Talib Sheikh, who recently took over Fidelity’s multi-asset income funds, believes the global economy has entered a new regime.

Talib Sheikh has spent 2024 moving Fidelity International’s $7.4bn multi-asset income portfolios out of government bonds, going overweight Europe and enhancing the investment process, after replacing Eugene Philalithis at the start of this year.

One of the first moves Sheikh made was to reduce interest rate risk and duration from three and a half years to one year in the $5.5bn FF Global Multi-Asset Income fund and its stablemates. “All we have left is short-dated plays,” he said.

Government bonds are expensive and risk additive, he explained. As a result, diversification has become harder during the past 18 months because “government bonds and investment grade credit haven’t really been that safe”. Currencies can be a useful diversifier, he added.

In the fixed income portion of his portfolios, Sheikh favours corporate hybrids in Europe. He has invested in contingent convertibles (CoCos), also known as additional tier 1 (AT1s) bonds, which sit at the bottom of the debt stack above equities and pay attractive yields in the region of 7.5% for two years of duration.

He has modest exposure to infrastructure using investment trusts, which have had “a pretty torrid time” in recent years due to rate hikes. They offer high free cash flows and high dividend yields, many of which are inflation-linked, he said.

Equity exposure is at the top end of his funds’ permissible ranges, at 40% for FIF Multi Asset Income, 60% for FIF Multi Asset Balanced Income and 80% for FIF Multi Asset Income & Growth.

Sheikh, who joined Fidelity from Jupiter Asset Management in October, has been increasing his exposure to core developed market equities where growth is expanding, with an emphasis on continental Europe. “We’re trying to buy more value plays where there is a cushion, where we can see the earnings start to increase from here,” he explained.

Performance of fund year-to-date vs sector

Source: FE Analytics

Sheikh has adjusted the investment process to be more responsive to changing economic scenarios so that the fund is always “relevant”, whatever the macroeconomic outlook.

These changes resulted in Square Mile Investment Consulting & Research removing the Multi-Asset Income fund’s A rating as its analysts would “prefer to see how the combination of the changes to the team and approach progresses over time”. Rayner Spencer Mills Research reaffirmed its rating.

Sheikh said he approaches multi-asset investing in a similar way to his predecessor Philalithis. “The way I think about the world is very connected to the way Fidelity thinks about it,” he explained. “They definitely wanted someone who thought in a similar way to how Eugene built portfolios.”

Nonetheless, he also wants to bring his 25 years of experience to bear. “I’m not just going to copy what Eugene did. I want to try and enhance the process and bring my own experience. Most of that is to do with the idea that we’re in a new regime.”

Sheikh believes the global economy has entered a new regime of regional desynchronisation, higher government deficits and stickier inflation. He thinks inflation will move symmetrically around central banks’ targets, so “sometimes we’ll worry about inflation, sometimes we’ll be worrying about deflation”. The macroeconomic backdrop is oscillating between reflation, where commodities do well, and goldilocks, where equities outperform, he observed.

Between the financial crisis and the Covid pandemic, the global economy moved in sync but more recently, regional economic cycles have become desynchronised. Europe and the UK have experienced mild recessions, China has had “a terrible time” and US economic resilience has surprised on the upside.

This has created greater divergence and therefore more opportunities for asset allocators. “If you’ve been ignoring Europe, long the US, long Japan and short China, you’ve had an amazing three years,” he observed.

Sheikh’s approach to asset allocation is to form a structural view – his outlook for the next six to 12 months – then a shorter-term cyclical view covering six to nine months, which guides tactical shifts. He then analyses what his structural and cyclical forecasts mean for asset prices.

“I think of macro forces as being like a wave going across the global economy. It’ll hit one asset class then another asset class, then another asset class,” he explained. “So what we’re trying to do is think forward how those macro forces are going to be priced across various asset classes.”

The multi-asset portfolios are built using Fidelity funds alongside third-party funds, leveraging recommendations from the in-house manager research team. He also uses derivatives to adjust the asset allocation efficiently and cheaply.

Sheikh’s funds have three objectives: income first, as well as downside protection, plus the prospect of capital growth. He is aiming for volatility to be half that of the equity market and described the investment process as “stable, repeatable and sensible.” His multi-asset funds will not beat returns from equities over 10 years, but “we’re a different animal”, he pointed out. “We’re taking half the risk. There is no free lunch. We’re trying to smooth the ride for investors.”

European high yield has outperformed the US this year, which is pretty rare, but the factors driving those returns are even more intriguing.

With an impressive 12.29% return, high-yield bonds were the best-performing sub-sector of the fixed income universe in 2023. To investors’ delight, that relative momentum has been maintained into 2024 despite spreads being tight and there are signals of further good news ahead.

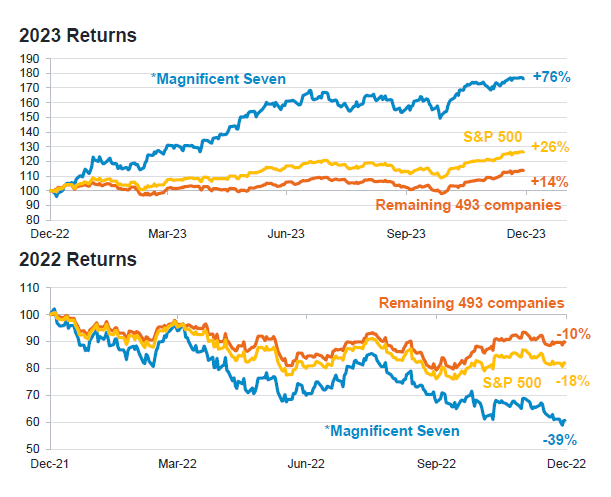

The high-yield market has behaved similarly to global equities (if you strip out the outlier performance of the ‘Magnificent Seven’) benefiting from the shift towards risk-on, fuelled by signs of falling inflation and the prospect of rate cuts – even if they are delayed and fewer in number than originally expected.

But the most fascinating element of high yield as we move into spring is the increase in differentiation between the US and Europe.

US high yield is essentially flat on the year. Within that, B and CCC-rated bonds rallied strongly over the first quarter of 2024 but have since sold off, along with the rest of US high yield as the effects of interest rate uncertainty have impacted US credit generally.

In contrast, dynamics in European high yield have become very interesting. Over 12 months, Europe has outperformed the US by 1.8%, which in itself is a pretty rare occurrence. But what’s even more unusual is that the European market has outperformed despite the fact that it has more BB bonds in its universe.

Indeed, BBs have led the European market year-to-date, up 1.86%. BB-rated bonds have generally outperformed their US counterparts and have not sold off to the same extent in the second quarter of this year.

The driver of this differential comes from the different expectations around interest rate paths for Europe versus the US. A first cut in the summer remains likely for Europe, while later this summer or even further out is looking more plausible for the US.

As an active manager, it’s good to see the return of differentiation between rating categories that are classically more interest-rate sensitive like BBs, and those more influenced by factors like idiosyncratic risk, which is the case for CCCs. This creates potential value-add opportunities across geographic allocations and credit selection.

On a global view, the high-yield market was yielding 8.11% at the end of April. While this is a touch off the 9-10% that we view as an automatic ‘buy’ signal, strong coupon generation is keeping performance motoring and is only likely to increase as rates remain higher for longer.

Despite the market largely pricing out early interest rate cuts, performance has been maintained by a healthy underlying economic environment for credit. Tailwinds include limited supply, thanks to lots of names refinancing early, as well as multiple ‘rising stars’ moving back up to investment grade. Additionally, you’ve got investors looking to deploy cash, both from coupon income and new allocations.

It would be remiss not to mention that we’ve seen a couple of headline-grabbing negative credit events recently, but these have resulted from idiosyncratic stories around very large-cap structures struggling against poor results and refinancing issues.

Overall, the first quarter results season left corporates on firm footing with the asset class supported by healthy tailwinds, which should set it up for continued positive performance. When we see firm signs of rate cuts coming through, that should provide an extra boost to risk appetite.

In our portfolios, we’ve been adding coupon risk as we see that as the best way of generating returns within high yield as we tread water ahead of rate cuts. The US offers greater coupon return potential and has the stronger underlying economy, but that must be weighted up against the return of differentiation in Europe, which we would expect to outperform given the more benign growth and inflation environment.

We think a quality stance in Europe with a little bit more interest rate sensitivity is probably a good thing versus the US, because you've got at least one rate cut coming from the European Central Bank in the next couple of months, as reflected in the outperformance of BBs. Investment flexibility around regional allocations allows us to make top-down decisions based on where we see macro drivers and pressures, while we’re giving significant weight to bottom-up research in the current environment to avoid idiosyncratic risks.

Andrew Lake is head of fixed income at Mirabaud Asset Management. The views expressed above should not be taken as investment advice.

The research company’s Academy of Funds has several new entrants and two departures.

Square Mile Investment Consulting and Research has released its latest Academy of Funds round-up today, announcing the departure of two funds and a number of new entrants.

It has expelled PIMCO GIS Dynamic Multi-Asset and abrdn Europe ex-UK Income Equity from its Academy of Funds due to changes in leadership. Managers Geraldine Sundstrom and Stuart Brown are about to leave PIMCO and abrdn, respectively.

“While Square Mile acknowledges PIMCO’s strong resources and team approach, the fund’s rating was largely predicated on Sundstrom’s experience of managing dynamic multi-asset strategies,” Square Mile’s analysts said.

“As for the abrdn fund, it has lost its two portfolio managers within a relatively short period, with the previous co-manager Tom Dorner departing in September 2023, and Square Mile would like time to monitor the strategy and its investment team after the announced new manager, Charles Luke, will have stepped in.”

These defections were compensated by several additions to the fray.

Premier Miton secured a quartet of new ratings for its Diversified Growth range, with the Diversified Cautious Growth, Diversified Balanced Growth, Diversified Growth and Diversified Dynamic Growth funds all gaining an A rating as they enter the Mile Academy of Funds.

The flagship fund in the range, Diversified Growth, has delivered strong risk-adjusted returns for more than a decade, while the other three funds have achieved this since their launch over five years ago.

Performance of fund against sector and index over 5yrs

Source: FE Analytics

“Key to the strategies' success are the views of the specialist investment teams at Premier Miton, which are responsible for the underlying sleeves which collectively make up the funds within the range,” the analysts said.

“These funds are a robust option for investors seeking a range of growth-orientated actively managed multi-asset portfolios.”

One of the cheapest active funds in the IA North American sector, the HSBC US Multi Factor Equity fund also received an A rating thanks to the managing team’s ability to “consistently provide alpha across a range of strategies since July 2006”.

The fund offers core exposure to US equities, targeting an ex-ante tracking error of 2.5% per annum from the S&P 500 and focusing on value, quality, momentum, low risk and size factors.

In the closed-ended space, the Mercantile Investment Trust also joined the list with an A rating. The strategy is led by the “experienced” Guy Anderson, who is part of a “well-resourced” team at JPMorgan Asset Management.

The trust predominantly focuses on high-quality and fast-growing UK equities listed outside of the FTSE 100. It convinced Square Mile for its “repeatable, efficacious” investment process, its liquidity as a £1.7bn investment vehicle, and its yield which has grown each year over the past 10 years and is currently at 3%.

Finally, the Vanguard Global Corporate Bond and Global Short Term Corporate Bond index funds were given Recommended ratings, which are awarded to funds that “meet the highest standards in their fields but cannot be readily differentiated from their direct peer group, such as passive vehicles”.

The former tracks the Bloomberg Barclays Global Aggregate Float Adjusted Corporate Index Hedged and the latter the Bloomberg Barclays Global Aggregate Corporate 1-5 Year Float Adjusted Index Hedged.

“Both funds’ benchmarks are structured in such a way that the largest constituents will be companies with the highest absolute levels of debt. While this could create a concern from a credit risk perspective, it is difficult to avoid given the size of the investment universe,” the analysts concluded.

Strategies admitted to the Academy of Funds

Source: FE Analytics

The investment platform is rolling out a range of passively-managed multi-asset solutions in response to the rising popularity of cheap trackers.

Hargreaves Lansdown is launching four multi-asset model portfolios using passive funds and exchange-traded funds (ETFs) managed by BlackRock.

The new passive range follows last year’s launch of HL Managed – a suite of model portfolios using active funds as building blocks.

The investment platform is offering a range of cheaper passively-managed solutions in response to the popularity of trackers amongst its clients, said chief investment officer Toby Vaughan. In the past two years alone, the number of Hargreaves Lansdown clients using passive funds as their main investment has increased by 80%.

“Our new ready-made multi-index investment portfolios are an easy cost-efficient solution for those looking to get started with investing,” he added.

The HL Multi-Index portfolios come in four flavours. The adventurous portfolio will have 100% in equities, while the moderately adventurous offering will have an 80/20 split between stocks and bonds, with 70-90% of equity market volatility.

Balanced investors will have 60% in equities and the rest in bonds, with 50-70% of stock market risk. Finally, HL Multi-Index Cautious will have just 30% in equities and 70% in bonds with 30-50% of the volatility of global equity markets.

Within that framework, Hargreaves Lansdown fund managers David White and Ziad Gergi will make country and sector allocation decisions, which they will implement using BlackRock’s passive funds and ETFs.

White is the lead manager for the new multi-index fund range as well as for HL Growth, the platform’s workplace default fund. He joined Hargreaves Lansdown in 2022 from Nationwide and before that ran institutional multi-manager portfolios at BMO Global Asset Management.

Gergi joined Hargreaves Lansdown last year from Barclays Wealth, where he was head of multi-asset portfolio managers. He is a co-manager of HL Multi-Manager Balanced Managed Trust, the HL Multi-Manager Equity & Bond Trust and the HL Multi-Manager Special Situations Trust.

The new multi-index model portfolios will start trading on 6 June 2024 and Hargreaves Lansdown is offering a £1 per unit fixed offer launch price until 11.59pm on 5 June 2024. The minimum investment is a £100 lump sum or £25 monthly commitment. The ongoing charges figure is capped at 0.3% but Hargreaves Lansdown charges its platform fees on top, which go up to 0.45%.

Promotion of Natalie Bell follows the hire of a new manager in the Liontrust Economic Advantage team.

Natalie Bell has been promoted to named manager on the £1.1bn Liontrust UK Smaller Companies and £146m Liontrust UK Micro Cap funds.

Bell has been part of Liontrust’s Economic Advantage team – which runs the funds – since August 2022 and has been supporting on the day-to-day management of the funds, building her knowledge of the holdings and contributing to investment decisions.

She joined Liontrust in 2021 as part of its Responsible Capitalism team, where she led engagement with investee companies across the full suite of the firm’s funds. Prior to joining Liontrust, Bell worked in corporate governance and policy at EY and the Confederation of British Industry (CBI).

Anthony Cross, head of the Liontrust Economic Advantage team, said: “Since moving across into fund management, Natalie has consistently impressed us with her diligence and skill in analysing companies.

“She has quickly become an integral member of the team and her recent tenacity in leading our efforts to lobby for government support for the UK equity market has been especially notable. Natalie’s promotion to become a named manager of the UK Smaller Companies and UK Micro Cap funds is richly deserved and a natural step in her continued career progression.”

Performance of funds vs sector over 5yrs

Source: FE Analytics

Bell will continue to work on the other Economic Advantage funds with their existing named managers. Her promotion comes after a new fund manager was hired by the team.

Alexander Game joined Liontrust last month from Unicorn Asset Management where he worked for almost a decade and was a named manager on the Unicorn UK Growth fund, Unicorn UK Smaller Companies fund and the Unicorn AIM IHT and ISA portfolio service.

Cross commented: “Alex is a natural fit for our team, bringing with him a strong track record of identifying attractive long-term investment opportunities and an investment ethos that is closely aligned to the Economic Advantage process.”

Liontrust said Bell’s promotion and Game’s appointment are “very positive milestones” in the evolution of the Economic Advantage team.

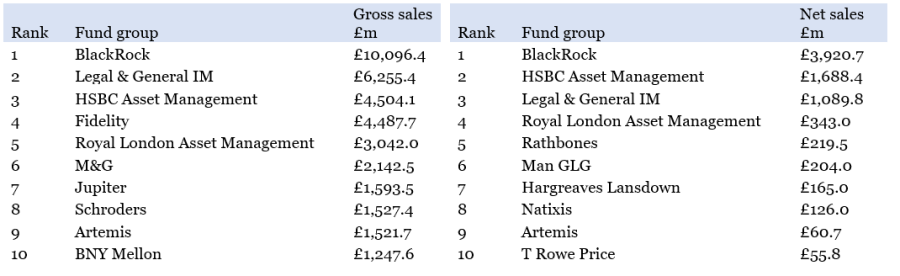

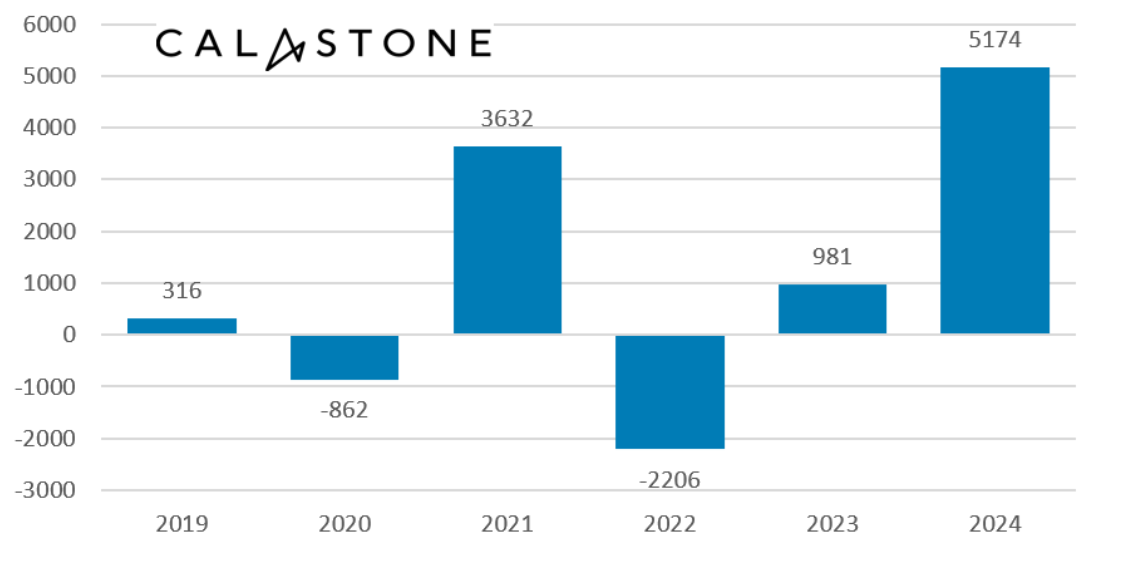

Quarter-over-quarter and year-over-year fund sales have grown in all major asset classes.

UK fund groups have opened 2024 with elevated inflows compared to 2023, the latest Pridham report released today has shown.

BlackRock, Legal & General Investment Management and HSBC Asset Management were the main beneficiaries thanks to their passive offerings, which accounted for 74% of all new flows.

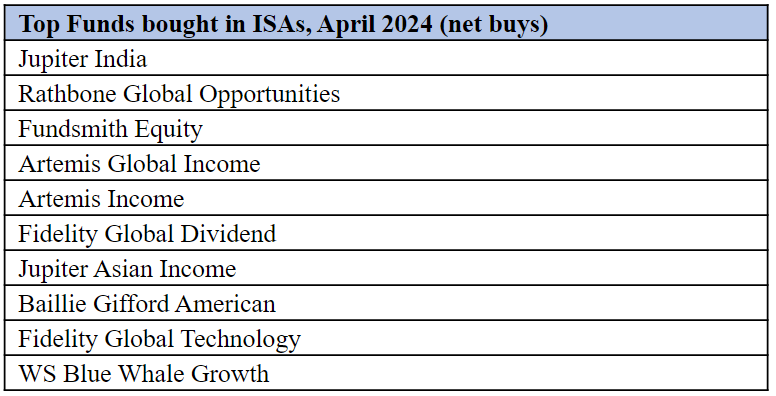

But active managers also benefitted from recent growth trends, with seven houses moving into positive sales territory – most notably Jupiter Asset Management, Artemis and Rathbones, as the tables below show.

Most popular asset managers in Q1 2024

Source: Pridham report

Compared to 2023, BlackRock’s leadership position was further strengthened this year, with gross retail flows into its UK domiciled open-ended investment funds surpassing £10bn for the first time since the final quarter of 2020.

HSBC also moved up one ranking on the back of its passive funds.

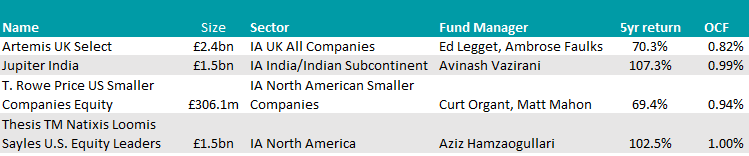

In the active cohort, Artemis entered the top-10 best-selling gross and net sales rankings with strong demand for its equity funds, especially Artemis UK Select, which was its top retail seller.

Jupiter moved up two spots for gross new business and has seen growth in three consecutive quarters. The Jupiter India fund received the most retail attention, placing it within the quarter’s best-selling retail funds.

The popularity of US equities among UK-based investors also gained Natixis Investment Managers and T. Rowe Price a spot in the top 10 best-selling net new business rankings – Natixis Loomis Sayles U.S. Equity Leaders and T. Rowe Price US Smaller Companies Equity were the most bought strategies.

Source: FE Analytics

With equity markets buoyant and fixed income offering investors both yield and capital appreciation potential, the future looks bright for the

“Q1 retail sales showed that demand for high-performing active funds remains there. The active opportunity, however, is diverse, with fund groups often only seeing success in a limited number of investment categories at one time,” he said.

“As retail investors and their advisers adjust their portfolio allocations to reflect the outlook of higher for longer interest rates, opportunities will be created for fund groups to win new business.”

Fund selectors lose confidence in the AllianzGI bond strategy after Mike Riddell’s departure.

Experts are selling the Allianz Strategic Bond fund after its lead manager Mike Riddell jumped ship to Fidelity International.

Allianz Global Investors (AllianzGI) has appointed Julian Le Beron to take over with an “enhanced” team-based, co-led approach, which “will be beneficial in terms of expanding the inputs into strategies,” the firm said.

This development didn’t convince experts, who all agreed the fund is a sell.

Having shot the lights out in 2020, as 8AM Global’s Andy Merricks noted, Allianz Strategic Bond is “at least consistent now, achieving fourth quartile returns regularly”.

Performance of fund against sector and index over 5yrs

Source: FE Analytics

“I would assume that those still holding it are doing so because of Mike Riddell in the hopes that he can recapture the spark of 2020. Now that he’s moved to Fidelity I would imagine Riddell supporters will follow him,” he said.

“For those who remain, it will be interesting to see whether the ‘enhanced’ investment process means that it will find a way of yielding even less than it does now compared to cash and eroding capital or whether they will stem the tide and see better performance in the coming months.”

Ben Yearsley, investment consultant at Fairview Investing, agreed with Merricks that the fund is “quite unique and very specific to Riddell”, making it “difficult to stay put after he's gone”.

Investors won’t be able to follow Riddell to Fidelity directly either, as he won't take over the Fidelity Strategic Bond fund until 2 January 2025 at the latest.

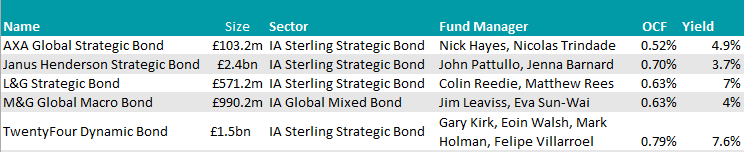

It’s also likely that the new AllianzGI managers will dial down the risk, according to Yearsley. He recommended that investors “sell now and go for a new choice”, possibly splitting the money between AXA Global Strategic Bond and the M&G Global Macro Bond fund.

“They blend well together as the AXA fund has core allocations to the main bond asset classes while the M&G’s product is more specialised, with currency returns being a big part of the decision making process,” he said.

It is managed by Jim Leaviss, who Yearsley considers “one of the premier bond managers”.

Jason Hollands, managing director of Bestinvest, also leaned towards selling, indicating the TwentyFour Dynamic Bond fund and the Janus Henderson Strategic Bond fund as two possible replacement candidates.

The former is a concentrated best-ideas fund with a flexible mandate to roam across the fixed income markets. It has performed “incredibly well” in a variety of very different market conditions.

“It is also able to use interest rate and credit derivatives to optimise exposure, as well as take short positions for hedging purposes,” he said.

On the other hand, the Janus Henderson vehicle invests across global bond markets focusing on total return rather than income.

“Managers John Pattulo and Jenna Barnard take a cautious approach to risk, not for example buy any emerging market bonds, only developed markets. They also have an aggressive selling mindset to protect the fund’s value, with company profit warnings or management change potentially triggering a review,” Hollands added.

Finally, Andy O’Shea, an investment director at Pharon Independent Financial Advisers, said he was never a fan of the AllianzGI fund as it did not provide enough risk diversification from equity exposure.

“There have been a number of funds that aim to provide a catch-all diversifier for clients through access to multiple sources of alpha, but using them all at once just introduces additional volatility with little quantifiable benefit. Therefore whilst Mike Riddell is undoubtably a very intelligent manager, I would not follow him across to Fidelity, nor stick with Allianz Strategic Bond,” he explained.

“I would suggest considering the L&G Strategic Bond fund instead. This fund slips under many radars but has provided IA Sterling Strategic Bond sector-beating performance and comprehensively outperformed the Allianz fund since the arrival of Colin Reedie in January 2019.”

Source: FE Analytics

Investors are unwilling to back smaller companies and other less liquid parts of the market, says the Henderson Opportunities Trust manager.

The collapse of Woodford Investment Management and the shuttering of his funds is still causing issues for other fund managers almost five years later, according to James Henderson.

The biggest consequence of the Woodford scandal, in which the disgraced fund manager invested heavily in unquoted or illiquid stocks – ultimately leading to the firm being unable to pay back investors who were trying to withdraw their money – is that investors now place a premium on liquidity.

This will cost them, however, when illiquid areas of the market such as smaller companies start to recover.

That’s what Henderson and co-manager Laura Foll are preparing for in their Henderson Opportunity Trust. It was hit harshly by investors’ attitudes turning sour towards the alternative investment market (AIM) three years ago, as the chart below shows.

Performance has dwindled somewhat in the past decade as well, with the vehicle slightly underperforming the rest of the IT UK All Companies sector over the past 10 and five years.

But Henderson is excited about the opportunities in AIM, as he explained below. He also discussed how much the economic backdrop impacts a company’s success and why there’s no such thing as a forever-stock.

Performance of fund against sector and index over 3yrs

Source: FE Analytics

What is the fund’s process?

We invest in a diverse list of stocks that often aren't in the mainstream. We're looking for the forgotten, unloved stocks and this always brings in a medium- and small-company bias to the fund.

We use different valuation methods for different areas of the market. We have a recovery theme going on at the moment and for a recovery stock, we're looking for turnover and not wanting to pay much for it.

Another area is tomorrow's winners. These are the often small companies that we believe will be more substantial in the future, so we're looking at prospective turnover and how they're compounding their earnings.

Why should investors pick your fund?

It's meant to be a real mixer in people's portfolios. We don’t see it as a one-stop shop, but as complementary to other things investors hold, as there won't be much crossover with more index-orientated funds.

Admittedly, it's a difficult fund to choose. The alternative investment market (AIM) hit a brick wall three years ago, which hasn’t helped. There aren't many funds looking in that area anymore and since Woodford’s funds imploded, there has been a real pressure on liquidity.

People may be paying too big a premium for liquidity. In the investment trust structure, we can take a slightly longer view and buy some illiquid stocks, because that's where the valuation discrepancy is greatest. That's where the excitement is and the recovery will come through.

How much is the performance of recovery stocks linked to the economic recovery of the UK?

Companies can achieve great things even with headwinds. Last year, Marks and Spencer recovered despite the cost-of-living crisis. The recession was very mild, but it still would have been a headwind and being one of the biggest names on the high street, it could go against the general economic climate.

If you provide excellent services or products, the overall economy doesn't really matter, and that'd be very much the case with some of tomorrow's winners as well, for example alternative energy stocks.

Whatever happens in the economy, if you're beginning to answer the energy problem so that people can move away from fossil fuels, it doesn't really matter what happens to the overall economy or interest rates: you're going to have a good business.

However, a bank is more closely tied to the economy, obviously.

Does this mean there are inherently good companies that you could potentially hold forever?

The lifecycle of companies is getting shorter and people don’t stay at the top of the tree forever. I would be careful about paying high P/Es [price-to-earnings ratio] for companies that are performing well. It's a very competitive world and there will always be people taking on the person at the top.

With the internet and things like price comparison websites, a company that starts to fail, doesn't have the best product, or is not giving the best service, is found out quicker than it used to. That's why we rotate out of the successes over time and into things that are more challenged, companies that are losing today that can recover.

How does this impact portfolios and turnover?

You need to be moving on a bit quicker than in the past. I can't envisage buying a share and thinking I'll never sell it. Turnover used to be about 15% and now it'd be closer to 25%. Average holding periods are also shorter, every five or six years we're turning things over. There are fewer forever stocks now.

Is Warren Buffett wrong then with his hold-forever philosophy?

In the English market, there aren't stocks like Coca-Cola. Every company that's been at the top in the UK has also declined over time. Vodafone was once a huge percentage of the UK index – while it’s still a very popular product, it's been dreadful for a long time.

However, even Coca-Cola wouldn’t be a forever stock. The world moves on even for it.

What were the best and worst calls of the past 12 months?

Our timing with Rolls Royce, which became the biggest holding in the fund, was lucky. It recovered much quicker than I thought it would. It was bought between £1.10 and £1.20 and the price now would be over £4.10. I've reduced it this week.

Our biggest drawdown last year was Zoo Digital, which does the dubbing for film productions. With the writer strike, it was hit big and then since it's opened up again, it hasn’t got back the amount of work it had before, as production companies do more in-house dubbing.

It has a good management team, but the area is much more difficult. The share price has been falling and we have cut it. The share price has fallen from £1.50 to £0.50.

What do you do when you’re not managing funds?

I’m very excited about getting into Bologna later in the month, as we've lent a picture to a show just outside Bologna on the pre-Raphaelites and Botticelli. They're showing how the Italian masters influenced English Victorian painters.

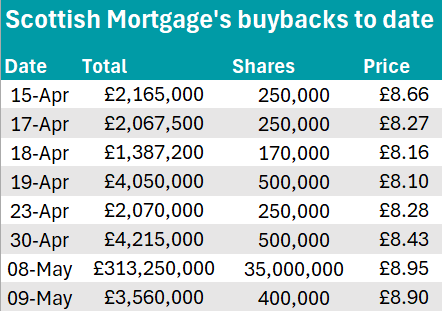

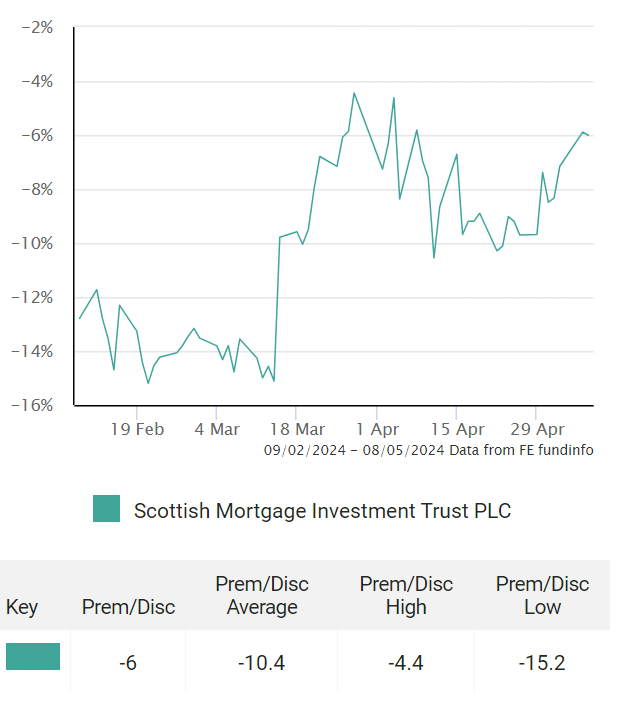

More than 94% of the trust’s share buybacks so far were carried out on Wednesday.

The Scottish Mortgage investment trust went on a shopping spree this week, buying £311m worth of its own shares in just one day – the largest buyback since its two-year budget of at least £1bn was announced in March.

Paying £8.95 per share, the company bought back 35 million shares on Wednesday, following up with a more modest £3.5m purchase on Thursday. Prior to this, the average purchase had only been worth approximately £2.8m per transaction.

The scale of this move means that 94.1% of the trust’s buybacks so far were carried out on this day, taking Scottish Mortgage approximately one-third of the way in its announced buyback programme.

Source: Trustnet, HMRC

The goal of this scheme is to narrow the trust’s discount, which was north of 14% in mid-March. Although the efficacy of buybacks has been brought into question by some, results seems to have arrived for the Baillie Gifford flagship trust, which is now trading at a 6% discount.

Scottish Mortgage’s discount

Source: Trustnet

Scottish Mortgage commercial director Stewart Heggie said the board and managers of the trust remain “resolutely committed” to facilitating trading around net asset value (NAV) and maximising returns for shareholders.

“Since the announcement of the buyback programme, the discount has narrowed by around 10 percentage points, which has contributed towards a share price return of 45% over the past year,” he concluded.

Multi asset funds have the potential to weather storms while making strong returns.

Picking when to get into stocks, bonds or alternatives is no easy feat. Market timing is notoriously difficult at the best of times but many think of it in the context of equities: when should I buy UK stocks or sell my US companies?

Now imagine trying to get the mix of assets right as well and it is easy to see how DIY investors can go disastrously wrong.

Sometimes investors can be overwhelmed by the choices on offer. Yet in investing, like many aspects of life, perhaps the simplest answer is also the most practical solution.

Multi-asset funds were designed to be a one-stop shop for savers who want to put their money to work but had no clue as to how to navigate financial markets. These funds typically invest in three core areas – equities, bonds and alternatives.

Research this week from Aegon Asset Management highlighted the fickle nature of markets, showing how varying asset class returns can be in each calendar year over the past decade.

It is a chart I have written about before, but thought worth mentioning again this time around for the inclusion of a multi-asset fund.

The fund selected in the below chart sits in the IA Mixed Investment 20-60% Shares sector, the second lowest risk multi-asset sector based on the potential amount the funds can hold in equities.

In theory therefore, investors would expect the returns to be far behind equities – given that this is the area that should make the most money over the long term. And this is true. Annualised returns over the 10-year period are far behind global equities.

But that is not the full story. Looking back over the past 10 calendar years, it shows that, more often than not, multi-asset funds can be in the top half of the performance ranking, beating global equities several times over the decade.

It also highlights that the annualised return matches the returns of UK stocks, while its risk-adjusted returns (the amount of potential loss versus potential gain) is pound for pound the same as global stocks.

In other words, although the returns have been lower, the volatility has also been dampened, meaning investors had a much smoother ride.

Source: Aegon Asset Management

The fund in question is the Aegon Diversified Monthly Income fund, which has been the seventh best performer over the past decade in its 104-fund strong sector.

Some may argue therefore that these figures do not represent the average fund and would require investors to pick one of the top performers – something which is incredibly hard to do without the benefit of hindsight.

Yet its five-year numbers are much closer to average. Even only looking over the past five calendar years, the portfolio has been above average in all apart from 2020, when Covid caused myriad issues for fund managers.

At my age (31 at the time of writing), I am in the somewhat advantageous position of only needing to put my money into equities. Most of my savings are for the long term, either retirement or as part of a rainy day fund that hopefully will remain untouched for several years.

But as I get nearer retirement (or needing the money for other reasons) and diversification and asset class selection becomes a much larger consideration – as will protecting my hard-earned savings – I will seriously consider moving my money to a multi-asset fund.

UK GDP grew by 0.6% in the first quarter of 2024.

UK GDP rose by 0.6% in the first quarter of the year, exceeding the Bank of England’s 0.4% expectations and indicating the end of the short-lived technical recession that gripped the country at the close of 2023.

This figure marks the UK's strongest quarterly GDP growth since before the pandemic and is also the first time in nearly three years that UK GDP has outpaced both the US and the Eurozone.

The service and production sectors rose 0.7% and 0.8% respectively in the first quarter of the year, spearheading the economic growth and offsetting the decline in construction.

As such, today’s GDP figures coupled with yesterday’s inflation numbers suggest the UK economy is turning a corner.

However, David McCreadie, CEO of Secure Trust Bank, stressed that growth forecasts anticipate the economy to plateau.

He added: “Attention now shifts to the Bank of England, given the sustained pressure on households and businesses stemming from elevated interest rates. A rate cut would provide an added impetus to the economy by reducing borrowing costs for businesses.”

However, Charles Hepworth, investment director at GAM Investments countered that the Bank of England may be less inclined to cut rates into an economy that is growing faster than expected. He explained that both inflation and wage growth dynamics will need to abate to make a June rate cut a “distinct likelihood”.

Danni Hewson, head of financial analysis at AJ Bell, added that although the figures are encouraging, the cut to National Insurance and the increase in the national minimum wage which took place in April have yet to come through to consumer spending and their impact remains to be seen.

She warned: “Those green shoots we’ve heard so much about since the start of the year have sprouted nicely, but it will only take one spring storm to damage the burgeoning flowers.”

Meanwhile, the FTSE 100 hit new all-time highs this morning, although it might not have much to do with domestic macro-economic factors.

Russ Mould, investment director at AJ Bell, concluded: “Given its international horizons, this has little to do with the UK’s better-than-expected GDP growth and is largely being driven by strength in the resources space where higher metals prices and the promise of M&A are helping to stoke share prices.

“The next key test of the index’s new-found vim and vigour will likely come next week in the form of US inflation figures.”

Dan Nickols, who leads Jupiter’s UK ‘smid’-cap team, will leave the firm on 30 June 2024.

Dan Nickols, head of Jupiter Asset Management’s small and mid-cap UK equities team, will retire on 30 June 2024. He is lead manager of the £426m Jupiter UK Smaller Companies fund and the £120m Rights and Issues Investment Trust and is an FE fundinfo Alpha Manager.

Matt Cable will replace him at the helm of both strategies. He has co-managed the Rights and Issues trust with Nickols since Jupiter won the mandate in October 2022. Cable joined Jupiter in 2019 and has more than 15 years of investment experience, garnered at M&G Investments and Schroders.

Tim Service, who has worked with Nickols for almost 20 years, will replace him as head of Jupiter’s ‘smid’-cap team and will be a supporting manager on the fund and trust. Service has been at Jupiter since 2007 and was previously a UK equity fund manager at Merian Global Investors. Earlier in his career, he was an analyst at JPMorgan and ABN Amro.

Nickols joined Jupiter in 2020 when it acquired Merian, where he led the UK small and mid-cap team. Before that, he worked at Albert E Sharp, Morgan Stanley and Deloitte and Touche.

Jupiter UK Smaller Companies has a strong long-term track record but has struggled during the past five years, trailing the IA UK Smaller Companies sector and the Numis Smaller Companies index. It peaked at £1.5bn in assets under management in September 2021 when it was the most popular fund in its sector but has been in outflow mode since then, shrinking to one third of its former size.

Fund vs sector and benchmark over 5yrs

Source: FE Analytics

The fund suffered in 2022 as central banks rapidly hiked rates, putting the small and mid-sized growth-oriented companies in its portfolio under pressure.

As Bestinvest managing director Jason Hollands explained: “This was down to the strong growth style bias being hit hard during a period of rising interest rates and borrowing costs. It is also a relatively concentrated portfolio for a small-cap fund, with circa 56 holdings, which does leave it more vulnerable to stock-specific risk than more diversified products.”

Trustnet looks at funds within the IA Europe Excluding UK and IA Europe Including UK sectors that have been run by the same manager since at least 2004 and have achieved top-quartile returns over the past three years.

European equities may not be as popular as their North American peers, but they are proving to be a more fertile ground for seasoned managers. While no veteran manager in the IA North America sector has been able to make top-quartile performance in recent years, four have achieved this feat across the IA Europe Excluding UK and IA Europe Including UK sectors.

Below, Trustnet researched the European funds that have been managed by the same person since 2004 or earlier and have produced top-quartile returns over the past three years, showing those who have been through it all and continue to make top returns.

One of the two funds in the IA Europe Excluding UK sector reflecting our criteria is Artemis SmartGARP European Equity, which has been managed by Philip Wolstencroft and Peter Saacke since 2001 and 2002 respectively. The latter is leaving the firm at the end of June however to become a maths teacher.

The fund’s investment process is based on Artemis’s proprietary tool “SmartGARP”, which aims to help the managers spot reasonably valued companies with superior fundamental growth.

As such, companies matching the market capitalisation and liquidity requirements are assessed against eight factors, including macroeconomics, investor sentiment, growth, valuation, estimate revisions, momentum, accruals and environmental, social and governance (ESG) factors.

Each company is then assigned an overall score, with 100 being the highest possible mark. However, only those scoring above 90 will be considered for inclusion in the fund.

The result is that none of the benchmark's heavyweights are among the fund’s top 10 holdings. Moreover, GSK is the only 'Granolas' stock in the fund, also constituting an off-benchmark position as it is listed in the UK.

While the fund has shined in recent years, long-term performance has been strong as well, with the fund also sitting in the sector’s first quartile over five years and in the second quartile over the past decade. Yet, this has come at the price of a higher volatility than its peers.

Performance of funds over 3yrs (to last month end) vs sector and benchmark

Source: FE Analytics

The second fund in the IA Europe Excluding UK matching our requirements is Waverton European Capital Growth, which has been steered by FE fundinfo Alpha Managers Charles Glasse and Chris Garsten since 2001.

They look for ‘wealth-creating’ companies, operating in favourable business environments and trading at attractive valuations.

The fund is concentrated, with the top 30 holdings accounting for 98% of the portfolio according to FE Analytics. The managers do not bet the house either on the Granolas as it just holds three of them (out of 11): Nestle, Novartis and Sanofi.

Long-term performance has been good as well, as Waverton European Capital Growth sits in the top quartile of the sector over five and 10 years.

It has also been one of the least volatile funds in the IA Europe Excluding UK sector both in recent years and over the past decade.

Two veteran managers in the IA Europe Including UK sector also outpaced their competitors over the past three years.

The first one is Laurent Nguyen, who has been at the helm of Pictet Quest Europe Sustainable Equities since 2002 and also delivered top-quartile performance over 10 and five years.

ESG factors are a core element of the strategy, with the manager seeking to invest in companies with low sustainability risks and to avoid those involved in activities that negatively impact society or the environment.

Unlike the two previous funds, Pictet Quest Europe Sustainable Equities takes a bigger punt on the Granolas, with Novartis, Novo Nordisk, L’Oreal and GSK all appearing in the top 10 holdings.

Both short- and long-term performance have not come at the expense of higher risk, as the fund has consistently been one of the least volatile in the sector. It also boasts one of the highest Sharpe ratio, indicating investors have been fairly rewarded for the amount of risk taken.

Performance of funds over 3yrs (to last month end) vs sector and benchmark

Source: FE Analytics

Finally, Michael Barakos is another European veteran manager to have delivered top quartile returns over the past three years.

He has been managing JPM Europe Strategic Value since 2004 and was joined by Ian Butler in 2014 and Thomas Buckingham in 2017. Together, they look for attractively valued sound companies.

As such, the fund is currently overweight insurance, bank and automobiles & component sectors, with Mercedes-Benz being the latest addition to the portfolio. The decision was made as a result of the German car company’s announcement of a new share buyback.

Conversely, JPM Europe Strategic Value recently sold UK bank NatWest due to disappointing third-quarter results and financial year 2023 guidance last year.

While short-term performance has been good, the fund has suffered over the past decade, as the value-style of investment has been generally out of favour in that period. As such, it sits in the bottom quartile over 10 years and in the third over five years.

The fund has also been more volatile than its sector peers, both over the short- and long-term.

Toys, social media, gaming and music are all ways children can invest in the things that interest them.

UK savers have an infatuation with cash, particularly parents, the majority of whom are placing their children's Junior ISAs (JISAs) into cash rather than investing in stocks and shares.

In fact, more than 60% of JISAs are held in cash. This flies in the face of conventional wisdom, which suggests that people with long time horizons should put their money to work in riskier assets as they have more time to make money.

But there is a certainty with cash returns, while stocks can lose money. One way to help get over this hurdle is to encourage children to be interested in investing, according to Dan Coatsworth, investment analyst at AJ Bell.

This is crucial, as the more money built up for a child in their early years, the easier it should be financially for them to deal with some of life’s big milestones when they become an adult, he said.

He suggested a “spend some, save some” approach, as a “fair way to let the child deploy some of the cash while also subtly teaching them the importance of putting money away for another day”.

As they get older, Coatsworth said introducing concepts such as interest on savings and teaching them patience for bigger rewards will stand them in good stead for later money issues.

Children are likely to be more engaged if parents get them involved with investment decisions. Picking companies that make the things they like can be a great way to encourage the younger generation to put their money into assets that can make higher returns.

“A child might be more willing to put some of their money into certain companies, or funds that invest in them, if they are familiar with their products and services, and you explain that they could potentially make money if these companies do well,” he said.

“For someone of primary school age, it might be the companies which make their toys, favourite meals or drinks, or the creators of their cherished games.”

For example, Lego is an “obvious choice” when considering toy manufacturers. Unfortunately, the company is privately owned and you cannot buy its shares.

“Instead, choices of listed companies relevant to this theme include toy workshop operator Build a Bear; Hasbro, which owns Nerf and Peppa Pig; and Barbie and Hot Wheels owner Mattel,” Coatsworth said.

As they get older, interests may have moved on to things such as mobile phones, social media, fashion, music or gaming.

“Apple is likely to be a phone brand many children aspire to own, with the iPhone often considered to be a must-have product. Apple’s shares trade on the US stock market and can easily be bought by a UK investor and held in a Junior ISA,” said Coatsworth.

For music lovers, streaming service Spotify’s shares trade on the US stock market and can be included in a Junior ISA. It is one of the biggest music streaming platforms and makes money by charging users a subscription fee or carrying third party advertising.

Meanwhile, film buffs might wish to consider the parent companies behind such platforms as Amazon Prime, Apple TV, Disney, Netflix and Paramount Plus, which are all on the US stock market.

For social media users, US-listed Meta owns WhatsApp, Instagram and Facebook – the first two names are likely to have “considerable appeal” to teenagers, said Coatsworth.

“Snap is the other ‘biggy’ in the social media world with oodles of children using its Snapchat app. Its shares also trade on the US stock market,” he noted.

Meanwhile, although TikTok is owned by Chinese group ByteDance meaning its shares are not available directly, there are investment trusts and funds that have a stake in the company, including UK-listed Scottish Mortgage.

For gamers, he suggested VanEck Vectors Video Gaming and eSports ETF, where big holdings include Switch console maker Nintendo, Roblox and Take-Two, whose franchises include Grand Theft Auto.

Kazakhstan, the world’s ninth largest country, offers an array of eclectic and appealingly priced opportunities.

At first glance, frontier markets have delivered remarkably similar returns to the more established emerging markets over the past decade, but that simplistic view masks vast underlying differences between the two asset classes.

While a quick snapshot today shows comparable long-term numbers, the reality is that frontier performance is lowly correlated to emerging market equities, as well as far less volatile. The same is true between frontier and developed market performance.

In fact, to the surprise of many people, the MSCI Frontier index has been less volatile than even the MSCI Europe and Japan indices over the past decade. The low correlation and volatility are primarily due to decreased foreign investor activity within frontier markets.

With global growth expected to remain elusive in 2024, the world’s developing lower-income countries are expected to lead the way in growth terms over the coming year and beyond. This should not be surprising, considering that 16 out of the world’s 20 fastest-expanding economies over the past decade have been countries classified as frontier.

But despite continually improving fundamentals and the diversification qualities of the frontier universe, investors continue to underappreciate the eclectic and appealingly priced opportunities available in these often-misunderstood economies. In addition, the high degree of market inefficiencies arguably makes this equity investment class exceptionally suitable for active investing.

As such, we believe it is vital to regularly go on the road and visit the diverse countries within frontier to get a better understanding of the broader opportunities and risks within these untapped economies, as well as deepen our awareness of the unique corporates within.

If there was one part of the frontier universe far beyond the current gaze of investors, it would be the former Soviet republics in Eastern Europe and Central Asia. However, we continue to be encouraged by the investment opportunities within this vast part of the planet, which is why our team took a visit to the region last year.

Visible optimism abounds in Kazakhstan

While Kazakhstan is the world’s ninth-largest country by size, it has a small population of just 20 million people. Impressively, Kazakhstan's GDP per capita has risen tenfold to nearly $12,000 over the past two decades, primarily as a result of the development of the country’s commodity markets. However, the country also boasts a well-educated population – with a literacy rate of almost 100% – and relatively good infrastructure.

A turning point for the country came in 2019, when corruption-plagued leader Nursultan Nazarbayev – the first president of Kazakhstan – stepped down and was replaced by Kassym-Jomart Tokayev. While corruption remains a major issue, Tokayev has made strong strides in removing loyalists of the prior regime from top government and corporate posts.

On our trip, we visited Kazakhstan’s futuristic capital Astana, as well as the country’s commercial centre of Almaty, which sits at the foot of the majestic Trans-Ili Alatau mountains. While improvements remain in their infancy, it was encouraging to see how eager the government and corporates were in terms of elevating standards. On the ground, virtually everyone was excited about the prospects of this new era.

The top holding within our frontier markets portfolio is Kazakh financial group Kaspi, which is also the largest company in the MSCI Frontier Markets index. Kaspi’s super-app is the largest consumer-focused ecosystem in the country – with services in payments, marketplace and fintech. In fact, this is one of the most advanced digital eco-systems in the world where consumers easily can pay for items in-store, order groceries, renew their driver’s license or view their digital passports.

In January this year, Kaspi joined the Nasdaq after a $1bn share sale, which valued the entire company at more than $17bn, which has since then rise to nearly $22bn.

We met with the chief executive officer of Kaspi on our visit and continue to be impressed by his vision and the company’s growth plan execution, as well as capital allocation track record. We believe the valuation remains cheap and consensus estimates still underestimate Kaspi’s potential, particularly as it looks to grow beyond its current borders.

In addition to Kaspi, we have positions in several other Kazakh companies – including Kazatomprom, one of the world’s largest producers of natural uranium, Halyk Bank, the largest savings bank in the country, and London-listed Central Asia Metals, a mining company with operations in Kazakhstan and North Macedonia.

While we remain optimistic about the outlook for our Kazakh investments, it is important to remain vigilant to the risks, particularly as the country shares long borders with both Russia and China, who are competing for resource wealth and political influence. However, so far Kazakhstan has played its geopolitical cards in a well-balanced manner.

Unlocking value in off-benchmark Georgia

Our frontier team also visited the Georgian capital Tbilisi on our trip to the region. This small dynamic economy, which only boasts a population of about four million, has performed well over the longer term, driven by its oligopolistic banking sector.

The war in Ukraine has resulted in a huge influx of highly skilled Russian and Ukrainian IT developers into Georgia, which has propped up the economy and the currency. Surprising to many, the economy has risen by 25% in US dollar terms since the outbreak of the Ukraine war.

While not in the MSCI index, we characterise Georgia as a ‘regular frontier’, as its reasonably robust economic drivers are offset by political and geopolitical risks.

Our meetings with the country’s central bank and Ministry of Finance reinforced our view of the conservatively managed Georgian economy. It maintains a fiscal deficit below 3%, public debt/GDP is below the government cap of 40% and the current account deficit has shrunk to 3% of GDP.

We have exposure to the country through London-listed Georgia Capital – which has a diverse portfolio spanning pharmacy, insurance, renewable energy, water utilities and a large stake in Bank of Georgia. While the company trades on a NAV discount of more than 50%, we are optimistic about the strength of many underlying assets of Georgia Capital and expect the company to continue unlocking value over time.

Johannes Loefstrand is portfolio manager of the T. Rowe Price Frontier Markets Equity strategy. The views expressed above should not be taken as investment advice.

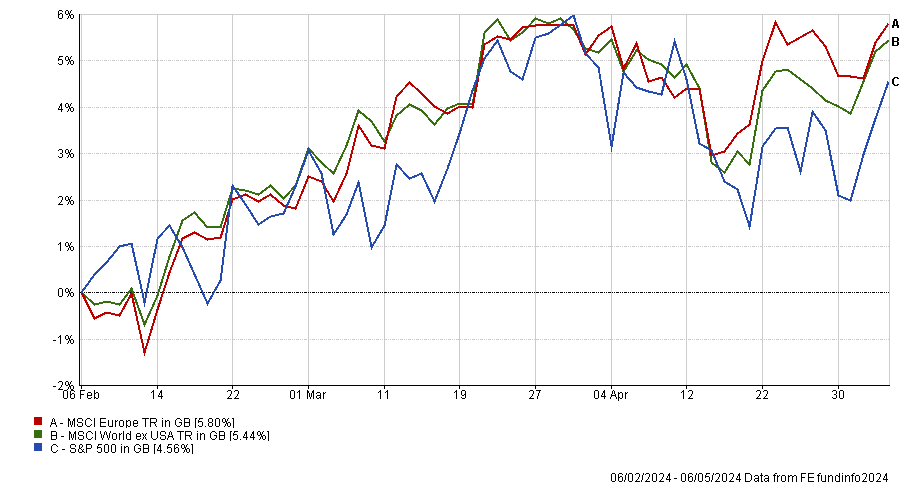

UK, European and emerging market equities could have their moment in the sun if the Fed doesn’t cut interest rates.

Markets outside the US will come to the fore if the Federal Reserve fails to cut interest rates this year, according to experts, who suggested investors might want to look outside of the world’s largest market if the central bank remains on its heels.

The market was quite upbeat at the end of last year, expecting the Federal Reserve to cut interest rates early in 2024, triggering a Christmas rally. Yet, things didn’t pan out as expected, with US inflation proving stickier than expected. Therefore, the question is now whether the Fed will cut rates at all in 2024.

For Peter Dalgliesh, chief investment officer at Parmenion, this change in expectations will have a big impact on equities, especially in the US.

He said: “The higher for longer backdrop of interest rates is likely to place increased challenge on the sustainability of growth and corporate earnings, raising risk of a de-rating in equity multiples, especially in longer duration sectors.

“As a result, care in identifying asset classes and sectors trading on attractive valuations and with a high confidence in being able to meet or exceed expectations is key.

He suggested US equities “look vulnerable to a pause” in the current climate, while the cheaper valuations and relatively low expectations for Europe, UK and the emerging markets mean stocks in these parts of the world look more attractive.

The caveat is the expected future direction of the dollar, with a sustained strength in the US currency usually correlating with a reduction in risk appetite – a headwind for non-US growth assets.

Dalgliesh added: “The dollar index remains some way below its 2022 highs with recent strength appearing to stall suggesting that investor risk appetite may be beginning to broaden.”

While a ‘no cuts this year’ scenario will likely impact investor sentiment across the board, Richard Carter, head of fixed interest research at Quilter Cheviot, believes bonds would suffer more than equities.

This would be in line with the dynamics in place since the beginning of the year. While equities have been generally more resilient, the higher-for-longer narrative has hampered the performance of bond indices.

Performance of indices YTD

Source: FE Analytics

To hedge against the risks of the higher-for-longer scenario, Carter pointed to very short duration bonds, cash and sectors that benefit from higher rates such as banks.

However, with government bonds yielding over 4%, Dalgliesh sees them as an attractive source of income and a way to protect a portfolio against downside risks in the event of a growth shock stemming from the delayed effects of tighter monetary policy.

He explained: “The continued inversion of the yield curve suggests this remains a possibility and shouldn’t be totally ruled out.

“In the same way with equities, care is required within corporate bonds having seen spreads narrow towards their historical lows, with a focus on quality, balance sheet strength and cashflow generation a necessity.”

Yet, Tom Becket, co-chief investment officer at Canaccord Genuity Wealth Management, is not overly worried about a no cuts scenario. While rate cuts would probably be helpful for most markets, he is not convinced they are necessary.

He said: “Bond prices are 'about right' and equity markets are marching to the beat of the economy's drums. Whilst the economy is ok, corporate profits are growing and inflation is moving in a progressively downward direction, we think the outlook for both bonds and equities is solid, but unspectacular.”

What if the Fed hikes rates again?

As US inflation has proved more persistent than expected, the market is fearing that the Fed might hike interest rates again, although Jerome Powell recently indicated that the US central bank is unlikely to move in this direction for now.

Dalgliesh explained: “Growth would need to be materially stronger and broad based for rates to move higher. It is widely acknowledged that real rates are already restrictive, so to move them even higher would require very strong data to be seen.”

However, if the Fed was to throw a curveball at the market and hike rates, the impact would likely mirror the no cuts scenario, leading to a weaker bond markets and volatility in equities, according to Carter.

In this situation, Dalgliesh expects value style equities, emerging markets, commodity as well as mid- and small-caps to play catch up as those asset classes have been beaten up out of fear of a recession.

There’s a real risk the economic cure ends up being worse than the disease.

The Bank of England’s Monetary Policy Committee (MPC) has voted to maintain the Bank Rate at 5.25%, postponing the much-awaited rate-cutting cycle further into the year.

The vote had a majority of 7 to 2, with two members preferring to reduce the rate by 0.25 percentage points to 5%. The tougher line prevailed, however, leaving interest rates at their 16-year high.

The outcome was priced in as a 95% chance earlier today, as noted by Tom Hopkins, senior portfolio manager at BRI Wealth Management, but markets are increasingly worried about the impact on the economy.

Nicholas Hyett, investment manager at Wealth Club, said that while the central bank continues to diagnose persistent inflation as the major danger facing the UK economy, “there’s a real risk the economic cure might end up being worse than the disease”.

“It’s an increasingly delicate balancing act. In this murky picture, the inclination is to sit on the fence a little longer, especially since cutting too early risks sinking sterling and kick starting another bout of inflation,” he said.

“Leave interest rate cuts too late though and the Bank risks accidently cratering the economy in its eagerness to get inflation under control. The MPC’s two dissenters clearly think that risk is growing.”

Inflation is now expected to return to around the 2% target in the near term, before rising again later in the year. Quilter Investors investment strategist Lindsay James said a process of gradual rate cuts “may soon begin” and that inflation is now close to being under control.

“Inflation is less likely to spike given energy prices are well off their highs and storage levels remain robust after a mild winter,” she said.

“Focus can thus turn to supporting economic growth at a time when the UK economy is struggling to escape the orbit of a growth rate that is effectively zero.”

While this feels significant, she also said it’s important not to get ahead of ourselves, noting that markets have been “a little giddy” in recent quarters about the prospect of interest rate cuts.

“The floodgates won’t simply just open. Central banks have a tendency to be fairly conservative and so expectations for just two rate cuts by year end look reasonable.

“Slow and steady will be the order of the day when the time comes for the Bank of England to start cutting,” she concluded.

Short-term factors make the region attractive, while valuations remain unchallenging.

European equities have been unloved for some time, making almost a third of the returns of their US counterparts over the past decade. As a result, Eurozone stocks are trading at a 20-30% discount to the US.

This is despite recent strong performance. Over the past six months the Euro Stoxx index has been the best major equity market, up some 19.2%, pipping the S&P 500 by 2.5 percentage points.

It raises the question of whether investors should dive into the resurgent market while they can still take advantage of the relatively attractive valuations on offer.

Sources: JP Morgan Asset Management, FTSE, IBES, LSEG Datastream, MSCI, S&P Global, data to 6 May 2024

Some, but not all, of the valuation gap can be explained by the American economy’s greater productivity and the US market’s larger weighting to tech stocks, said Niall Gallagher, manager of GAM Star European Equity. US companies spend twice as much as their European peers on capital expenditure and research and development (as a percentage of cash flow), he added.

Meanwhile, war in Ukraine has weighed upon the European market and China’s slowdown (European stocks rely heavily on exporting to Asia) has impacted some companies heavily.

However, with inflation coming down, energy prices cooling, rate cuts on the horizon and China starting to recover, the stage may be set for a European resurgence.

Trustnet asked some of the best-performing European equity managers, all of whom have been nominated for the FE fundinfo Alpha Manager of the Year awards, whether this a good time for investors to shift focus from the new world back to the old.

Europe is well placed to benefit from a near-term cyclical upswing

Frederic Jeanmaire, manager of the CT Pan European Focus fund, thinks many of the tailwinds holding Europe back for the past couple of years are dissipating.

“Interest rate rises that followed the inflationary impact of the Ukraine war are petering out, energy prices have fallen from their peaks and inflation is coming under control faster than in the US,” he said.

John Bennett, who manages Janus Henderson Investors’ Pan European and Continental European strategies, agreed. “In the near term, Europe as an export-oriented group of economies is coming back in favour, as the interest rate cycle is about to turn and macroeconomic lead indicators are improving,” he said.

“Europe is an early cycle trade. It shows in stock performance. European equities versus the S&P 500 are on fresh three-month relative highs. Europe is making multi-year highs versus the MSCI World ex-US index. After almost two years of steady outflows from Europe, the region is beginning to see inflows again.”

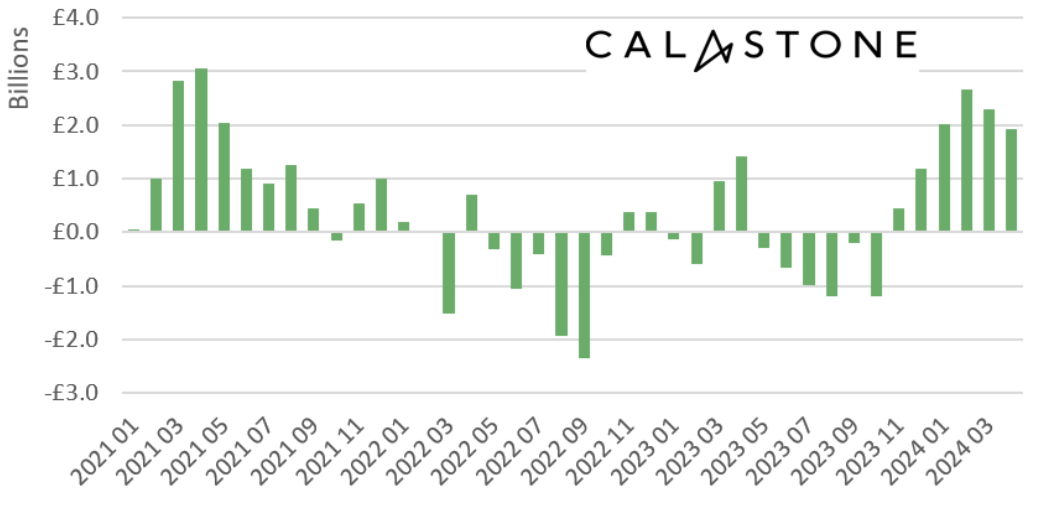

Indeed, UK investors ploughed £471m into European equity funds in April 2024 alone, Calastone’s Fund Flow Index found.

Europe vs S&P 500 and MSCI World ex-US over 3 months

Source: FE Analytics

Giles Rothbarth, who manages the BlackRock European Dynamic and BlackRock Continental European funds, also believes Europe could be about to experience a “near-term cyclical upturn”.

“The European equity market today provides the broadest opportunity set we’ve seen in decades – benefitting from a diverse range of themes, such as innovations in health care, energy efficiency and the growing need for higher compute power,” he noted.

“We believe European companies are well positioned to benefit from improving capital expenditure and investment. We can observe this in growth forecasts, with earnings expected to accelerate – a trend happening in end markets that have been depressed due to market shocks in recent years.”

Deglobalisation could play to Europe’s strengths

Two related factors driving that growth are onshoring and fiscal spending. Deglobalisation has already sparked a record amount of fiscal spending in the US and this is likely to continue as geopolitical tensions persist.

Bennett thinks this trend will create opportunities for stock pickers. “Enablers of deglobalisation (think industrial automation, digitalisation, electrification and construction materials firms) could thrive,” he said.

“We could also see a political shift in favour of populist/pro-labour policies, from both traditional 'left' and 'right' ends of the political spectrum. This could mean stronger wage inflation and greater labour market friction.”

These forces, as well as higher borrowing costs, are creating an environment where the strong are likely to get stronger. “Large incumbents across many industries (such as brewing, food catering and enterprise software) could see their already dominant positions enhanced as the end of virtually 'free' money tempers the threat of disruption by unprofitable start-ups,” Bennett said.

Old world stocks possess unrivalled heritage

Franz Weis, manager of the Comgest Growth Europe Compounders fund, thinks that focusing on Europe’s relatively cheap valuations is missing the point – the quality and long-term heritage of Europe’s companies are what makes them so attractive.

“The beauty of Europe is the heritage of its companies and the quality which often comes with it. The companies we’ve assembled in Comgest Growth Europe Compounders fund are on average 130 years old,” he explained.

“It is very difficult to find such companies in the much younger emerging markets and even in the bigger US market, which is dominated by the comparatively young tech industry. Even Microsoft, one of the oldest tech companies, is only 49 years old.”

Some of the world’s strongest consumer and luxury brands are based in Europe, including Hermès (founded in 1837) and Ferrari (founded in 1939). Both of these companies are unique, he said. “They keep supply tight, have a strong new business pipeline and continuously develop their brands with a long-term view.”

Another example is the high tech and precision engineering industry. “You can find a lot of gems in Europe built on a strong heritage and protected by strong moats. Carl Zeiss is a company which is 208 years old and has developed unique precision optical technology for centuries,” Weis said.

“Carl Zeiss also delivers high precision optics to ASML, the Dutch giant supplying the lasers crucial for global semiconductor manufacture, allowing it to do EUV lithography.”

Jeanmaire concurred. Within industrials and aerospace, Airbus is an example of “European know-how leading to long-term enduring competitive advantage,” he said.

“Europe also contains several outstanding consumer goods brands distributing their product globally. Inditex, the owner of Zara, boasts strong brand and supply chain advantages over its competitors,” he added.

Three reasons to buy Europe

Gallagher also said there are plenty of reasons to invest in Europe other than attractive valuations.

First, “there is a greater sectoral diversity across European stock markets in contrast to the US where technology is so dominant,” he said. Second, “Europe could be said to have a more value bias, such that if the markets shift towards a less benign global growth outlook, value could come back into favour.”

And finally, European companies offer greater geographical diversity. They earn half their revenues from outside of Europe on average and have more exposure to Asia than US companies.

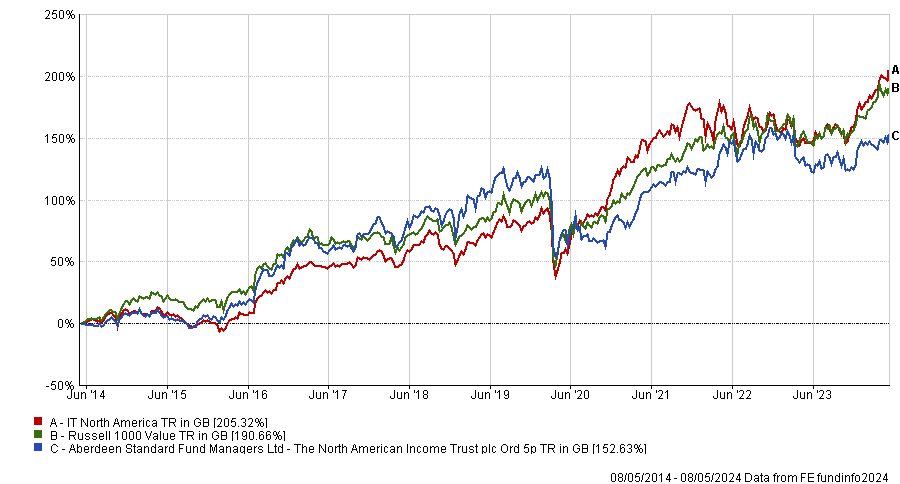

Fran Radano will continue to manage the portfolio with the support of Janus Henderson’s US equities team.

The board of The North American Income Trust has selected Janus Henderson as its new investment manager. The appointment will take effect in the third quarter of the year, pending the trust’s passing of the continuation vote.

This decision comes after a review of its existing management arrangements with abrdn and engagement with several other management groups.

The North American Income Trust’s board highlighted Janus Henderson’s “large and well-resourced” North American analyst team as a benefit for shareholders.

Board members expect this switch will lead to the creation of a portfolio of high-quality companies, characterised by revenue, earnings and dividends growth as well as to the reduction in the investment trust’s management fee.

Current manager Fran Radano will remain at the helm of the trust. He resigned from his role at abrdn and has agreed to join Janus Henderson where he will be supported by a team of 36 US equity analysts.

Dame Susan Rice, chair of The North American Income Trust, said: “Radano has managed the company’s portfolio for over 10 years and we believe that working closely with Janus Henderson’s broad and experienced equities desk in the US will bolster his ability to continue to find attractive investment opportunities in the North American market.

“Janus Henderson has strong credentials in North American equity income investment and we believe that this will lead to improved NAV performance while maintaining the company’s attractive dividend.”

The US equity team at Janus Henderson manages £180bn of assets and consists of 15 portfolio managers headed by head of US equities Marc Pinto.

Performance of investment trust over 10yrs vs sector and benchmark

Source: FE Analytics

Over the past decade, The North American Income Trust has lagged both its benchmark and the IT North America sector, having only outpaced Middlefield Canadian Income Trust. It also sits at the bottom of the sector over five years.

Ewan Lovett-Turner, head of investment companies research at Numis Securities, said the move was “interesting”, noting that shareholders should benefit from a 13 basis point reduction in fees. Janus Henderson is also waiving three months’ worth of fees for shareholders while the trust moves across.

“However, some shareholders may have been hoping for more radical changes, given underwhelming relative performance under abrdn,” he said.

“It will be interesting to see if this is enough to stimulate additional demand with the shares currently trading at a 14% discount.”

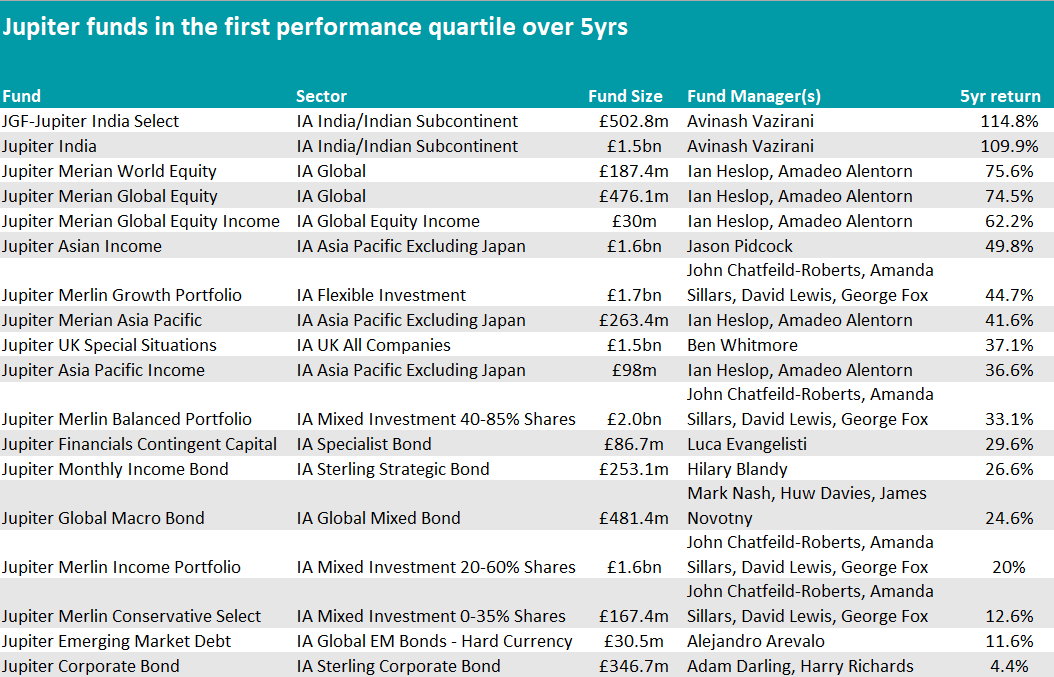

The firm’s UK strategies have underwhelmed, but Asia and fixed income are flourishing.

Investment styles go in and out of favour and funds’ performance ebbs and flows accordingly. Within the natural swings of the market, however, fund houses have specific sector expertise that will shine through at times when another segments of the offering may languish.

In this new Trustnet series, we aim to explore just that, highlighting the strengths and weaknesses of different asset managers in specific areas. This week, we begin with Jupiter.

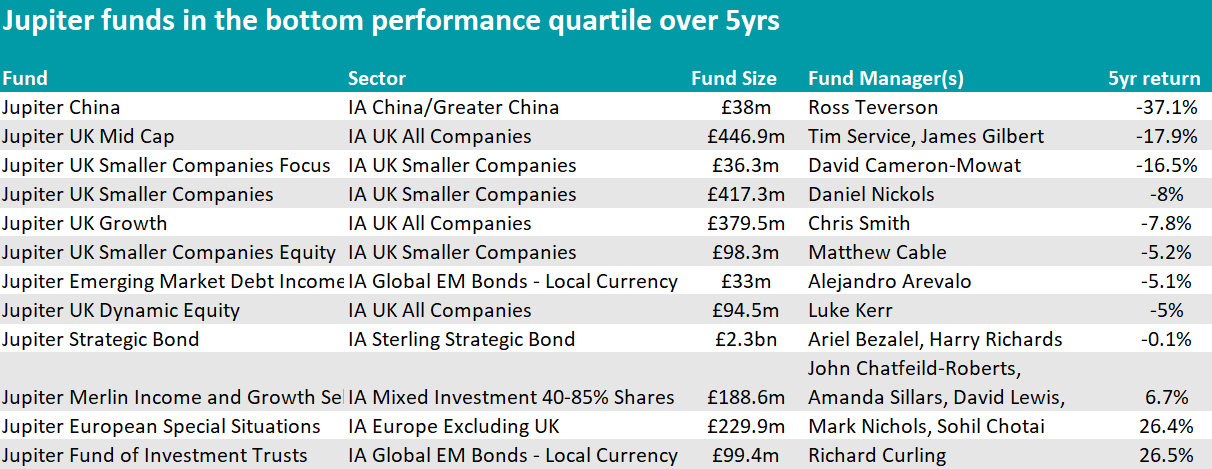

On a company level, latest results haven’t been particularly encouraging, with pre-tax profits falling by £48m to £9.4m in 2023 on the back of £2.2bn in net outflows, as the firm announced in February.

Money has flowed out of Jupiter’s most recognised vehicles, with Jupiter UK Special Situations shedding £300m and Jupiter Global Value £115.7m, as star manager Ben Whitmore announced his departure from the company, leading analysts to drop these strategies from their best-buy lists.

People also withdrew £263.8m from the Jupiter Income Trust, as Trustnet highlighted before, and the departure of Chrysalis Investments and its managers Richard Watts and Nick Williamson also led to an £800m reduction in Jupiter’s assets under management (AUM).

These departures hit the company hard, despite hiring veteran names such as Adrian Gosden and Chris Morrison, who joined Jupiter from GAM at the start of the year, and FE fundinfo Alpha Manager Alex Savvides from JO Hambro Capital Management, to take over Whitmore’s funds.

From a performance perspective, it is in the UK where Jupiter’s funds have struggled the most. Whitmore’s Jupiter UK Special Situations is the only domestic fund in the asset manager’s suite to have outperformed the market over the long term, while all other IA UK All Companies and IA UK Equity Income strategies in the Jupiter stable have underperformed their peers.

Facing a particularly harsh environment, the UK small-cap team, who ran the sector’s most popular fund back in 2021, have suffered from outflows ever since, as investors turned their back on UK equities in general and UK small-caps in particular.

The Jupiter UK Smaller Companies, UK Smaller Companies Equity and UK Smaller Companies Focus funds have underperformed both the IA UK Smaller Companies sector and the Numis Smaller Companies index over the past 12 months, three and five years.

Jupiter UK Smaller Companies Equity and UK Smaller Companies Focus did surpass the average peer in the past decade, however, as the table below illustrates. They are managed by Matthew Cable and David Cameron-Mowat, respectively.

Source: FE Analytics

All three strategies also featured in Trustnet's 'bang for your buck' series, where they stood out with the lowest alpha scores of the past five rolling years, meaning that they haven’t been able to add extra returns on top of their benchmark.

The biggest of the three funds, Jupiter UK Smaller Companies, is run by FE fundinfo Alpha Manager Daniel Nickols and used to be the most popular fund in its sector, peaking at £1.5bn in assets under management (AUM) in September 2021 and then going on to experience significant outflows.

According to Rob Morgan, chief analyst at Charles Stanley Direct: “The fund became a bit of a victim of its own success.”

Known for his “multi-cycle experience and intimate knowledge of the UK small-cap market”, Nickols has endured “an exceptionally tough period”.

Performance problems mostly stemmed from a wretched year in 2022, when growth-orientated smaller companies faced the sudden and significant headwind of much higher interest rates.

Bestinvest managing director Jason Hollands said that “in large part, this was down to the strong growth style bias being hit hard during a period of rising interest rates and borrowing costs”.

“It is also a relatively concentrated portfolio for a small-cap fund, with circa 56 holdings, which does leave it more vulnerable to stock-specific risk than more diversified products.”