Retirees and those saving for retirement often invest in poorly performing funds, an AJ Bell study finds.

Some 90% of pension funds have failed to beat a UK equity tracker over the past decade, according to data from AJ Bell, which showed the scale of poor performance suffered by those saving towards retirement.

The benchmark has hardly been a demanding one. Indeed, the FTSE All Share index – which was used in this study – has been one of the worst performing markets globally over 10 years, as the below chart shows.

Around three quarters of the underperforming funds failed to beat the index by at least 10 percentage points, the study found, while more than a third were 20 percentage points behind or more.

It is worth noting however that not all are 100% invested in equities and will have other assets such as bonds and alternatives, which will have impacted performance.

Laith Khalaf, head of investment analysis at AJ Bell, said: “This doesn’t look like a market which is serving consumers well, and yet tens of billions of pounds are invested in pension funds posting disappointing performance.”

Performance of indices over 10yrs

Source: FE Analytics

Included in the list of underperformers were Standard Life/Invesco Perp High Income 4 Pension, which was the worst of the group, making just 13% over 10 years. This included a 0.25% platform cost per year, which was taken into account, although pension funds have different share classes and it is possible some performed better than others.

Standard Life UK Equity 4 Pension (44.5%), SE Ethical Pension (46.7%), Scottish Widows UK Equity 2 Pension (47.5%) and Sun Life Canada CLIC Equity 1 Pension (47.7%) rounded out some of the worst “big funds with small returns”.

Poor performance can have seriously damaging effects in the real world, Khalaf said, as it will dramatically impact the size of savers’ pension funds when they retire.

“If you are able to get a 6% net return on a £50,000 pension pot for 20 years you will end up with £167,357. Reduce that return to 4%, and you end up £57,801 poorer, with a pot of just £109,556.

“Returns from the UK stock market itself haven’t been great over the past decade, but funds which have fallen significantly behind a tracker add insult to injury.”

There are several reasons why pension funds are performing so poorly. First is that many were set up decades ago before the invention of tracker funds. Instead, they invested in ‘closet trackers’ which charged active management fees, Khalaaf said.

Another is that charges on older pension plans tend to be higher. Khalaf said they “look high by modern standards, because they were set a long time ago before investment and platform costs started to fall”.

For example, Stakeholder pensions were popular in the early 2000s. They were marketed as a low-cost scheme with a maximum cost of 1.5% per year for the first 10 years and 1% thereafter.

“But you can now buy an index tracker fund for an annual charge of under 0.5% in a SIPP, and many successful active funds will cost less than 1% per annum including platform charges,” Khalaf noted.

The final reason is the “inertia tax”. This is a result of many pension schemes now being closed to new money, which has meant there is a lack of motivation to improve the products.

“The Financial Conduct Authority’s (FCA’s) Consumer Duty regulation will apply to closed books from July, which should in theory help drive improvements for investors in closed pension funds. There is still the risk that providers drag their feet, are hamstrung by the original pension fund mandates, or make improvements which still fall far short of the most competitive pension plans now available to savers,” the AJ Bell head of investment analysis said.

All savers should assess the performance of their pensions by requesting a performance factsheet and compare the fees they are being charged. Some older pensions can charge as much as 2.4% per year, according to a 2019 paper by the FCA.

“As a rough rule of thumb, you can now buy a UK tracker fund for around 0.3% to 0.5% including platform costs, and an active equity fund for around 1% to 1.2% including platform costs. Some active funds, especially multi-asset funds, cost significantly less,” Khalaf said.

If you are being overcharged or find you are in a poorly performing portfolio, it could be time to transfer to a cheaper or better performing option.

There is a rich vein of opportunity in European smaller companies that provide essential tools for the technology and healthcare sectors.

California in the 1840s was at the centre of the gold rush, which created enormous excitement, as prospectors and investors went in search of their fortune.

However, the real winners weren’t the gold mine owners or the landlords who leased the land but rather individuals such as Samuel Brannan, who became a millionaire selling picks and shovels to miners, and companies such as Levi’s (Levi Strauss travelled from Germany to California), which began providing durable clothing to workers.

Both Brannan and Strauss were able to profit from growth in the overall industry by providing critical products and services.

California is once again the centre of investors’ attention, and this time the excitement is about silicon, or, put more simply, technology. With the Magnificent Seven stocks (Apple, Microsoft, Nvidia et al) and the explosion of data creation, manipulation and storage, we see many parallels with the original gold rush.

Generative artificial intelligence (AI) and related services are turbo-charging data consumption, and the companies providing the tools that create and store this data stand to benefit most from the growth opportunity.

During this current gold rush, European companies once again are among those providing the ‘picks and shovels’.

Critical tools

Large companies such as ASML or ASM, two the world’s biggest suppliers to the semi-conductor industry, tend to get all the plaudits, but in Europe’s smaller companies universe there are several standout names providing critical tools and infrastructure to the supply chain.

There are two Swiss companies which, we believe, are well-placed to benefit from this structural trend. Firstly, VAT, the world’s leading vacuum valve producer, will see increased demand as more tools require high-integrity vacuums, with its valves (picks) being critical in getting to those ever-smaller node sizes.

The second, Comet, stands to benefit meaningfully from the AI revolution as more complex chip architectures are required, and in turn its plasma technologies become even more integral to the manufacturing process.

However, California’s Silicon Valley is not the only site of a current gold rush – we see structural growth in other areas. For example, health efficiency and the ability of blockbuster products to help reduce healthcare spending remains a focus given ageing populations and indebted governments.

As with the technology sector, stock market participants tend to focus on the headline names, for example Lilly and Novo Nordisk, when looking at the growth of GLP-1 based obesity drugs. But delve beneath the surface of the industry and analyse the supply chain and one can uncover some highly attractive ‘pick and shovel’ makers in the European smaller companies space.

Swiss company Bachem manufactures the ‘P’ (peptide) in the GLP-1 name – the key active ingredient for the drug. Capacity is in short supply and, with its reputation for quality and delivery, we think Bachem stands to benefit from the booming industry.

Dig deeper still into the GLP-1 supply chain and you find two German companies, Schott Pharma and Gerresheimer, which supply the devices (vials, synergies and injectable pens) that allow the drugs to be administered. These devices are designed into the manufacturing process, verified by the regulator and therefore hard to displace once the contract is won. This gives the companies and investors like us confidence in the future cashflows and growth trajectory of these businesses. Furthermore, there is a large and growing pipeline of biologic drugs in addition to GLP-1s that will drive demand for their products.

As we look across our portfolios, we see numerous other examples of ‘pick and shovel’ makers: Weir Group (mining equipment), Carel (control units for HVAC equipment), Tecan (sophisticated diagnostic machines for labs) and engcon (innovative tiltrotators to the excavator industry). The European smaller companies universe is rich with businesses that have important attributes.

One might ask, why not buy the company that is at the forefront of development — or the large-cap names we have all heard of? Because, as in the gold rush of the 1840s, we believe that by buying the pick and shovel maker, you are betting not on a single ultimate winner in the industry but on the entire industry winning.

Structural growth

By buying businesses that can grow along with industry volumes and more importantly provide unique and critical components for the industry’s infrastructure, you reduce the competitive (or regulatory) pressures often faced by the larger players, yet still benefit from the structural growth of the sector.

Our view is that investors will be rewarded by owning businesses that provide a specific service or product to the industry, where the competitive moat is high, where the products are ‘under the floorboards’ of the customers and where the industrial niche is relatively concentrated.

The European smaller companies sector is rich with businesses such as these. However, the focus on the Magnificent Seven in the US and the Super Six in Europe has meant less attention has been paid to this area of the market. We believe this allows investors to find businesses exposed to the same growth themes as well-known large caps – at more attractive prices. It also allows investors to diversify their risk, as often these companies provide for the entire industry, rather than being reliant on a single customer.

European smaller companies comprise a unique area of the global stock market, and with a quality growth philosophy one can access these ‘pick and shovel’ businesses and thus partake in gold rushes around the globe.

Phil Macartney is an investment manager, European equities at Jupiter Asset Management. The views expressed above should not be taken as investment advice.

Experts prefer UK small-cap funds with £60m to £200m, but a larger size is acceptable for US strategies.

The size of a fund is an important metric, as it can impact the manager’s ability to apply their investment philosophy.

This is particularly true for funds specialising in small-caps due to liquidity considerations. For instance, a fund that has become too big will have to take excessively large positions in small companies, creating concentration and liquidity risks.

Another risk is that the fund may have to increase its exposure to larger, more liquid businesses, which would dilute its genuine small-cap exposure. In other words, this could turn a small-cap fund into a mid-cap portfolio.

Kamal Warraich, head of equity fund research at Canaccord Genuity Wealth Management, said: “A small-cap fund’s maximum size is based on ‘capacity’, which is essentially how big a total strategy can get (strategy meaning all funds and mandates run under the same philosophy and process) before it has to abandon its current investment approach.

“Many things can impact a strategy, but the most important considerations in my opinion are: size and speed of fund inflows, breadth and depth of the investable universe and liquidity profile of the fund.”

There is, however, no magic number for how big a small-cap fund can get before its size becomes a hurdle. It depends on the average market capitalisation of underlying companies, the size of positions the manager intends to take and the breadth of the market.

Nick Wood, head of fund research at Quilter Cheviot, said: “For example, small-cap investors in the US are likely to hold much larger and more liquid companies than counterparts elsewhere simply down to the structure of that market."

While US small- and mid-caps tend to be relatively large and would, in some instances, be considered large-caps if listed elsewhere, UK and European smaller companies are much less liquid.

Rob Burgeman, investment manager at RBC Brewin Dolphin, said: “The perils for a larger fund, then, of finding themselves stuck in lobster pots – investments that they can get into but not out of – are increased.

“This can be a problem, as successful strategies attract greater flows of funds. These funds then pour into the same holdings, boosting their prices further and increasing the returns of the fund. However, when the tide turns, the fund manager can find that the only buyer of some of their larger holdings was themselves. Prices then start to fall sharply, redemptions increase, and it becomes something of a vicious circle.

“Good fund management houses will soft close and then hard close their funds to prevent them growing too large and avoid this issue.”

For UK smaller companies funds, which invest in a less liquid market, the sweet spot is under £200m, saidTom Hopkins, senior portfolio manager at BRI Wealth Management. A size range between £60m and £200m is “ideal for active, concentrated, yet liquid portfolios”.

He warned against funds exceeding £500m in assets under management as they may need to increase their exposure to large- and mid-caps.

While smaller funds are generally better in this asset class, there are risks associated with buying units in tiny funds.

Hopkins explained: “The risk of investing in a fund that’s too small is that your deal size could make you a significant shareholder within the fund, which some investors may find uncomfortable.”

While Hopkins would back a fund as small as £60m, Burgeman is wary of funds under £100m.

“A micro fund is going to struggle to generate the returns required to be financially viable for the fund management group, leaving it exposed to the prospect of being abruptly shut or merged with another strategy,” Burgeman said.

“This is okay, maybe, if a fund has just launched and there is reasonable prospect of it reaching critical mass within an acceptable period.”

Small-caps have been deeply out of favour in the UK and elsewhere in recent years. Data from the Investment Association showing that the size of small-cap equity funds has contracted from £14.5bn five years ago to £9.8bn today, as a result of both outflows and disappointing returns.

Yet, easing inflation and the potential for rate cuts this year could benefit smaller companies, which are trading at significantly lower valuations than the wider UK market.

Hopkins concluded: “As smaller companies remain undervalued, we will continue to see heightened M&A activity from overseas and private equity buyers if these valuations continue.

“For a long-term investor, the current valuation of the UK small-cap market provides an attractive buying opportunity as the market still has plenty of high-quality and exciting businesses for investors.”

Jefferies and Peel Hunt one, short sellers zero as the brokers’ buy ratings prove prescient.

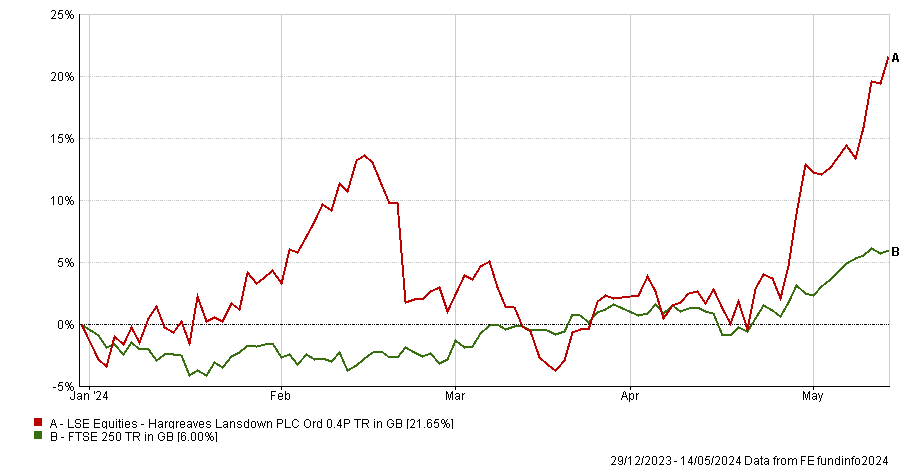

Hargreaves Lansdown’s volatile share price has rebounded strongly since March 2024, although it is still way off its 2019 peak. Broker Jefferies has issued a buy rating for the platform’s stock in the belief that its fortunes are turning around under new chief executive Dan Olley and Peel Hunt recently reaffirmed its buy rating.

Nonetheless, Hargreaves Lansdown remains one of the UK’s most shorted stocks judging by the percentage of its share capital disclosed to be in the hands of short sellers (5.5% at the end of April 2024, according to the Financial Conduct Authority).

Hargreaves Lansdown’s share price year-to-date vs FTSE 250

Source: FE Analytics

Analyst recommendations are split with six analysts expecting Hargreaves Lansdown to underperform, five saying it will outperform, three buys, four holds and one sell, according to the Financial Times as of 9 May 2024.

So, who is right? And should you buy, hold or fold Hargreaves Lansdown’s shares?

Eric Burns, chief analyst at Sanford DeLand, sides with Jefferies and Peel Hunt. Hargreaves Lansdown is a high beta play, so he expects its shares to perform well if the UK and global stock markets – which hit fresh highs last week – continue to rise.

“I struggle to follow the logic of being short a stock like HL when the FTSE is reaching new highs on a daily basis. Rising markets provide an organic uplift to assets under administration – HL’s key performance metric – even without it adding new customers,” he explained.

“Following the sell-off, we have a business with a free cash flow yield we estimate of about 7.1% this year, rising to 7.5% next. This puts it very much in the ‘value’ category.”

Peel Hunt agreed that the platform looks cheap. “Hargreaves Lansdown is now trading on a December 2024E EV/EBIT of c.8x, or a price-to-earnings ratio of 12x, well below the other listed platforms,” the broker said on 30 April 2024, reiterating its buy recommendation. “We do not believe the longer-term prospects are being reflected in the share price.”

Sanford DeLand has held Hargreaves Lansdown (HL) in its CFP SDL Buffettology fund since October 2014. It also owns AJ Bell in its CFP SDL Free Spirit fund. “We love platform businesses; they are very scalable and tend to exhibit the sort of returns we are looking for,” Burns said.

“In the case of HL, return on average equity is in excess of 50% and conversion of reported earnings into free cash flow is high. Despite all the negativity you will hear, this is a business that has grown revenue at a 10%+ compound annual rate over the past 10 years during which time active clients have gone from 507,000 to over 1.8m. It’s the sort of steady compounder we like.”

Hargreaves Lansdown has benefitted from the higher rate environment through its popular Active Savings product which enables savers to achieve a better rate of return on cash, Burns added.

“There have also been regulatory concerns regarding the interest platforms earn on client cash balances although this appears to be ameliorating,” he noted.

Julian Roberts, an equity analyst at Jefferies, argued that although Hargreaves Lansdown is not the cheapest investment platform, its pricing is competitive – and fees are not as critical to customer loyalty as the platform’s detractors may believe.

“Platform fees of 45 basis points (bps) are capped at £45 a year for shares. On an average account size of c. £75,000, that is 6bps. It is more than AJ Bell, which caps out at £25 (3⅓ bps), but the £20 difference is quite slim in the scheme of things, and HL would point to execution cost savings due to their larger size and network. This does not hold for all asset classes, but absolute differences are not huge,” Roberts explained.

“Perhaps more importantly, in our survey of UK savers this year, the two most expensive platforms were also the most popular, so we doubt that the target market is as price sensitive as people might think. Brand and service probably matter more.”

Roberts thinks that Hargreaves Lansdown’s sheer size masks its success at bringing in new customers. “HL fishes for new clients in the same pool as all of its competitors, but it loses them from a much bigger one. Lose 10% of 1.8m customers, and you need 180,000 new ones to replace them. AJ Bell can lose 10% and only need 35,000 new ones to grow,” he said.

“HL added 34,000 net new customers in the quarter to March 2024, versus 15,000 at AJ Bell, but the gross numbers are even further apart. We see this as a sign of brand strength.”

For Hargreaves Lansdown, this represented a 48% jump in net new clients compared to the first quarter of 2023, as its new cash ISA and ready-made pension portfolios proved popular.

Positive market movements also helped the platform to grow its assets under administration by 5% during the first quarter of this year to £149.7bn, according to Peel Hunt. Net inflows improved to £1.6bn, which was above consensus expectations.

Since coming onboard as CEO last year, Olley has had “a real impact”, Roberts continued. The former dunnhumby boss has “re-jigged the sequence and content of the investment programme, replaced the chief technology officer, brought in a new strategy office and a new corporate affairs director, and there have been results”.

The most recent addition to the investment programme is a range of passively-managed model portfolios, which will start trading next month.

On the other side of the equation, short-sellers have had plenty of reasons to bet against the stock during the past few years.

Having owned the platform for a decade, Burns acknowledged its fall from grace. “If you combine difficult market conditions with the unwanted connection to the [Neil] Woodford affair and a spat with its founder then I guess that’s fodder for the shorters,” he said.

The platform’s shareholders, Burns included, are hoping these headwinds are in the past and that momentum has turned in Hargreaves Lansdown’s favour.

In a further potential fillip to shareholders, Burns suggested that HL might join the increasing ranks of British companies catching the attention of overseas buyers.

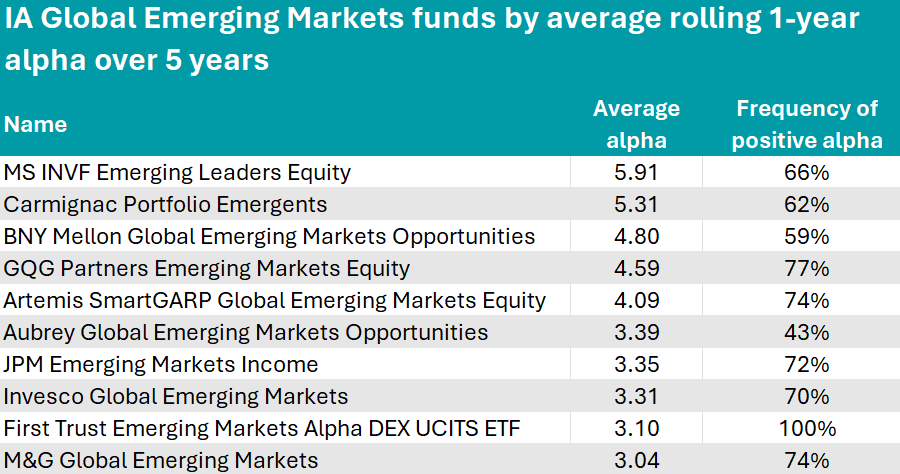

Morgan Stanley’s MS INVF Emerging Leaders Equity fund and Carmignac Portfolio Emergents outperformed the most over five years.

Active investing is all about stock selection and outperforming indices in order to give investors extra returns that they can’t get through passive funds.

By outperforming their benchmarks, managers can show that their decisions have benefitted the fund, keeping investors happy and justifying their higher fees.

In this series, Trustnet is looking at funds’ outperformance, as measured by alpha, over the past 61 year-long periods measured every month from 2018 to 2023.

Today, we analyse the IA Global Emerging Markets sector, where the Morgan Stanley Investment Management’s MS INVF Emerging Leaders Equity fund had the highest alpha score.

The $955.6m fund follows a benchmark-agnostic investment process whereby the manager Vishal Gupta focuses on companies that are poised to benefit from future growth themes.

His top three stocks are Brazil-based digital banking firm Nu Holdings (8.3%), Argentinian online marketplace MercadoLibre (7.4%) and Taiwan Semiconductor Manufacturing Company (7%).

Over the past five years, the fund outperformed its benchmark, the MSCI Emerging Markets index, by an average of 5.9% per annum.

Source: FinXL

The second-best fund was Carmignac Portfolio Emergents, with an average alpha of 5.31.

It is co-managed by Xavier Hovasse and Haiyan Li-Labbé, who combine a fundamental top-down approach with bottom-up analysis. The fund’s main country exposure is China (27.9%), followed by South Korea (18.4%) and India (14.4%). The top holding is Samsung (9.9%).

In third position, BNY Mellon Global Emerging Markets Opportunities concluded the podium with an average alpha of 4.8. It is managed by Liliana Castillo Dearth, although she joined Newton Investment Management in October 2023 – the fund’s track record prior to that was built by former managers Paul Birchenough and Ian Smith.

Other notable strategies in the list included the value-focused Artemis SmartGARP Global Emerging Markets Equity fund (average alpha: 4.09), which is recommended by FE Investments analysts as a core emerging-market fund. Its investment process “goes beyond deep value and distressed stocks to include a wider variety of factors”, they said.

The Aubrey Global Emerging Markets Opportunities fund (average alpha: 3.39) has a “strong consumer focus and growth-bias”, FE analysts said, making it a good fund for secondary exposure

Finally, the five FE fundinfo Crown-rated JPM Emerging Markets Income (average alpha: 3.35) also deserves a mention.

“In tough environments such as 2020, where many companies looked to cut their dividend payments, this fund’s ability to focus on capital appreciation provided it with resilience and the capacity to maintain total return generation in downward markets,” FE analysts said.

“Unlike traditional income funds, this fund takes a more flexible approach, in that capital appreciation is as equally important as income generation. The fund is best suited as a core emerging market exposure, with defensive characteristics for those seeking a source of income.”

There was only one fund in the whole emerging markets sector that consistently delivered a positive alpha throughout the past five years – the First Trust Emerging Markets AlphaDEX UCITS ETF.

With just £15.3m of assets under management (AUM), this overlooked exchange-traded fund (ETF) has beaten the benchmark it is tracking, the Nasdaq AlphaDEX EM index, with an average outperformance of 3.1% – higher than many active managers in the sector.

For this, it only charged 0.80%, in a sector where the average ongoing charges figure (OCF) is approximately 0.95%. Its main exposures are to China (18.1%), Turkey (15.3%) and Taiwan (11.63%).

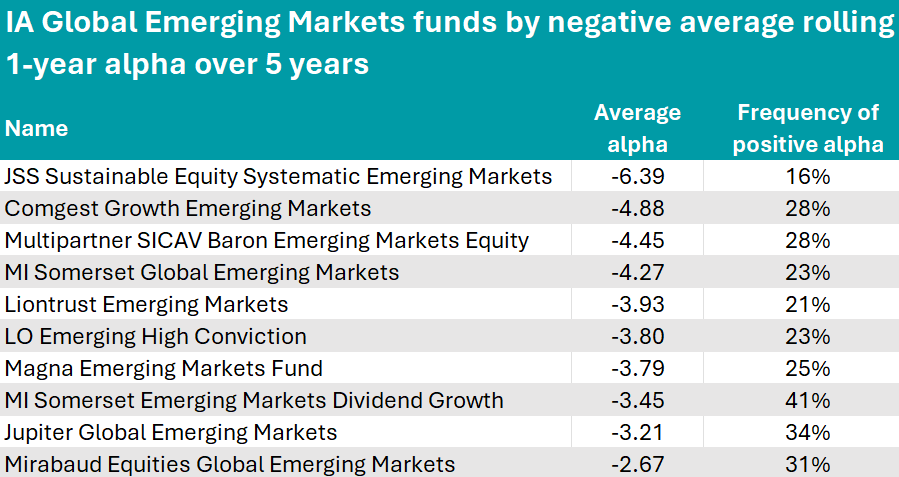

At the bottom of the table were funds with negative alpha, whose managers’ active decisions detracted from performance rather than contributed to it.

Source: FinXL

The most negative scores were those of JSS Sustainable Equity Systematic Emerging Markets (-6.39), Comgest Growth Emerging Markets (-4.88) and Multipartner SICAV Baron Emerging Markets Equity (-4.45).

Sectors previously in this series: UK Equity Income, UK All Companies, Global, Global Equity Income, Sterling bonds, smaller companies, global bonds, cautious funds, balanced and adventurous funds, European funds, Asia funds.

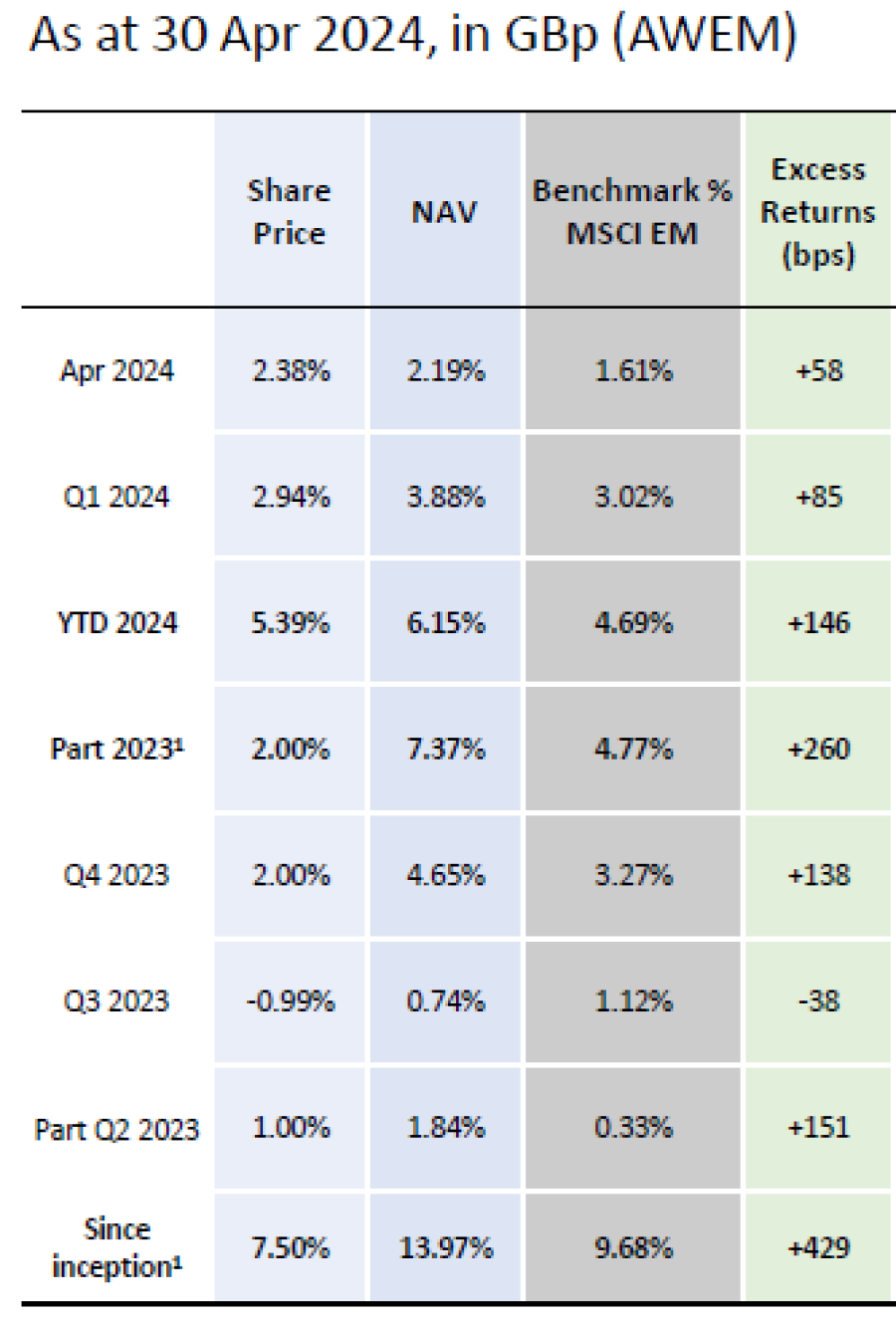

Prashant Khemka, manager of Ashoka WhiteOak Emerging Markets, believes that managers who don’t beat their benchmarks should not charge fees.

Ashoka WhiteOak Emerging Markets was one of just two investment trusts to go public last year amidst a period of drought in new listings for the London Stock Exchange.

This new fund aims to replicate the success of its stablemate Ashoka India Equity by applying the same investment philosophy to the broader emerging markets universe.

The £35m investment trust made the headlines again recently as it is looking to absorb its much larger peer, Asia Dragon Trust, to grow its assets under management and get onto the radar of a wider investor base.

Performance of fund

Source: WhiteOak Capital Management

Below, the founder of WhiteOak Capital Management, Prashant Khemka explains his strategy, how the investment trust structure enables him to generate higher alpha and why managers who don’t outperform their benchmarks should not charge fees.

Could you explain your investment strategy?

A crucial prerequisite to generate sustainable, peer group-leading performance over many years and market cycles is to have a robust investment culture. Everyone in our team is driven by a single-minded objective: to generate the highest return compared to anyone else in the peer group. We don’t have a top-quartile or top-decile mindset, but a sportsman-like mindset: we’re aiming for the gold medal.

We follow a stock selection-based approach, underpinned by the belief that outsized performance is generated by investing in great businesses trading at attractive valuations. We use an analytical framework, which also serves as a valuation framework, called ‘OpcoFinco’.

From a risk management perspective, an end objective is to maximise alpha while also minimising the volatility of that alpha.

What is the OpcoFinco framework?

To generate cash flow sustainably in the future, a company needs returns on incremental capital to be higher than the cost of capital.

When you find businesses that possess these attributes, you must value them logically and invest only if there is a substantial upside to fair value.

The OpcoFinco framework enables you to analyse a company through the prism of return on incremental capital and then to quantify the value of return on incremental capital.

Unlike many people, we don't use the price-to-earnings ratio at all. We think it's very misleading because it is distorted.

Could you explain your fee structure?

We have a 0% fixed management fee structure. We charge a performance fee on a three-year cumulative alpha basis, which means we only get paid if we outperform. The alignment of interest is strong because we can't just sit on our laurels and expect to get paid.

There are too many investment trusts out there that have never generated alpha, but are charging fees on an ongoing basis. There's very little accountability and I'm quite surprised to find that the accountability level is not as high as I would have expected in a developed market like the UK.

The 0% management fee combined with the annual redemption facility and performance of the trust should keep the discount very tight. In the case of Ashoka India Equity, we've generally been trading at a small premium versus a 15% to 20% discount for most of our peers.

Why did you choose the investment trust structure?

Emerging markets are inefficient segments of the global equity market and we have an overweight to small and mid-cap (‘smid’) companies because it’s an even more inefficient part of emerging markets. Being overweight smids doesn’t mean you are going to outperform but a good management team can generate higher alpha in that space.

Because it's closed-ended, the investment trust structure enables us not to worry as much about liquidity. Hence, we can allocate more capital in small-cap companies, which may not be appropriate from a liquidity management perspective in an open-ended vehicle.

It also allows investments in pre-IPO opportunities. It’s not possible to explore those opportunities in open-ended vehicles.

What has been the best-performing stock in the portfolio since launch?

The best performer has been Doms Industries, which is an Indian stationery and art material manufacturer. It produces things such as pencils, erasers and mathematical instruments. Basically, things students would use in school.

When I grew up, Doms wasn't around. We used all kinds of pencils that weren't necessarily branded. But now when I go back to India, I see that all the kids in the family are using Doms products.

Fila Group from Italy is an investor in Doms Industries and owns a good amount of its shares.

What about the worst-performing stock?

It has been Budweiser Brewing Company APAC, which is listed in Hong Kong. The Chinese market has been under tremendous pressure and most of our Chinese names are down 11% to 44%.

Following the reopening of China after Covid, it was expected that the demand for beer consumption would substantially normalise and get back to its earlier growth path, but like many other segments of the Chinese economy, consumption has been fairly tepid.

That is why Budweiser has derated.

The portfolio is underweight China relative to the benchmark. How do you approach this market?

We never form top-down views such as ‘China is in deep trouble, so we will underweight this market.’

However, the portfolio is overweight the most democratic countries and underweight the least democratic countries. We believe authoritarian regimes have lower alpha potential. Similarly, we are underweight state-owned enterprises and overweight private companies.

Now, if you reassign some of the companies in the portfolio that are exposed to China like South Africa’s Naspers (which has a sizeable stake in Tencent) as well as some off-benchmark names, our allocation to China is more or less in line with the benchmark.

How do you select your off-benchmark positions?

Most of them have three attributes: they derive the majority of their value from emerging markets, are high alpha opportunities and mitigate some factor risks in the portfolio.

For example, if you take France’s LVMH, 60% of its growth was driven by China alone in the 10 years prior to the Covid crisis and we estimate that a majority of its profits still come from emerging markets. It mitigates the underweight risk in China.

Similarly, Netherland’s ASML derives the majority of its value from emerging markets, has high alpha potential and mitigates the underweight risk in Taiwan.

What do you do outside of fund management?

I like to spend time with my family. I have three kids and we have a fund management competition going on between them. They have their own portfolios and try to outperform each other. It’s good fun to see the industry within the family as well.

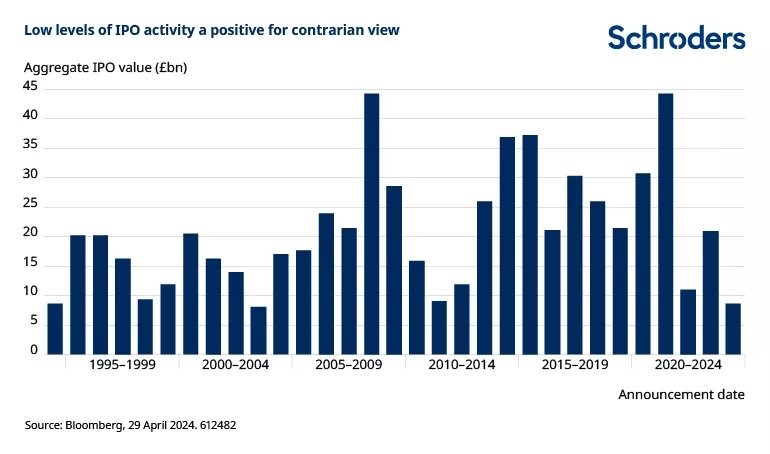

UK equities hit an all-time high this week but there’s plenty of petrol in the tank to continue fuelling this rally.

The UK equity market hit fresh highs this week and, while no-one wants to get in at the top of any market, there are many reasons to believe that this rally might only just be getting started.

With the benefit of hindsight, we would all have boosted our domestic equity holdings months ago, but some investment professionals think now still seems like a relatively opportune moment to get in on the action.

While many catalysts have converged to produce the recent rally (including an improvement in economic data, imminent rate cuts and voracious share buybacks) there are plenty more irons in the fire yet to make an impact.

FTSE 100 and FTSE All Share vs MSCI ACWI, year-to-date

Source: FE Analytics

One factor that could really move the dial would be inflows.

As Artemis Income’s Nick Shenton pointed out, the UK stock market has “been making all-time highs on a total return basis for a while [but] it’s not doing so from an extended position where it’s widely owned or the shares don’t [offer] value. We think it bodes quite well that it’s starting to make all-time highs without the aid of international investors coming back to the UK market, or even domestic investors”.

Meanwhile, private investors continue to pull money out of UK equity funds, channelling it instead into passively-managed global and US equity funds. Asset managers are bullish about the prospects for US large-cap stocks and European equities but not the poor old UK. Even wealth managers such as Coutts are turning their back on the UK – at precisely the wrong time, in my view.

The UK government is doing its best to stem the tide of outflows, launching the British ISA which is not expected to move the needle massively, but is a step in the right direction. It proves there is political will to take action to support the stock market, which is why Man Group’s Henry Dixon called the British ISA announcement in the spring Budget “a faint line in the sand moment”.

Jack Barrat, who co-manages Man GLG Undervalued Assets with Dixon, said the chancellor’s call for UK pension funds to disclose their allocations to domestic equities should give the stock market more “sunlight” and “greater attention”.

If the government were to go one step further and abolish stamp duty, that could encourage investors back into the stock market.

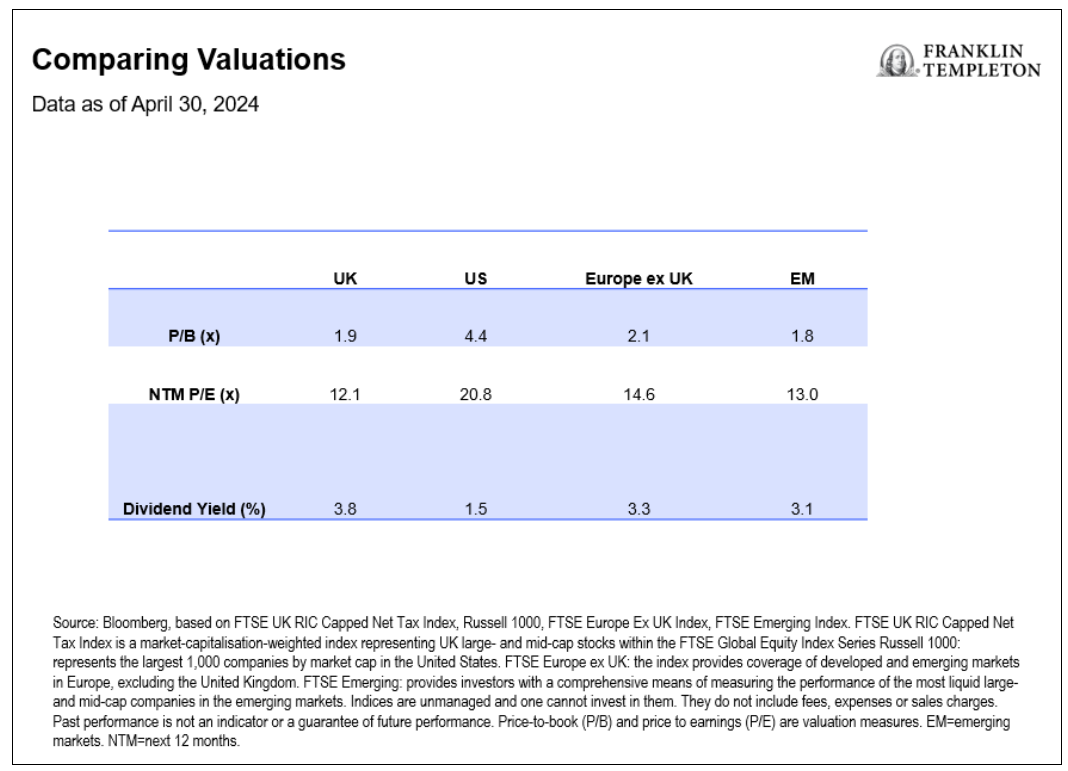

Valuations remain attractive despite this year’s gains, as the chart below shows.

Marcus Weyerer, senior ETF investment strategist, EMEA at Franklin Templeton, said: “With a price-to-book ratio of less than 2.0, UK equities are currently trading at a discount of more than 50% compared to US equities. Additionally, in terms of forward price-to-earnings, they are closely aligned with emerging market levels. Furthermore, the UK has long been considered a haven for income investors, and it currently boasts a dividend yield of 3.8%.”

Cheap valuations in a cheap currency have sparked a “frenzy” of merger and acquisition (M&A) activity, according to James Lowen, manager of JOHCM UK Equity Income. Five of his 60 holdings have been approached by bidders this year alone.

There has been a dearth of initial public offerings (IPOs) but if valuations were to surge, British companies might become more confident about going public here.

And if valuations better reflected what public companies are worth, management teams might be less eager to move their listings to the US.

A pickup in IPOs would create a virtuous circle, according to Graham Ashby, a UK all-cap fund manager at Schroders. “History clearly shows that increased UK IPO activity typically corresponds with a short-term peak in the equity market – witness the high levels of IPO activity in 2008 and 2021, compared with current depressed levels,” he said.

Meanwhile, companies themselves are cognisant of the value in their own cheap shares, so have been buying them back in droves. Buybacks – along with companies being taken out by foreign acquirers or moving their listings abroad – are gradually shrinking the size of the UK equity market.

Ashby observed that “less supply when demand may be set to increase” could eventually drive up prices. Quoting Warren Buffett’s maxim of being greedy when others are fearful, he concluded: “It may be time to get greedy.”

The overall cheapness of the UK market masks the fact that some of the UK’s largest stocks already appear expensive, Lowen warned. The seven “expensive defensives” (AstraZeneca, GSK, Diageo, Unilever, LSEG, British American Tobacco and RELX) look overvalued and comprise a fifth of the FTSE 100, which represents “a big danger lurking under the surface” for passive investors.

Other areas such as banks, insurers, miners and small-caps offer greater opportunities. That is why Lowen believes actively-managed strategies that can deviate away from the FTSE 100 index’s largest names would be a better way to play the UK recovery.

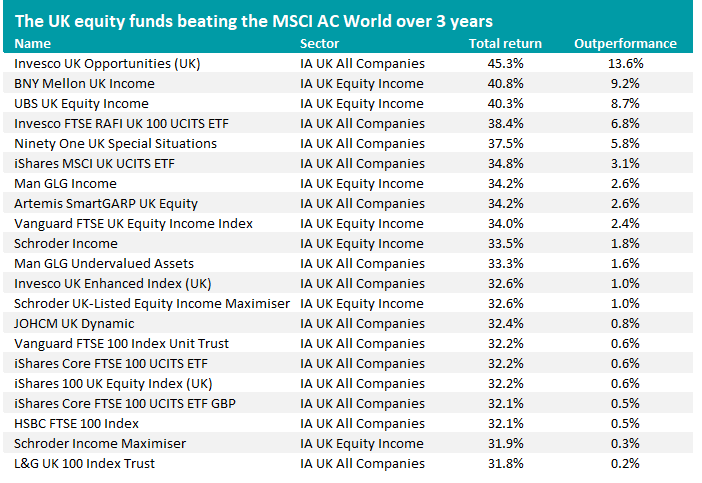

FE fundinfo head of editorial Gary Jackson set out to find the best performing active UK equity managers this week and found 21 funds that beat the mighty MSCI All Country World index over three years.

Five funds even outperformed the MSCI ACWI by more than 5% (Invesco UK Opportunities, BNY Mellon UK Income, UBS UK Equity Income, Invesco FTSE RAFI UK 100 UCITS ETF and Ninety One UK Special Situations).

This is no mean feat, dominated as the global index is by the US, which has outperformed the UK mightily.

If these fund managers can surpass global equities during a period where the UK has been a laggard, what might they be capable of at the helm of a more buoyant opportunity set?

This could be an attractive entry point into the asset class, say experts.

Small-caps have been deeply out of favour in the UK and elsewhere.

Every month over the past year, the size of small-cap equity funds has shrunk by a third, contracting from £14.5bn five year ago to £9.8bn today, according to data from the Investment Association. This shrinkage has been caused by both outflows and disappointing returns, which have averaged at -15% over the past three years.

But with UK economic growth now improving, inflation easing and signals that a rate cut could come as soon as next month, some of this negative sentiment could start to lift, according to Bestinvest managing director Jason Hollands.

He declared: “It could be quite an interesting time to dip the toes back in.”

“Small-cap stocks are inexpensive and another factor to consider is that the whole UK market is basically up for sale to international bidders at the moment, who can see plenty of value opportunities,” he added.

His message was echoed by Sheridan Admans, head of fund selection at TILLIT, who said the expectation that rates have stabilised or will potentially be cut later in the year “has provided a catalyst for rising investor interest”.

FundCalibre managing director Darius McDermott added that today’s cheap valuations, which are unlikely to last over the long term, represent a “good potential entry point”.

For investors who are tempted by these opportunities, below is a selection of domestic and international small-cap funds to consider.

UK small-caps

Hollands went with the River & Mercantile UK Listed Smaller Companies fund and, for investment trust fans, Henderson Smaller Companies.

The former is managed by George Ensor with a focus on the smallest 10% of companies on the UK market.

“The ES River & Mercantile process includes growth, value and recovery buckets, so the fund has performed well in a variety of market environments,” he said.

Henderson Smaller Companies, managed by veteran Neil Hermon, includes exposure to mid-cap stocks in the FTSE 250.

“It has a quality growth approach and will ‘run its winners’, holding on to its winners as [they ascend] into the mid-cap arena. In common with most UK equity investment companies, it is trading at a fairly big discount at the moment, -13%, which should appeal to bargain hunters,” Hollands concluded.

Admans also admires the River and Mercantile fund, but suggested the Aberforth Smaller Companies trust as another option, with its “unique approach” to investing in companies that are out of favour.

“Its focus on turnaround stories or value investing is a refreshing alternative to the more popular growth-focused funds in the market,” he said.

“What sets Aberforth apart is its team-based approach and its emphasis on dividends and a company's ability to pay them.”

Despite its success, the trust is currently trading at an 11.6% discount to its net asset value, presenting “a great opportunity for investors who are looking for exposure to Aberforth’s specific niche of deep value UK small-caps”.

Other picks included Liontrust UK Micro Cap, favoured by Pharon Independent Financial Advisers head of fund solutions Andrew K O’Shea. It has been "successfully managed" on a team approach by Anthony Cross, Julian Fosh, Victoria Stevens and Matt Tonge since its launch in March 2016 and they have more recently been joined by Alex Wedge and Natalie Bell.

The fund is managed using the "Economic Advantage" investment approach that looks to identify companies with a durable competitive advantage by generating – and more importantly, sustaining – a higher-than-average level of profitability.

"Companies that are successful in gaining a place in the portfolio must also have a minimum percentage of the share ownership held by senior management," said O'Shea.

"The fund currently has a bias towards the technology and industrials sectors, which together account for approximately 50% of the portfolio."

McDermott highlighted the IFSL Marlborough UK Micro Cap Growth fund, which has gone through a period of poor performance due to its style being out of favour but “will recover when the wind changes”.

Small-caps overseas

But it’s not just in the UK that smaller companies could come rally from their low valuations. McDermott was also bullish on US and European small-caps, where many world-class, high-quality companies are trading below their intrinsic value.

To tap into a European small-cap recovery, he highlighted Janus Henderson European Smaller Companies.

“Backed by a large and experienced investment team, this is a true stock picker’s fund where the managers are happy to invest across the entire universe to deliver returns,” he said.

For exposure across the board, abrdn Global Smaller Companies is a “textbook global small-cap fund”, said McDermott.

Based around abrdn’s screening tool 'Matrix', which former co-manager Harry Nimmo helped create, it identifies smaller companies from all around the globe, including in emerging markets, that are believed to have the best growth prospects.

Finally, for investors looking for exposure to the largest stock market in the world and one of the most dynamic parts of it, Admans chose the Artemis US Smaller Companies fund.

“The managers take a flexible approach and aren’t wedded to either growth or value but they look for the large companies of tomorrow,” he said.

“As such, there is a slight preference for long-term structural growth sectors like technology and healthcare. The team managing this fund has significant experience and a track record of investing in US small-caps.”

Investment decisions are driven by both macroeconomic views and bottom-up stock picking, he added.

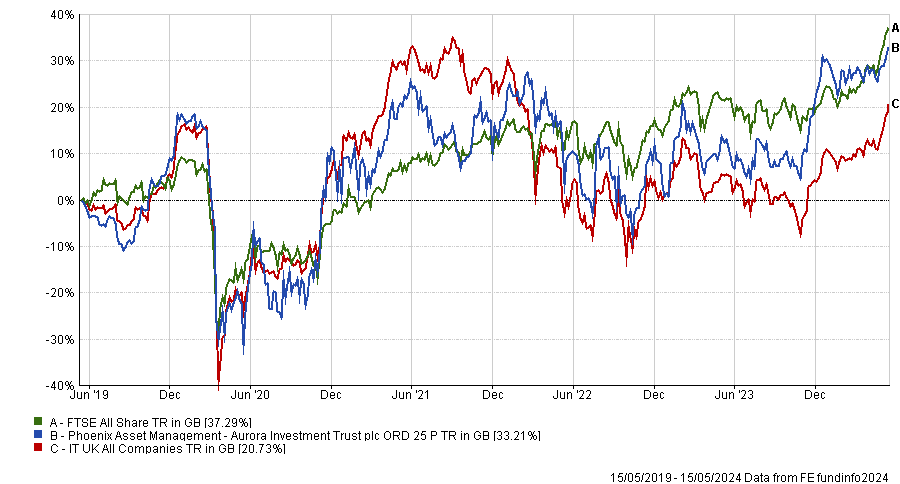

There is more growth in airlines and banks than people think, according to Phoenix Asset Management's Gary Channon.

Airlines and banks aren’t usually thought of as growth areas, but they have the potential to surprise sceptical investors, according to Gary Channon, manager of the £190.7m Aurora Investment Trust.

Although he focuses on valuations, he admitted he has been “obsessing” about the growth potential of these industries.

For banks, the market is assuming a 13-14% return on equity, but the manager predicts they are in a good position to deliver well above consensus expectations.

“What really excites me about banks and airlines is that so many of these companies now have almost-impossible-to-replicate market positions and actually quite good growth prospects,” he said.

Another misconception around these companies is that they are of lower quality, but he disagreed and said their competitive positions are “very strong”.

Performance of fund against sector and index over 5yrs

Source: FE Analytics

Banks tend to grow in line with deposit growth and to consolidate their market shares over time, he noted.

“In the past 25 years, deposits have grown about 6% per annum in the UK. If banks grow deposits by 5% or 6%, their earnings growth is going to be 10-15%,” said Channon.

As for airlines, he used Delta as an example, whose revenue growth has been twice that of Procter and Gamble and the same as L'Oreal over the past 25 years, and its competitive position has improved.

The market is substantially underestimating the potential of banks and airlines, said the manager, and what’s even better, these stocks are trading at “incredibly” low multiples.

“The earnings progression is what makes me think that the absolute opportunity here is much bigger than people think,” he concluded.

Channon is not the only one bullish on banks. Hargreaves Lansdown equity analyst Matt Britzman cited four reasons why investors should consider buying the UK’s largest banks: defaults remain low; elevated interest rates are a tailwind; capital levels support strong shareholder returns; and the UK’s economic outlook is improving.

With first-quarter results strong across the board and economic data pointing to clement conditions ahead, banks “have a spring in their step”, Britzman said.

In the same vein, J O Hambro Capital Management’s James Lowen said banks have been one of the best performing parts of his JOHCM UK Equity Income fund during the past year, but he thinks they are still cheap and have further upside. He owns Barclays, Natwest and Standard Chartered.

Channon has chosen Lloyds Banking Group as his fourth-largest position, making up 7.9% of the portfolio.

The Aurora trust also holds include Ryanair and easyJet, which respectively account for 6.8% and 4.4% of its assets under management.

Channon follows a value-based approach to investing in high-quality UK-listed businesses and aims to buy stocks at prices that allow for strong returns.

The gold price has soared recently but there could still be upside if history is anything to go by.

Since late February, the gold price has soared to new heights in nominal terms, trading at 2,349 dollars per troy ounce. There are various contributing factors including anticipated delays to rate cuts following stickier-than-expected inflation; rising geopolitical risks in the Middle East; and a weakening US dollar.

The two biggest drivers, however, appear to have been central bank purchases and algorithmic traders pushing the price up.

Gold’s recent performance indicates improved sentiment towards the metal, although in real terms the price still lags 2020 levels reached during the Covid-19 crisis. Also, if we zoom out on the performance of gold equities, the asset class is trading well below its long-term average, indicating there could still be a reasonable amount of upside from here.

Looking across the spectrum of gold investments, bullion outperformed miners. Gold miners are more closely correlated to equities, which have performed strongly, but only a narrow subset of stocks have led this outperformance and gold miners didn’t form part of that cohort.

Throughout history, gold has acted as a good inflation hedge, evident in the 1970-80s, but more recently in 2020-21 gold struggled to keep up with inflation due to headwinds such as rising bond yields.

In a similar vein, the relationship between the performance of gold and Treasury inflation-protected securities (TIPS) has decoupled over the past few years, with gold significantly outperforming those bonds. Only now, three years on, are we finally starting to see that relationship return.

Over the past few years, gold exchange-traded products have experienced significant outflows, even during the recent rally. However, the metal saw strong demand from central banks during March from countries such as China, Poland and Turkey. Gold as a proportion of foreign reserves remains very low in these countries (just 4% in China) compared with other regions such as the US, which has 70% of its foreign reserves in gold. So we could well see this demand continue.

It’s not new news but it’s worth highlighting that gold is an event risk hedge and a good diversifier in investment portfolios; in times of turmoil investors flock to safe-haven assets, including gold. We’ve observed this time and again in the past: for example, the gold price increased by 17% and 33% during the 9/11 attacks and Paris bombings respectively, whilst equities significantly lagged these figures.

Currently, geopolitical risk remains elevated, with continued conflict in Ukraine and the Middle East and rising tensions between the US and China, and therefore an allocation to gold could make sense.

The quality of gold investments has evolved over time and in 2012 the London Bullion Market Association (LBMA) published its Responsible Gold Guidance (RGG) in order to combat human rights abuse, avoid contributing to conflict and to comply with high standards of anti-money laundering and combat terrorist financing.

More recent guidance goes further and requires refiners to provide an assessment of their environmental, social and corporate governance (ESG) responsibilities. There are various passive vehicles which track the same index but have varying levels of ESG integration. By selecting products that require adherence to more recent LBMA RGGs, investors can achieve the same performance, at the same fee, whilst reducing exposure to the aforementioned risks.

So could it be gold’s time to shine? Well, despite the recent rally there could still be upside if history is anything to go by, and with central banks increasing reserves and geopolitical risks on the rise, there is a clear investment case for holding gold. And there is also the option to invest in exchange-traded funds with reduced exposure to various ESG risks if the appropriate fund is selected.

Jade Coysh is a senior research analyst at Momentum Global Investment Management. The views expressed above should not be taken as investment advice.

Experts reveal what signals retail investors should monitor to avoid pitfalls with their fund selection.

Researching and monitoring funds is a crucial aspect of investing and is indeed something that research teams at wealth management firms spend a significant amount of time doing.

Retail investors do not have access to the same level of tools and resources as manager research professionals and often have limited time available to do their own due diligence.

As such, they are at a significant disadvantage when it comes to spotting funds that might be going off the boil and identifying red flags before they cause problems.

Simon Evan-Cook, fund manager at Downing, said: “This is really hard for retail investors because the information and tools available to them are blunt at best. I suspect this is a regulatory thing, as there seems to be a view that if you give retail investors more tools and information, that they’ll end up doing themselves more harm than good. I have no idea whether this is true or not, but there you go.”

Trustnet asked experts what key aspects retail investors should keep an eye on to spot warning signals.

Put performance into context

Performance is of course a metric to monitor, but it must be assessed within a broader context.

Evan-Cook explained: “This doesn’t mean managers have to always outperform, far from it – we expect great managers to underperform from time to time.

“But it has to make sense, so if a manager follows a value style, we are fine with that if the wider value style has been having a tough time in the market. But if it’s the opposite, this is a red flag.”

Spot style drift

By the same token, Jason Hollands, managing director of Bestinvest, stressed that investors should understand their fund manager’s style and make sure they are not drifting from it.

He said: “When they appear to be straying from their professed approach, this can provide a red flag that something may be going wrong. That could be a value manager buying stocks on hefty multiples or one with a long-term ‘buy and hold’ approach significantly upping their portfolio turnover.”

Concentration isn’t always a good thing

Hollands has a preference for concentrated portfolios as they show that the managers have higher conviction in their picks.

He said: “When you see a notable change in the number of holdings, it might be indicative of lack of confidence creeping in.”

However, he also cautioned against heavy concentration, such as when three or four stocks have a disproportionate weight in the portfolio. “This does increase the risk of the fund and set the alarm bells running too,” he added.

Be wary of large funds

While performance may be the first port of call for retail investors, size also matters.

Darius McDermott, managing director of FundCalibre and Chelsea Financial Services, warned investors to be particularly careful with big funds as they are harder to manage.

“Be wary of big funds, particularly with small-cap, mid-cap or multi-cap, or bond funds. Being relatively small and nimble is key to alpha generation in these types of funds,” he explained.

Evan-Cook agreed and recommended looking for telltale signs, such as a gradual increase in the number of stocks in the portfolio or a growing exposure to mega-cap stocks instead of small-caps.

However, McDermott also called on investors to be wary of “sub-scale” funds that need to charge high fees to survive.

Keep an eye on flows

If a fund’s assets under management are shrinking rapidly, that might be because other investors may have noticed something concerning under the bonnet, according to McDermott.

Hollands agreed: “It is potentially a signal that large, institutional investors with deeper research resources and access to more portfolio information than private investors have concerns and are deserting the manager.

“Even where this is not the case, when a fund is experiencing major outflows, this can be hugely disruptive, as was the case with the collapse of the Woodford Equity Income fund.”

Yet Hollands also warned that the reverse situation is not ideal either, as rapidly growing assets under management can have an impact on the strategy.

“For example, if past successful performance has partially been driven by investing in smaller companies, rapid growth in assets may impact the ability to take such positions. Likewise, if a fund has historically had a high portfolio turnover approach, actively trading positions, growth in size may make it less nimble,” he explained.

Monitor managers’ behaviour

Investors should also observe the behaviour of their fund managers, said Evan-Cook, although he admitted that this is more of an art than a science.

“Signs of an ego getting out of control are hard to define, but if something arouses your suspicion, you might be better off out than in,” he said.

Evan-Cook also recommended that investors make sure their fund’s manager does not have too much on his or her plate in terms of other responsibilities, for instance if they manage several funds, as it might mean “they’ve taken their eye off the ball”.

Research key personnel changes

For Hollands, a manager departure is always a time for investors to consider whether the new manager has a credible track record or if they are “unknown quantity”.

He said: “Fund groups will often replace an incumbent with a deputy who may be highly familiar with the process or bring in a new team from outside.”

Corporate change could be a red flag

Finally, investors should also pay attention to potential corporate upheavals that may affect a fund group, be it a merger or acquisition and the subsequent integration or a controversy.

He said: “Institutional consultants – who advise large investors such as pension schemes – will typically freeze recommending companies going through such change until the situation stabilises.”

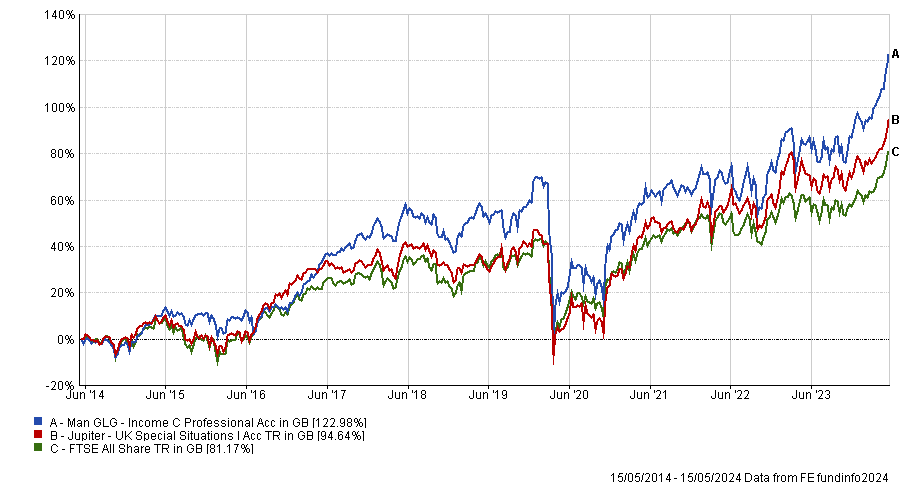

The platform is removing Jupiter’s fund following the departure of its manager, Ben Whitmore.

AJ Bell has chosen Man GLG Income to replace Jupiter UK Special Situations in its model portfolio solutions (MPS).

The decision to remove Jupiter UK Special Situations came when lead manager Ben Whitmore announced his departure to launch Brickwood Asset Management and was replaced by Alex Savvides from J O Hambro Capital Management.

AJ Bell's £2.6bn range of model portfolios are numbered one through six, with one being cautious and six being the highest risk and described as 'global growth'. The platform has added Man GLG Income to portfolios two through six, with an allocation of between 3.5% and 6%, depending on the risk level.

Ryan Hughes, interim managing director of AJ Bell Investments, said: “Ben Whitmore brought a specific value focus that blended well with the rest of the portfolio, helped by his clear investment philosophy and consistent implementation of his process, which led to strong returns. The characteristics are well shared by Henry Dixon and Man Group with a similar value bias.

“There is high correlation between the two funds, making Man GLG Income the natural replacement for Jupiter UK Special Situations, and it is a fund already well known to the investment team as it has been used in the AJ Bell Income MPS for a number of years.”

Performance of funds vs benchmark over 10yrs

Source: FE Analytics

Dixon, an FE fundinfo Alpha Manager whose £1.9bn Man GLG Income fund has achieved top-quartile returns over one, three and five years, invests with a “willingness to look across the market-cap spectrum and comfort in investing away from the index”, Hughes explained.

Square Mile Investment Consulting & Research has awarded the fund an A rating and praised Dixon’s contrarian approach. “The manager and his team are entirely focused on uncovering out of favour opportunities in order to provide both an attractive income and total return for investors. The manager ultimately has to have high conviction in a company's recovery potential, as well as the temperament to invest when others are fleeing,” Square Mile’s analysts said.

“There is definitely an ethos of exploring where others fear to tread and given the contrarian nature of the process and the willingness to invest in medium and smaller sized companies, as well as company debt and overseas stocks, the fund is likely to look and act very differently to its peers and benchmark at times.”

Hargreaves Lansdown highlights low defaults and a recovering economy as two reasons for optimism.

UK banks have outperformed the wider market over the opening months of 2024 and analysts at investment platform Hargreaves Lansdown think there are compelling reasons for further gains.

The FTSE All Share Banks index has made a 23.8% total return over 2024 to date, more than double the gain in the FTSE All Share. This adds to a recent history of strength: while it took banks a long time to recover from the financial crisis, the FTSE All Share Banks index is up 69% over five years versus just 27.3% from the FTSE All Share.

Performance of UK banks vs wider market over 2024

Source: FE Analytics. Total return in sterling between 1 Jan and 14 May 2024.

Matt Britzman, equity analyst at Hargreaves Lansdown, said: “The UK’s largest banks have a spring in their step with first quarter results strong across the board and economic data points to clement conditions ahead.”

Below, the analyst gives four key takeaways from the recent UK bank reporting season.

Default levels remain low

Loan defaults – or the failure of borrowers to make required repayments on debt – are a key concern for banks and something that investors play close attention to.

However, Britzman pointed out that borrowers have shown “impressive resilience” over the past year despite rising costs and increasing interest rates, which often make it harder for people to pay back loans.

This does not mean that loan defaults are falling. A Bank of England survey of lenders found that default rates on loans to households and small- to medium-sized businesses increased in 2024’s first quarter and are expected to have risen again in the second quarter.

“Banks need to keep track of the money they might not get back from loans, and these expected losses show up as negative entries in their financial reports,” he added. “But first quarter results were strong: fewer people than expected are failing to pay back their loans, and the hit to profits was much smaller than many had feared.”

Higher for longer interest rates could act as a tailwind

Higher interest rates tend to benefit banks – so long as they do not cause a significant uptick in loan defaults. So, with borrowers being more resilient than feared, the prospect of interest rates staying higher for longer could be another positive for many banks.

Several months ago, some of the big banks thought interest rates would be cut several times in 2024, which would reduce the income they derived from loans. However, inflation is being more sticky than central banks had hoped so they are unlikely to cut rates as fast as many first thought they would.

“It’s still too early for banks to revise their income guidance, but if current trends continue, they may have the confidence to raise guidance in the coming quarters,” Britzman said.

The UK economic outlook is improving

Another reason for optimism in UK banks are signs of an improving domestic economy. Britzman said one of the key themes raised by bank management teams in reporting season’s investor calls was an improved outlook for the UK economy, albeit “from a low base”.

Given this, banks expect lending volumes to improve over the course of the year, the housing market to continue to show signs of improvement and wage growth to remain ahead of inflation.

Britzman added that domestic-focused banks like Lloyds and NatWest, which are seen as UK economic bellwethers, look best placed to benefit from this trend.

Capital levels support strong shareholder returns

The final positive sign for UK banks is that many are banks are sitting on strong capital levels, which the Hargreaves Lansdown analyst described as “one of the key strengths of this cycle”.

This is important for investors, as this capital allows banks to absorb shocks, acts as a foundation for growing the loan book and offers scope for shareholder returns.

Britzman concluded: “The potential for shareholder returns should be seen as a key attraction for the banking sector.

“A good run so far in 2024 means yields have come down a touch, but given the strong capital positions, investors can expect some hefty dividends and buybacks over the medium term.”

Trustnet looks at emerging market and Asian equity funds that have been run by the same manager since 2004 and have achieved top-quartile returns over the past three years.

Emerging market equities have been on a rollercoaster ride during the past two decades. While they trounced developed markets in the 2000s, they have lagged behind in the 2010s.

Given this contrasting track record, seasoned managers who have weathered various market conditions may have advantages when it comes to navigating volatile markets.

Below, Trustnet researched funds in the IA Emerging Markets, IA Asia Pacific Excluding Japan, IA Asia Pacific Including Japan, IA Latin America, IA China/Greater China and IA India/Indian Subcontinent sectors that have been managed by the same person since 2004 or earlier and have produced top-quartile returns over the past three years.

Managers who ticked these boxes have been through it all and continue to make top returns.

Performance of indices from 2004 to 2014 and from 2014 to 2024

Source: FE Analytics

In the IA Emerging Markets sector, James Donald and Rohit Chopra are the only ‘veteran’ managers to have fulfilled our criteria.

They have both been in charge of Lazard Emerging Markets since 1999 and were joined by Monika Shrestha in 2006 and Ganesh Ramachandran in 2020.

Together, they look for financially productive and sensibly-priced companies, but may also consider businesses with improving returns.

Analysts at Square Mile said: “The team has followed companies and the evolution of markets for many years, and has learnt to be appreciative of the threats and opportunities that come around over time.

“In essence, the managers look for companies with high or improving financial profitability as long as they are at acceptable and attractive valuation levels. This can mean building exposure to companies, sectors or markets that have been overlooked or ignored.

“Whilst this is a good discipline to have, this relative value approach can add a higher element of volatility, in what is already a volatile asset class.”

Indeed, Lazard Emerging Markets has been relatively more volatile than the average fund in the IA Global Emerging Markets sector over the past decade, although it has done significantly better in that regard over three years, according to FE Analytics.

Performance of fund over 3yrs (to last month end) vs sector and benchmark

Source: FE Analytics

In the IA Asia Pacific Excluding Japan sector, Richard Sennitt is the only manager who has met our requirements.

He joined Schroders in 1993 and has been managing Schroder Asian Income since 2001 as well as other Asian funds.

Sennitt seeks companies in the Asia Pacific region that can deliver both income and capital growth and has a particular focus on those with earnings growth, sustainable returns and valuation support.

The portfolio typically holds between 60 and 80 stocks with a bias to high-dividend paying companies.

Analysts at FE Investment said: “The Schroder Asian Income fund does not purely buy companies in only the highest-yielding sectors – capital appreciation is equally important. The fund has managed to grow the dividend payment consistently, even through periods like the financial crisis and 2020’s global Covid restrictions, where many companies slashed dividends.

“From a portfolio perspective, this fund offers diversification benefits to income investors as mainstream equity income funds available in the market are typically focused on the UK or on developed markets.”

In terms of geography, the fund has a bias toward the more developed countries in the region, such as Australia, Taiwan and South Korea, at the expense of China and India.

Performance of fund over 3yrs (to last month end) vs sector and benchmark

Source: FE Analytics

In the IA China/Greater China sector, Martin Lau and Louisa Lo are the only two veteran managers to have made top-quartile performance over the past three years amidst a particularly challenging period for Chinese equities.

Martin Lau has been at the helm of FSSA Greater China Growth since 2003 and was joined by Helen Chen in 2019.

The fund’s mandate allows the managers to look for opportunities in Mainland China, Hong Kong and Taiwan.

Rayner Spencer Mills Research analysts said: “The benchmark-agnostic approach means that the managers avoid compromise by avoiding large constituents of the index which may not possess the superior levels of stewardship that they are seeking – this also means that the sector allocations are a residual of the stock selection process. The process emphasises absolute rather than relative returns and risk is thought of in an absolute way rather than versus the benchmark.”

Performance of funds over 3yrs (to last month end) vs sector and benchmark

Source: FE Analytics

Louisa Lo has managed Schroder ISF Greater China since 2002, which also invests in the whole Greater China region and does not specifically focus on mainland China.

Although FSSA Greater China Growth has done better over three years, Schroder ISF Greater China has slightly outperformed over the past decade. However, FSSA Greater China Growth has generally been less volatile.

No veteran managers in the IA Asia Pacific Including Japan, IA Latin America and IA India/Indian Subcontinent sectors have met our criteria.

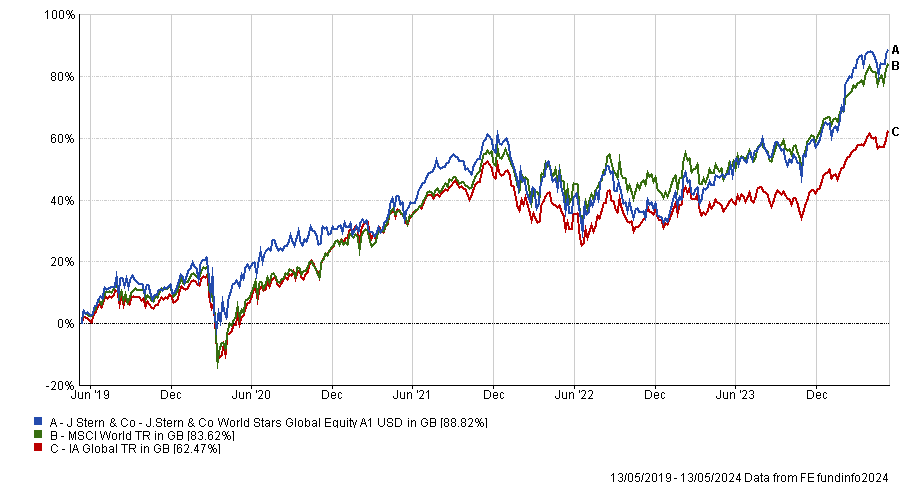

Nvidias’ valuation is “very reasonable” and Alphabet is cheap, according to J. Stern & Co.’s Chris Rossbach.

Investor demand for tech companies has skyrocketed in recent years and so have the multiples at which they trade, prompting valuation-aware managers to come out with dire warnings of dangerous hype surrounding artificial intelligence (AI).

As prices rose, so did rumours of a tech bubble that is about to burst, and experts started to say that the Magnificent Seven – the best-performing tech companies of the 2020s – could only go sideways from now on.

However, for Chris Rossbach and Katerina Kosmopoulou, managers of the J. Stern & Co. World Stars Global Equity fund, nothing could be more wrong.

In fact, Rossbach declared: “We are not in a tech bubble of any kind”.

“There are always going to be parts of the market and industries that are overvalued, but if you look at markets overall, the valuations don't seem to be excessive. Particularly in tech, they're not excessive at all.”

Semiconductor-darling Nvidia is trading on a 2025 price-to-earnings (P/E) ratio as high as 30x, but to Rossbach, that is actually “very reasonable” due to its size, scale, future prospects and the growth that it delivers.

This is particularly relevant as the managers keep an attentive eye on value and only invest in companies when prices are judged to allow for significant capital growth over five to 10 years or more. Nvidia is the top holding in the portfolio, representing 8.3% of the fund’s assets under management (AUM).

Alphabet, the parent company of Google and a leader not only in internet searches but also cloud computing, is the fifth-largest holding (4.4% of AUM) and is trading on 18x P/E, again a fair price to Rossbach.

“In fact, Alphabet is trading below the S&P 500 average multiple, so it's even below the market for the quality company that it is,” Rossbach continued.

“Big tech companies are reasonably valued compared to their prospects, and rising interest rates haven’t created a bubble but rather left many companies behind, such as many consumer, healthcare and industrial companies. We're very far away from having any kind of valuation issue,” he concluded.

The fact that mega-cap tech stocks have driven the market to its current highs does not worry Rossbach or Kosmopoulou either, because these companies’ growth is sustained. Kosmopoulou, who started her career at the time of the dot-com bubble in the early 2000s, said that is the key difference between now and then.

“Companies now are generating huge amounts of cash flow and are investing in things that effectively generate returns today. Back then, you had investments into the network, but with no visible return in sight. That's a key difference as you look back 20 years on,” she said.

Innovation and growth do not necessarily have to come from large caps either, Rossbach continued.

“One way innovation takes place is through small, innovative companies that get acquired at very high valuations by much larger companies, and these large companies can continue to prosper,” he said.

“But there's always the possibility of a disruption, especially as we get into the use cases for AI and the metaverse. It is entirely possible that some of the smaller companies will get to scale. The trillion dollar level is going to take a little bit of time, but we absolutely see many that could get into the $500bn range.”

Performance of fund against sector and index over 5yrs

Source: FE Analytics

The J. Stern & Co. World Stars Global Equity fund has recently turned five and since its inception, it has been in the top-decile of the IA Global sector, maintaining its outperformance record over the past five, three and one years.

It follows a benchmark-independent process which favours companies with pricing power and strong competitive positions in growing markets.

The market may vote to send momentum even higher in the short term, but in times like these, fundamental investors must stay the course.

The first calendar quarter was extraordinarily powerful for the price momentum factor – in layman’s terms, stocks which had gone up a lot in the previous three to six months tended to keep going up.

The MSCI World Momentum Index rose more than twice the broader MSCI World Index, increasing 21.2% versus the index up 9.9% in sterling terms. This degree of outperformance was the third-largest since the Momentum Index’s inception in the third quarter of 1973, surpassed only by the fourth quarters of 1984 and 1999, and was to the statistically minded a 2.8 standard deviation event.

We would not make too much of a 1999 comparison, as we are very aware that equity markets are what those statisticians would call a ‘non-stationary’ time series, in which the past doesn’t have the same deterministic effect that it does in stationary series (think coin flips).

The intuition behind this is that markets remember in a way that coins being tossed do not – the history of booms and busts has a ‘scarring’ effect on the collective minds of investors and means we cannot automatically extrapolate from what followed after Q4 1999 or, for that matter, Q4 1984.

Eyes on earnings

Evenlode’s valuation discipline and process mean that we rebalanced all our portfolios through the first quarter of 2024 into positions which were becoming better value as prices fell, in a market where this was an unusually punishing trade for relative returns.

Our focus is on a company’s cash earnings potential, adjusted for risk and capital intensity, over a horizon of five years and beyond, so there will be times when price momentum and long-term earnings potential diverge. When this happens, we will always follow long-term earnings potential.

There will also of course be times when price momentum and long-term earnings align. Our strategies are not necessarily negatively correlated with momentum, particularly when related to the wider index. However, history suggests that when momentum is unusually strong, our style is likely to suffer in relative terms. We think this is particularly the case right now when momentum is being fed by two separate waves, both of which tend to exclude the Evenlode Global Equity fund.

In the first group (as was the case in 1999 with the bull market in technology, media and telecoms) powerful thematic trends around generative artificial intelligence (AI) and drug innovation in GLP-1s for diabetes and obesity are driving some mega-caps to extraordinary new highs.

While we have exposure to the generative AI trend through Alphabet, Amazon and Microsoft, we have avoided pure plays on these trends as we are cautious around cyclicality and high thematic concentration.

Secondly, more like the Volcker boom of the 1980s, securities prices are being adjusted upwards after a period of inflation and a widely feared recession, in expectation of continued declines in borrowing costs and a resurgent global economy driven by the US. This has restrained the relative performance of companies which are less sensitive to changes in rates and economic growth.

With that being said, work we have done on fundamental earnings revisions suggests that our portfolio companies’ earnings expectations were little different to those of the index during the quarter.

Emerging opportunities

We prefer not to spend too much time worrying about factors and the macro context. The resilience of our portfolio companies’ earnings, both in the Q4 2023 reporting season and in the incremental revisions to consensus, makes us additionally confident that we have not strayed in our pursuit of compounding ability.

There are many things our companies are up to which excite us. For example, the opportunity for the card networks Mastercard and Visa to expand their sales of value-added services to issuers, acquirers and merchants; the opportunity for traditional data firms such as Verisk, Experian and RELX to improve the productivity of clients by offering more sophisticated analytics packages; and the opportunity for beauty and spirits companies like L’Oréal and Diageo to expand their footprint in emerging markets while further extending their innovation-based pricing pyramids in developed markets.

We expect there will be more ingots of treasure to heap onto the ‘weighing machine’ of cumulative shareholder earnings, described by Benjamin Graham. In the short-term, as Graham also observed, the market may vote to send momentum higher, but it is in these very times when you must stay the course.

James Knoedler is portfolio manager of the Evenlode Global Equity fund. The views expressed above should not be taken as investment advice.

A myriad of catalysts are spurring UK equities to new heights but not all stocks will benefit equally.

Catalysts to reignite the UK equity market are all coming in to land at once, like planes at Heathrow Airport, and the stock market itself is finally taking off.