 10% of the market in 2027 that is still significant room for them to grow,” he said.

Furthermore, once generative AI moves from training large language models – which requires fast computing power, and therefore heavy use of GPUs – the application of these models (inference) will depend less on fast-compute. This could lead to more extensive use of CPUs, which would play to AMD’s strengths, Osmani explained.

However, he disputed this thesis. “We believe that inference is also very data intensive and therefore will still require fast computing power and fast processing microchips. Therefore, the market might come to realise that the significant need for GPUs is sustained for longer than expected, which would favour Nvidia,” he explained.

While Nvidia has no obvious competitors apart from AMD in the GPU market, it could face external threats, such as from application-specific integrated circuit (ASIC) manufacturers.

Ford said: “They’re designed to address a very particular computational problem and deliver a silicone solution that addresses it.

“One of the problems with that approach is that designing and manufacturing chips is extraordinarily expensive. Ideally, you want to design a chip, which you can then manufacture as many times as you possibly can. That means you need to find particular computational tasks that have huge scale attached to them to develop an ASIC, but there really aren't very many of those.

“You could argue that there are more now than there were 10 years ago, but we believe it will remain somewhat limited. However, if there is an element of competition for Nvidia over the course of the next decade, we think it's far more likely to emerge from the ASIC manufacturers than from AMD.”

Clarke also pointed to the likes of Alphabet, Microsoft and Meta as potential threats because they are looking to design their own chips to reduce their reliance on Nvidia – although he thinks they are a long way off from threatening the GPU giant.

He concluded: “Time will tell, but the current rate of development, product advantage and market position for Nvidia looks formidable.”

The Tokyo Stock Exchange is targeting companies with low valuations and its initiatives should inherently benefit value stocks as Japan’s rally broadens.

It is a year since the Tokyo Stock Exchange (TSE) published new corporate governance guidelines pressing Japanese companies into driving greater capital efficiency and profitability.

Much has happened since. Now it feels the corporate governance movement is firmly embedded and tangible progress has helped to propel the Nikkei and the Topix to new heights. All of this is underpinned by a pivot towards an inflationary economy following decades of deflation, prompting the Bank of Japan to exit its ultra-easy monetary policy stance last month.

All eyes are now on the annual general meeting (AGM) season in June when more corporates are set to disclose their plans to improve shareholder value. While we are not expecting overnight change, we are anticipating some significant announcements.

Plenty of room to improve

While disclosure rates so far have been impressive, 35% of corporates have still not responded to the TSE’s demands to outline their initiatives. These laggards find themselves firmly under the microscope and must explicitly outline the reasons for not making the required changes.

The TSE continues to ramp up the pressure in other ways. Earlier this year it published a detailed set of requests alongside case studies of companies that had made a head start on improving their corporate governance.

It now publishes a monthly list naming those companies which have disclosed their initiatives – thereby exposing those which have failed to do so – which acts as an important incentive for management teams. The shame associated with not disclosing adequate initiatives weighs heavily on firms and executives.

It is not, however, all stick and no carrot. Positive announcements have generally seen strong reactions. Research by Goldman Sachs has highlighted how companies’ willingness to respond is reflected in their share price performance. As of the end of 2023, an equal weighted basket of the 810 TSE Prime Market names that had responded to the TSE’s request outperformed non-responders by around 12%.

Activist pressure

While there have been many examples of improvements since the turn of the year, with cross shareholdings – a longstanding bugbear of investors in Japan – increasingly under the spotlight, there is mounting pressure for these to be reduced at a faster rate. Some of this pressure came from activists. Indeed, the first quarter saw a 156% year-on-year increase in the number of activist events.

Activists have been relatively successful in cases where they specifically target outsized cross shareholdings. For example, in early 2023, Dai Nippon Printing announced that it would conduct a record share buyback of around $2.2bn and aim to generate $1.6bn in cash through the sale of cross shareholdings. This followed reports that an activist investor had built a 5% position in the stock with the goal of encouraging similar initiatives.

There are many such examples, and they often encourage rival firms, fearful of being targeted themselves or seeming inactive relative to a competitor, to pre-emptively act themselves.

Where next?

While progress to date has been encouraging, a large portion (43%) of listed stocks on the TSE Prime market still trade below book value, a far higher percentage than rival markets. For comparison, just 2% of the S&P 500 and 23% of the Euro Stoxx trade on a sub 1x price-to-book (P/B) valuation.

So far, many companies have focused on low-hanging fruit to improve their return on equity (ROE) – easy-to-achieve initiatives like the reduction of cash and/or cross shareholdings to enhance balance sheet efficiency.

At the forthcoming AGM season, some additional announcements of this ilk are expected. To some extent this is already being reflected in the share prices of the most likely candidates for change.

But the average Japanese corporate balance sheet remains unlevered and cash rich. The percentage of companies with net cash on their balance sheet remains high at 46% versus 14% in the US and 21% in Europe. That means there is plenty of work left to do on this front.

However, the more radical improvements to underlying profitability and the successful reform of cost structures, business models and business portfolios will take time to implement. But these longer-term solutions should extend the longevity of corporate governance reforms as an investment story.

A broader rally

With a policy that is generally targeting companies with low valuations, the TSE’s initiatives should inherently benefit value stocks.

Yet very much like the US, Japanese market breadth over the last 12 months has been narrow.

Performance has largely been driven by a select number of top cap value stocks as well as some technology stocks – even though these two areas of the market are expected to benefit less from the corporate reform push.

The reason is that foreign investors, who have flocked back to Japan, have focused on a small collection of well-known companies. With some stocks now looking overvalued, we expect the rally to broaden to more value names.

Moreover, the TSE has emphasised the need for the wider market to focus on long-term improvements to shareholder value; simply reaching 1x P/B – something some companies will achieve simply through market appreciation – is not going to be enough.

A year ago, we said ‘this time is different’. Given the disappointments of the Abenomics era, this was a bold claim. But the TSE has proved it really does mean business – and corporate Japan, long so adept at resisting change, is finally listening.

Emily Badger is a portfolio manager in the Japan CoreAlpha strategy team of Man Group. The views expressed above should not be taken as investment advice.

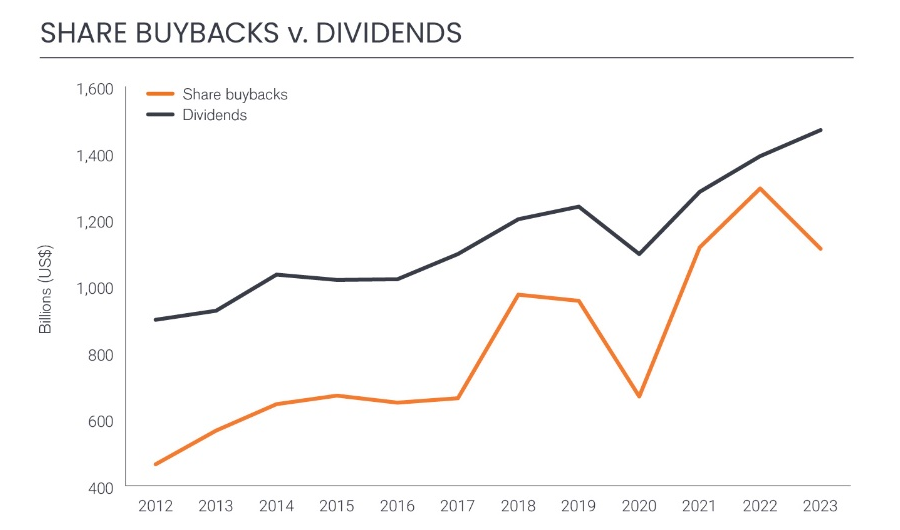

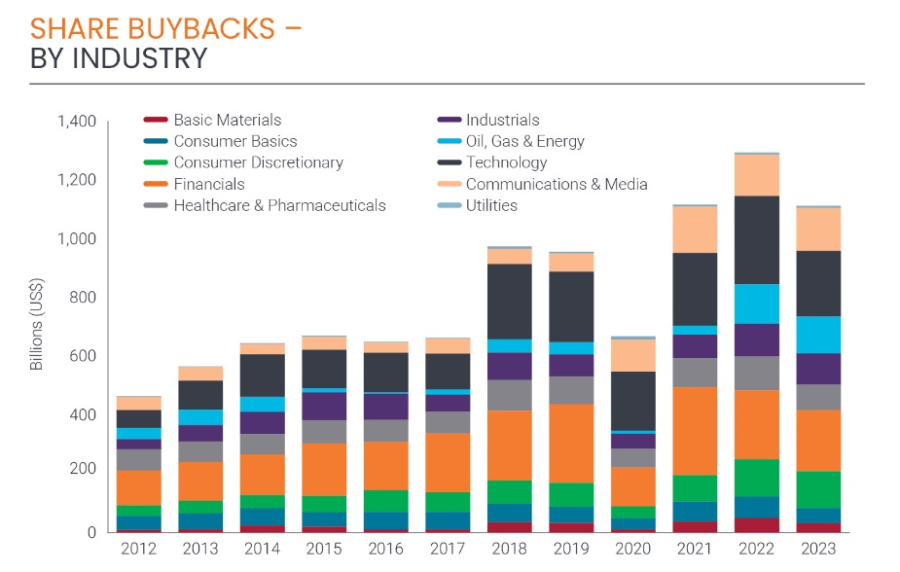

Share buybacks fell 14% year-on-year.

Companies focused more on dividends than share buybacks in 2023, according to data from Janus Henderson’s Global Dividend Index, with the $1.1trn spent on repurchasing shares last year some $181bn lower than in 2022.

This is a decline of 14% year-on-year and means 2023’s buybacks total was below even the 2021 level, although it remains far ahead of pre-pandemic marks.

Ben Lofthouse, head of global equity income at Janus Henderson, said higher interest rates have played a role in the decline of share buybacks.

“When debt is cheap it makes sense for companies to borrow more (as long as they borrow prudently) and use the proceeds to retire expensive equity capital,” he said.

“With rates at multi-year highs, that calculation is more nuanced; some companies are paying down debt at this point in the cycle, using cash that might otherwise have gone to buybacks.”

Buying back shares is a key tool for companies to reduce the amount of stock in issuance and therefore enhance the share price. It is a way of returning value to shareholders through capital gains.

Some prefer this to dividends, which is income paid out to investors, as share buybacks can be more flexible; whereas once a company starts paying dividends, shareholders expect to be paid at least the same amount every year – if not for the income to increase.

Source: Janus Henderson Global Dividend Index

Lofthouse said: “Many companies use buybacks as a release valve – a way of returning excess capital to shareholders without setting expectations for dividends that might not be sustainable long term. This is especially appropriate in cyclical industries like oil or banking.

“That flexibility explains why buybacks are more volatile than dividends. It also means there is no real evidence that buybacks are taking over from dividends.”

US companies bought the most shares last year. American companies are known for preferring buybacks to dividends and they accounted for some 70% of all share repurchases last year, with a total of $773bn.

This was down some $159bn on the previous year (or 17%) but remained 1.2x larger than the value of dividends paid by US companies.

Source: Janus Henderson Global Dividend Index

Outside the US, companies in the UK were the biggest buyers of their own shares, accounting for $1 in every $17 of the global total in 2023, the report found.

A total $64.2bn in repurchases was 2.6% lower year-on-year and equalled 75% of dividends paid, with oil major Shell leading the way. It is the largest non-US buyer of its own shares, (accounting for almost a quarter of the UK total).

However, the firm cut back last year, as did the likes of BP, British American Tobacco and Lloyds, among others. This was counterbalanced by an increase in share buybacks from banks such as HSBC and Barclays.

Share buybacks are also becoming more prominent in Europe, the report found, where the total paid rose 2.9% to $146bn in 2023, although it remains less of a tool for Asian stocks.

Dividends or buybacks?

Lofthouse noted the relative size of buybacks when compared to dividends shrank in every region except Japan and the emerging markets, suggesting dividends remain the most coveted option by companies and their shareholders.

However, he was quick to ward investors off assuming the trend for share buybacks was over.

“It’s tempting to extrapolate a new trend of decline for buybacks. But one down year from multi-year highs is not evidence that this is happening. It is all about companies finding the appropriate balance between capital expenditure, their financing needs and shareholder returns via dividends, buybacks or both,” he said.

The FTSE 100 is expected to leave Monday’s record close in the dust and climb to the dizzy heights of 8,500 to 9,000 this year.

The FTSE 100 hit a milestone on Monday, closing at an all-time high of 8,023.87, and experts expect the UK stock market to continue gathering steam.

Axel Rudolph, a senior market analyst at IG Group, thinks the FTSE could notch up to 8,300 this summer before flying as high as 8,500 by year’s end, while Darius McDermott, managing director of Chelsea Financial Services, believes 9,000 could be possible.

AJ Bell investment director Russ Mould stuck at a more conservative forecast of 8,300, arguing that ample dividend payments and record amounts of share buybacks are signs of corporate confidence.

Rudolph said: “Since the FTSE 100 is on track for its third consecutive month of gains, helped by foreign investors buying undervalued UK shares and companies, a technical analysis upside target called the 161.8% Fibonacci extension around the 8,300 mark may be hit over the next few months.”

A 161.8% Fibonacci extension is used by technical analysts to forecast price targets when financial markets hit all-time highs and is a 1.618 times price projection of a previous move.

“The depreciating pound sterling, making foreign purchases of UK shares cheaper to buy, is expected to underpin the UK blue-chip index as well,” Rudolph continued.

“By year-end the 8,500 mark may be reached, especially if the UK economy starts to grow again amid future interest rate cuts by the Bank of England, the first of which is expected to be seen in August.”

McDermott agreed and was even more bullish. “We like the UK and could easily see the FTSE 100 moving towards 9,000 by year-end if commodity prices continue their upward trajectory. There is also a renewed political realisation that the UK market is falling behind and the government has finally recognised it needs to do more to support its domestic stock market,” he said.

Taking a step back, the Covid-19 pandemic gave companies the chance to press the reset button on their dividend policies and adjust them to more sustainable levels.

“Now, with healthier cash flows, these businesses are using those resources to repurchase their own shares at historically cheap valuations, further boosting stock prices,” McDermott said.

“Increased geopolitical tension is also increasing commodity prices, benefiting the FTSE’s energy and mining stocks.”

Jason Hollands, managing director at Bestinvest, agreed. “The UK equity market is home to a significant aerospace and defence sector where stock prices have soared, reflecting ongoing global crises and increased defence spending. The standout performer here has been Rolls-Royce, whose shares are up 167% over the past 12 months, matching the aggregate returns from the Bloomberg Magnificent Seven Index of US mega-caps.”

Monetary policy divergence and US dollar strength have contributed to recent gains as well, he continued. “Global investors now anticipate two rate cuts from the Bank of England this year, as the inflationary environment looks more benign than it does in the US, where a possible reverse-ferret rate hike is back on the cards at the Fed.”

The domestic economy, meanwhile, is improving. “An unexpected rise in the composite Purchasing Managers Index in April suggests the economy grew faster at the start of the second quarter. GDP data earlier this month confirmed that the technical recession that the UK entered at the end of last year is almost certainly over and this signal might have boosted investors’ faith in UK equities,” Hollands explained.

Emma Moriarty, an investment manager at CG Asset Management, sees the next general election as a catalyst that “might resolve some of the more structural political uncertainty that has created an overhang for the UK markets”.

Despite breaking records, UK equities still appear attractively valued compared to other developed markets, Hollands pointed out. “UK shares are trading at a price-to-earnings (P/E) ratio of 11x, a 37% discount to global equities, and well below their long-term median valuations.”

Mould added that even if the FTSE 100 advanced to 8,350, the index would still be on a P/E of 12x and a yield of 3.9%.

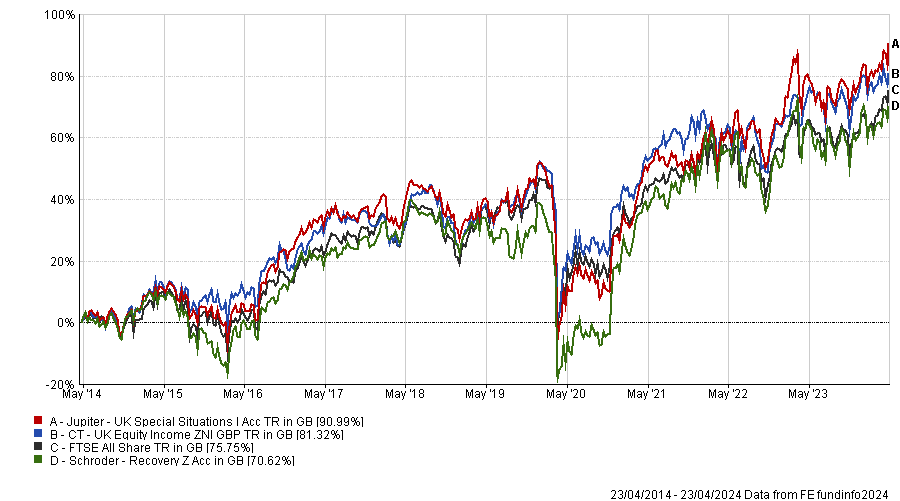

For investors who want to bet on the UK equity market’s sustained recovery and take advantage of the current reasonable valuations, McDermott suggested CT UK Equity Income, Jupiter UK Special Situations and Schroder Recovery. “These funds offer well-diversified portfolios, primarily focused on larger UK companies,” he said.

Performance of funds vs benchmark over 10yrs

Source: FE Analytics

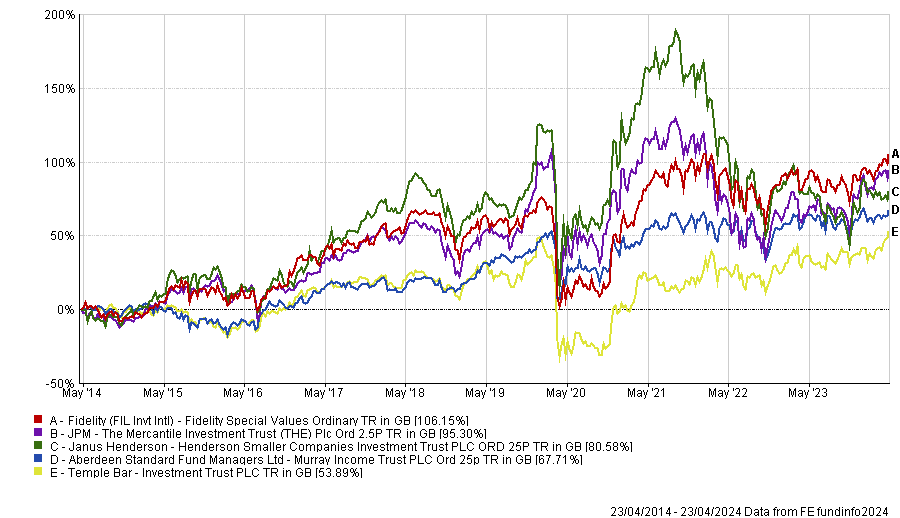

Hollands recommended considering investment trusts trading at discounts. “Strong trusts to consider include Fidelity Special Values (-10.1% discount), Mercantile Investment Trust (-11.2% discount), Murray Income Trust (-9.9% discount), Temple Bar Investment Trust (-7.4%) and Henderson Smaller Companies (-14.3%).”

Performance of trusts over 10 years

Source: FE Analytics

Most of the UK Equity Income funds with more than £1bn under management own BP, Shell and GSK.

Several of the largest and most popular UK equity income funds hold the same stocks so investors who split their income portfolios between these funds might not be getting the diversification they are trying to achieve – depending on which funds they choose.

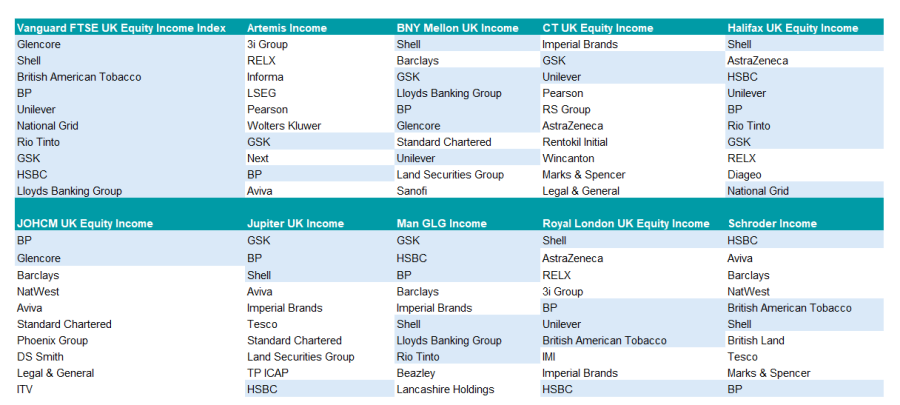

The IA UK Equity Income sector houses 10 funds with more than £1bn under management. One of these – the £1.2bn Vanguard FTSE UK Equity Income Index fund – is a passive tracker so Trustnet compared its top 10 holdings with those of the other nine funds.

Halifax UK Equity Income has the greatest overlap, with seven of the Vanguard tracker’s largest holdings amongst its own top 10, closely followed by BNY Mellon UK Income and Man GLG Income with six apiece.

Royal London UK Equity Income shares half of its top 10 stocks with the FTSE UK Equity Income Index. Four of Jupiter UK Income and Schroder Income's holdings overlapped.

At the other end of the spectrum, three funds share just two stocks with the Vanguard FTSE UK Equity Income Index’s top 10: Artemis Income, CT UK Equity Income and JOHCM UK Equity Income.

The most popular stock is BP; only CT UK Equity Income doesn’t have the oil giant in its top 10.

Shell and GSK are owned by seven of the 10 funds (including Vanguard), six hold HSBC and five have Unilever.

Beyond the index, several of these large funds’ highest conviction positions overlap with each other. Aviva, Barclays and Imperial Brands are owned by four of the funds, while AstraZeneca and Standard Chartered feature in three funds apiece.

Funds’ top 10 holdings

Sources: FE Analytics, funds’ factsheets

Market concentration forces large funds into the same stocks

One of the reasons that UK equity income funds’ holdings overlap is that the FTSE 100 is a highly concentrated market. Its top 10 holdings comprise almost half of its market capitalisation, while 57% of all dividends are paid by just 10 companies, according to Octopus Investments’ ‘Dividend Barometer’.

Sector concentration is significant too and can cause issues in times of market stress, such as the Covid-19 pandemic when oil companies slashed their dividends and banks were compelled to stop paying dividends completely.

AJ Bell investment director Russ Mould highlighted the UK market’s “hefty portion of earnings from unpredictable sectors such as miners and oil, and economically sensitive ones such as banks and consumer discretionary.”

Market concentration is even more of an issue for funds that have amassed a lot of assets – such as those in this study – which are compelled by their sheer size to channel assets towards the UK’s biggest companies.

Analysts at interactive investor, who added the £4.6bn Artemis Income fund to their Super 60 buy list this year, observed: “With its considerable size, the fund does not have the flexibility to invest significantly down the market-cap scale, but that has not hindered performance relative to the index over the medium term.”

The fund with the most differentiated holdings

Artemis Income had the most original line up from amongst the largest funds in the IA UK Equity Income sector. Four of its top 10 stocks were absent from its peers and from the FTSE UK Equity Income Index’s largest 10 positions.

FE fundinfo Alpha Manager Adrian Frost, Andy Marsh and Nick Shenton have struck out on their own by investing in Informa, LSEG, Wolters Kluwer and Next.

Managers who took bold off-benchmark bets

However, it was not the most actively-managed fund over the long term, according to the data.

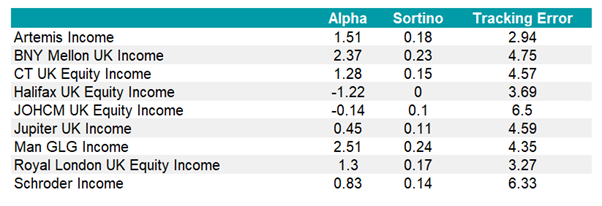

Indeed, JOHCM UK Equity Income, led by Clive Beagles and James Lowen, came out on top with the highest tracking error over 10 years and 15 years, meaning that the managers deviated from their benchmark and took active bets.

It was followed by Schroder Income under Andrew Evans and Kevin Murphy. Both houses have a value investment style.

Funds’ tracking error, alpha and Sortino ratios over 10yrs

Source: FE Analytics, data to 22 April 2024

The least correlated fund to the benchmark

The 10 largest funds in the IA UK Equity Income sector are closely correlated, which is to be expected as they have similar mandates; although CT UK Equity Income stands apart in this regard.

The only fund not holding BP in its top 10, CT UK Equity Income was significantly less correlated than its peers to the Vanguard FTSE UK Equity Income Index fund during the past three years to 19 April 2024. Its correlation was 0.76 according to FE Analytics, whereas the next lowest was Royal London UK Equity Income at 0.87.

Managed by Jeremy Smith, co-head of UK equities at Columbia Threadneedle Investments (and by veteran manager Richard Colwell until his retirement in 2022), the £3.2bn fund pursues a contrarian, value-oriented strategy and focuses on both mid- and large-caps. Smith aims for above-market yields with dividend and capital growth.

Kamal Warraich, head of equity fund research at Canaccord Genuity Wealth Management, pointed out that “the contrarian approach has often led to significant sector biases” such as a zero weight to energy and banks, but a large overweight to industrials.

The best performers

Despite the overlapping stock picks between some of the most popular funds, the outcomes experienced by investors diverged significantly over the long term.

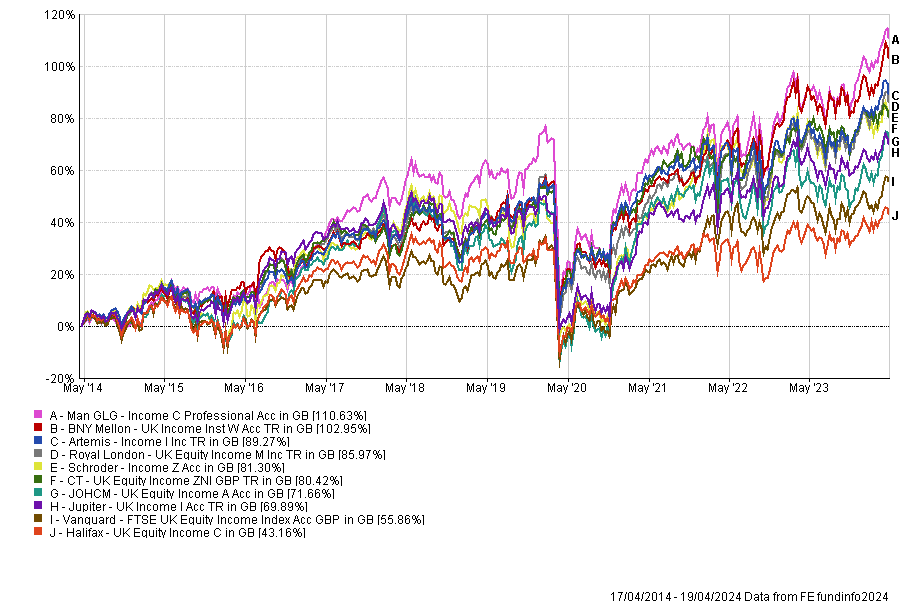

The best performers were Man GLG Income and BNY Mellon UK Income, both of which have doubled their investors’ money over 10 years to 19 April 2024, up 110.6% and 103%, respectively.

Vanguard’s tracker delivered half of that and was the second-worst performer of the group, up 55.9%, while Halifax UK Equity Income brought up the rear with 43.2%.

Performance of funds over 10yrs

Source: FE Analytics

Paul Angell, head of investment research at AJ Bell, recommended Man GLG Income for ISA investors. “The manager has a preference for stocks which have strong potential for dividend growth (exceeding twice the market average) and bonds (max 20%) that on a relative basis appear more attractive than their company’s equity,” he explained. “In order to avoid value traps the manager additionally focuses on a firm’s cash, cash flow, and assets.” The £1.7bn fund has a yield of 5%.

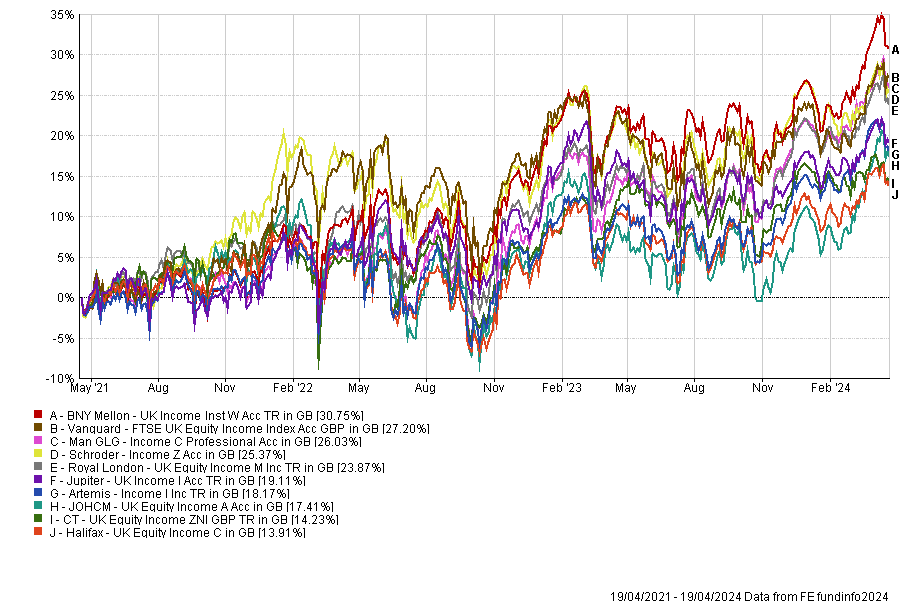

More recently however, Vanguard FTSE UK Equity Income Index has had its moment in the sun. The low-cost passive fund delivered the second-best returns of the group over three years, up 27.2%.

Performance of funds over 3yrs

Source: FE Analytics

BNY Mellon UK Income pulled ahead with 30.8% and had the highest alpha by a long way (5.1). Man GLG Income and Schroder Income returned 26% and 25.4%, respectively, with alpha scores of 3.33 and 3.35 over three years.

Financial advisers reveal their top choices for savers building up their pension pots and for retirees already withdrawing from their SIPPs.

Ruffer, Worldwide Healthcare and JP Morgan Global Income & Growth are among the best options for investors putting their pensions into investment trusts, according to IFAs.

There are typically two stages to pensions: the accumulation (or wealth building) phase where those yet to reach retirement are trying to increase their pot as much as possible; and the withdrawal phase for people who have finished work and are relying on their savings for income.

This tax year, savers can put up to £60,000 into a self-invested personal pension (SIPP), an increase on the £40,000 available 12 months ago, and can carry forward any unused allowances over the past three years.

As such, now may be a good time to consider what to buy. Below, financial advisers give their favourite investment trusts for each of the two stages of pensions.

The accumulation/wealth building phase

People with a long time horizon until retirement can consider taking more risk and investing in trusts that should grow over the long term, even if they experience short-term wobbles.

As such, Philippa Maffioli, senior investment manager of Blyth-Richmond Investment Managers, said growth and diversification during this period are crucial.

She suggested Worldwide Healthcare Trust, which gives investors exposure to pharmaceutical, biotechnology and other related healthcare companies ranging from multinational brands to unquoted companies.

Performance of trust vs sector and benchmark over 10yrs

Source: FE Analytics

“The fund is managed by OrbiMed Capital which was founded in 1989 and has become the largest healthcare investment firm in the world. The team is actively looking at nearly 1,000 companies and works to identify sources of outperformance, as well as those with underappreciated products in the pipeline with high quality management teams and strong financial resources,” she said.

Another option with a broader remit is Monks Investment Trust, managed by Spencer Adair and Malcolm MacColl from Baillie Gifford.

Performance of trust vs sector and benchmark over 10yrs

Source: FE Analytics

“Their aim is to focus on global companies from a range of profiles with above average earnings growth, which they expect to hold for around five years,” Maffioli said, although noting that they “address issues head on and aren’t afraid to take a critical look at their portfolio when necessary”.

For those unwilling to take such big bets on styles or themes, Chancery Lane chief executive Doug Brodie suggested trusts with long track records of outperformance such as Lowland, Murray International and City of London, which he said have “handsomely” beaten the FTSE All Share over 20 years. However, it is worth noting that Murray International is a global portfolio while the other two are UK focused.

Performance of trusts vs FTSE All Share index over 20yrs

Source: FE Analytics

“Investment trusts may not have the sales and marketing budgets of pension companies so investors have to look a bit harder. A quick look at the long-term returns will show folk there’s a good reason that institutional investors are big investors in trusts,” Brodie said.

For more tactical investors, Paul Chilver, associate and financial planning manager of Birkett Long IFA, suggested concentrating on trusts currently on a discount – of which there are many.

“Discounts are particularly attractive on UK-focused investment trusts and one suggestion for the accumulation stage of investment is the Mercantile Investment Trust managed by JPMorgan, which has been at a double-digit discount for many months despite very good short-term performance,” he said.

The decumulation/withdrawal phase

People already in retirement have to marry two competing issues. The first is to make sure that their investments continue to grow so they do not run out of cash, while the other is to withdraw money to help them make up the shortfall from a lack of earnings.

To balance this, Neil Mumford, chartered financial planner of Milestone Wealth Management, suggested the Scottish American Investment Company, known as SAINTS for short.

Performance of trust vs sector and benchmark over 10yrs

Source: FE Analytics

“This is my choice for someone looking at building either an income or growth portfolio and is a top five holding in my own SIPP. I am still accumulating but it will stay once I am drawing down,” he said.

“It is a truly diversified equity portfolio, spread equally between the US and Europe at around 35% each of the portfolio. Although it doesn’t have the highest yield at 2.9%, this dividend hero has increased its payouts by an average of 4.2% a year over the past five years and this dividend increase has not hampered its ability to grow capital – a total return of more than 170% over the past 10 years should please any investor.”

Now could also be a good time to get in as the share price is a “complete bargain”, trading at a discount of 10% to the trust’s net asset value.

More defensive investors might prefer the Personal Assets Trust or Ruffer Investment Company, said Maffioli, which both focus on capital preservation.

The former, managed by Sebastian Lyon and Charlotte Yonge, “offers global diversification across four asset classes and is a bedrock for lower risk and/or decumulating portfolios,” she said.

Ruffer meanwhile uses a “very disciplined approach”, aiming to maintain value over one year and grow capital incrementally over the longer term. “This means they would perceive a loss in line with the market as a failure,” Maffioli noted.

A trust for both?

One trust that appeared in the recommendations for both phases was JPMorgan Global Growth & Income Trust. Mumford said it was a strong option for those looking to build their wealth, as it invests predominantly in the high-growth US market, which makes up two-thirds of the portfolio.

“It is a high conviction portfolio with 50 to 90 holdings, with the top 10 making up more than 40% of the portfolio. This has allowed it to outperform by some margin with a 305% return over the past 10 years,” he said.

Performance of trust vs sector and benchmark over 10yrs

Source: FE Analytics

It is one of the few trusts trading on a premium at present, but this should not concern long-term investors, Mumford noted, adding it is “ideal” for regular monthly investments.

Chilver meanwhile highlighted the trust for those in the decumulation stage of their pension, noting that its 3.4% yield makes it attractive, despite its high weighting to the typically lower yielding US market.

Passive exposure to EMs isn’t likely to give investors what they are actually looking for…